Advertisement

Should You Worry About James Cropper PLC's (LON:CRPR) CEO Pay?

In 2012, Phil Wild was appointed CEO of James Cropper PLC (LON:CRPR). This report will, first, examine the CEO compensation levels in comparison to CEO compensation at companies of similar size. Next, we'll consider growth that the business demonstrates. Third, we'll reflect on the total return to shareholders over three years, as a second measure of business performance. The aim of all this is to consider the appropriateness of CEO pay levels.

Check out our latest analysis for James Cropper

How Does Phil Wild's Compensation Compare With Similar Sized Companies?

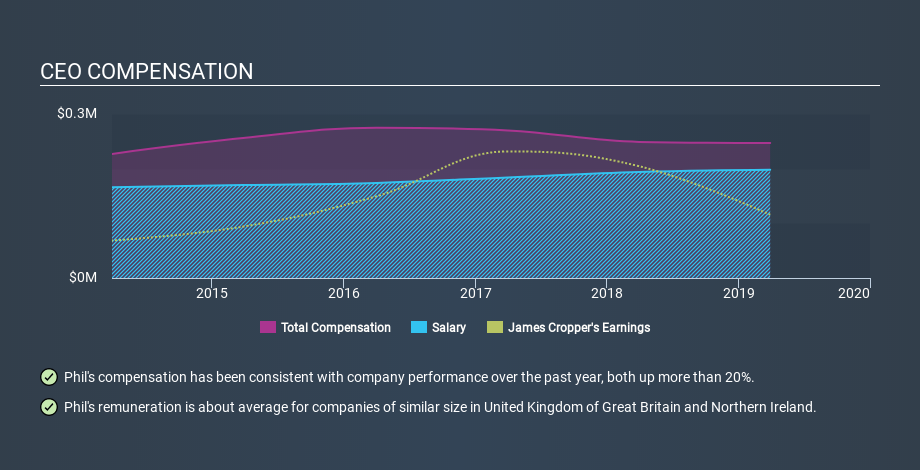

According to our data, James Cropper PLC has a market capitalization of UK£105m, and paid its CEO total annual compensation worth UK£247k over the year to March 2019. While we always look at total compensation first, we note that the salary component is less, at UK£198k. We took a group of companies with market capitalizations below UK£159m, and calculated the median CEO total compensation to be UK£272k.

Next, let's break down remuneration compositions to understand how the industry and company compare with each other. Talking in terms of the sector, salary represented approximately 63% of total compensation out of all the companies we analysed, while other remuneration made up 37% of the pie. So it seems like there isn't a significant difference between James Cropper and the broader market, in terms of salary allocation in the overall compensation package.

That means Phil Wild receives fairly typical remuneration for the CEO of a company that size. Although this fact alone doesn't tell us a great deal, it becomes more relevant when considered against the business performance. You can see a visual representation of the CEO compensation at James Cropper, below.

Is James Cropper PLC Growing?

On average over the last three years, James Cropper PLC has shrunk earnings per share by 22% each year (measured with a line of best fit). In the last year, its revenue is up 4.7%.

Unfortunately, earnings per share have trended lower over the last three years. The fairly low revenue growth fails to impress given that the earnings per share is down. So given this relatively weak performance, shareholders would probably not want to see high compensation for the CEO. You might want to check this free visual report on analyst forecasts for future earnings.

Has James Cropper PLC Been A Good Investment?

With a three year total loss of 24%, James Cropper PLC would certainly have some dissatisfied shareholders. It therefore might be upsetting for shareholders if the CEO were paid generously.

In Summary...

Phil Wild is paid around what is normal for the leaders of comparable size companies.

The company isn't growing EPS, and shareholder returns have been disappointing. Most would consider it prudent for the company to hold off any CEO pay rise until performance improves. On another note, we've spotted 3 warning signs for James Cropper that investors should look into moving forward.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies, that have HIGH return on equity and low debt.

Love or hate this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned. Thank you for reading.

About AIM:CRPR

James Cropper

Manufactures and sells paper products and advanced materials.

Undervalued with adequate balance sheet.

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Upside Gold ·

An Undervalued 3.3Moz Gold Project in Canada

Fair Value:CA$5.0778.3% undervalued

206 followersusers have followed this narrative

1 commentusers have commented on this narrative

29 likesusers have liked this narrative

SI

SimpleMan887 on GameStop ·

GameStop will ace the financial crisis wave with its strategic Bitcoin investment and cash reserves

Fair Value:US$22089.6% undervalued

52 followersusers have followed this narrative

2 commentsusers have commented on this narrative

21 likesusers have liked this narrative

YI

yiannisz on Hesai Group ·

The First Real Lidar Winner

Fair Value:US$27.0719.2% undervalued

13 followersusers have followed this narrative

1 commentusers have commented on this narrative

3 likesusers have liked this narrative

TR

tripledub on Taiwan Semiconductor Manufacturing ·

The Most Wonderful Monopoly in the Most Dangerous Neighbourhood on Earth

Fair Value:US$3814.0% undervalued

9 followersusers have followed this narrative

0 commentsusers have commented on this narrative

10 likesusers have liked this narrative

Recently Updated Narratives

AS

AstrisCorporateAdvisory on Ceres ·

Proven business incubator in transition

Fair Value:JP¥2.37k36.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FA

FA_Trader on Hektar Real Estate Investment Trust ·

Hektar REIT: Outlook is getting more interesting as retail stabilises and diversification starts to kick in

Fair Value:RM 0.4910.2% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on Guanajuato Silver ·

A Case for Guanajuato Silver (TSXV:GSVR) to reach (low end) CAD$4 (high end) CAD$18 by 2031

Fair Value:CA$1896.6% undervalued

19 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

YA

Yang_ on SoFi Technologies ·

SoFi Technologies: The Apex Aggregator and the Infrastructure of the Modern Financial System

Fair Value:US$22.9828.2% undervalued

54 followersusers have followed this narrative

0 commentsusers have commented on this narrative

38 likesusers have liked this narrative

TR

tripledub on Microsoft ·

Everyone's Terrified Microsoft Will Keep Spending. I'm Terrified They'll Stop.

Fair Value:US$3955.2% undervalued

43 followersusers have followed this narrative

3 commentsusers have commented on this narrative

41 likesusers have liked this narrative

RO

Robbo on Tesla ·

The academically fascinating Tesla

Fair Value:US$301.0k% overvalued

36 followersusers have followed this narrative

11 commentsusers have commented on this narrative

31 likesusers have liked this narrative