Advertisement

- United States

- /

- Trade Distributors

- /

- NYSE:WSO

Should You Consider Watsco, Inc. (NYSE:WSO)?

Want to participate in a short research study? Help shape the future of investing tools and you could win a $250 gift card!

I've been keeping an eye on Watsco, Inc. (NYSE:WSO) because I'm attracted to its fundamentals. Looking at the company as a whole, as a potential stock investment, I believe WSO has a lot to offer. Basically, it is a financially-robust , dividend-paying company with a strong history of performance. Below, I've touched on some key aspects you should know on a high level. If you're interested in understanding beyond my broad commentary, read the full report on Watsco here.

Flawless balance sheet with proven track record and pays a dividend

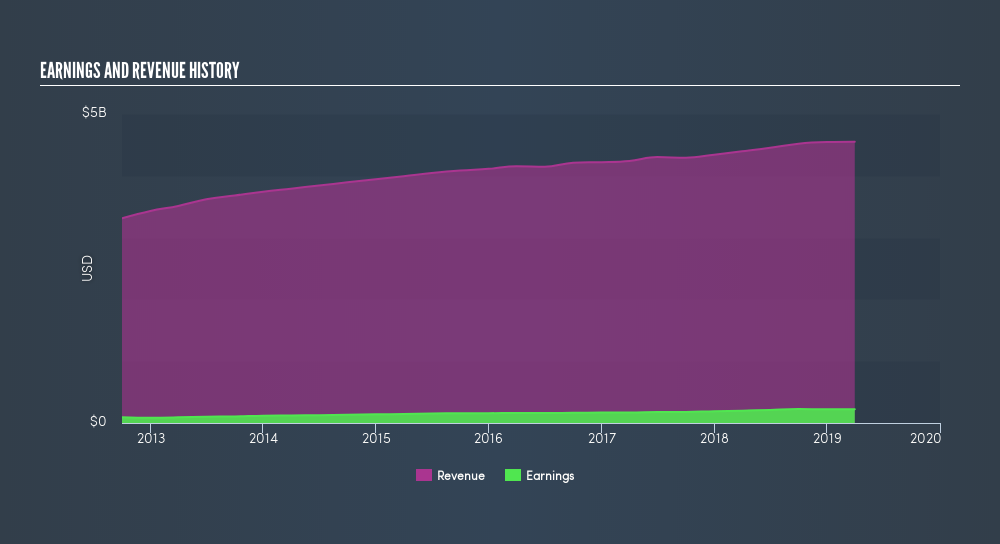

Over the past year, WSO has grown its earnings by 12%, with its most recent figure exceeding its annual average over the past five years. Not only did WSO outperformed its past performance, its growth also surpassed the Trade Distributors industry expansion, which generated a -7.0% earnings growth. This is an optimistic signal for the future. WSO's strong financial health means that all of its upcoming liability payments are able to be met by its current cash and short-term investment holdings. This indicates that WSO has sufficient cash flows and proper cash management in place, which is a crucial insight into the health of the company. WSO appears to have made good use of debt, producing operating cash levels of 1.86x total debt in the prior year. This is a strong indication that debt is reasonably met with cash generated.

WSO’s reputation for being one of the best dividend payers in the market is supported by the fact that it has been steadily growing its dividend payments over the past ten years and currently is one of the top yielding companies on the markets, at 3.9%.

Next Steps:

For Watsco, I've put together three essential factors you should further research:

- Future Outlook: What are well-informed industry analysts predicting for WSO’s future growth? Take a look at our free research report of analyst consensus for WSO’s outlook.

- Valuation: What is WSO worth today? Is the stock undervalued, even when its growth outlook is factored into its intrinsic value? The intrinsic value infographic in our free research report helps visualize whether WSO is currently mispriced by the market.

- Other Attractive Alternatives : Are there other well-rounded stocks you could be holding instead of WSO? Explore our interactive list of stocks with large potential to get an idea of what else is out there you may be missing!

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About NYSE:WSO

Watsco

Engages in the distribution of air conditioning, heating, and refrigeration equipment, and related parts and supplies in the United States, Canada, Latin America, and the Caribbean.

Flawless balance sheet average dividend payer.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Virtuix Holdings ·

From a “Shark Tank” Snub to an Air Force “Yes”: Why Virtuix at $3.50 May Be the Market’s Most Mispriced AI Story

Fair Value:US$7.562.8% undervalued

21 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75033.5% undervalued

69 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

TR

tripledub on Intuit ·

A Wonderful Business at a Not-So-Wonderful Price

Fair Value:US$56052.2% undervalued

64 followersusers have followed this narrative

4 commentsusers have commented on this narrative

30 likesusers have liked this narrative

TA

Talos on MindWalk Holdings ·

The Asymmetric TechBio Play: MindWalk Holdings and the Valuation Disconnect

Fair Value:US$8.2780.9% undervalued

35 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Recently Updated Narratives

RO

RockeTeller on Orezone Gold ·

Orezone Gold Could 3X–5X, Bomboré Ramp + Casa Berardi Quebec Asset Delivers 160-180Koz in 2026

Fair Value:CA$10.6878.4% undervalued

9 followersusers have followed this narrative

4 commentsusers have commented on this narrative

1 likeusers have liked this narrative

IV

Ivoed on Netflix ·

Netflix’s Business Quality Is Clear. The Harder Question Is Whether The Stock Is Still Cheap

Fair Value:US$8210.0% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

RockeTeller on NeXGold Mining ·

NexGold Mining: 4.7Moz M&I Resources, $100M Cash + Debt-Free, Construction Decision 2026 Undervalued Canadian Gold Developer

Fair Value:CA$39.5296.9% undervalued

5 followersusers have followed this narrative

3 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75033.5% undervalued

69 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9636.6% undervalued

61 followersusers have followed this narrative

9 commentsusers have commented on this narrative

19 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7442.1% undervalued

68 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative