Advertisement

- Spain

- /

- Specialty Stores

- /

- BME:ITX

Should You Buy Industria de Diseño Textil, S.A. (BME:ITX) When Prices Drop?

Stock market crashes are an opportune time to buy. High quality companies, such as Industria de Diseño Textil, S.A., are impacted by general market panic and sell-off, but the fundamentals of these companies stay the same. In other words, now is the time to buy strong, well-proven stocks at an attractive discount.

See our latest analysis for Industria de Diseño Textil

Industria de Diseño Textil, S.A. engages in the retail and online distribution of clothing, footwear, accessories, and household textile products through various commercial concepts. Formed in 1963, and run by CEO Carlos Crespo González, the company currently employs 131.66k people and with the company's market capitalisation at €88b, we can put it in the large-cap stocks category. Size matters. The bigger the company is, the more well-resourced it is. The more money it produces from its operations which means it is less reliant on external funding. When times are bad in the market, being self-sufficient is extremely important as you can continue to operate at your own pace. Therefore, large cap companies are a great bet to invest in when you're heading to the bottom of the cycle.

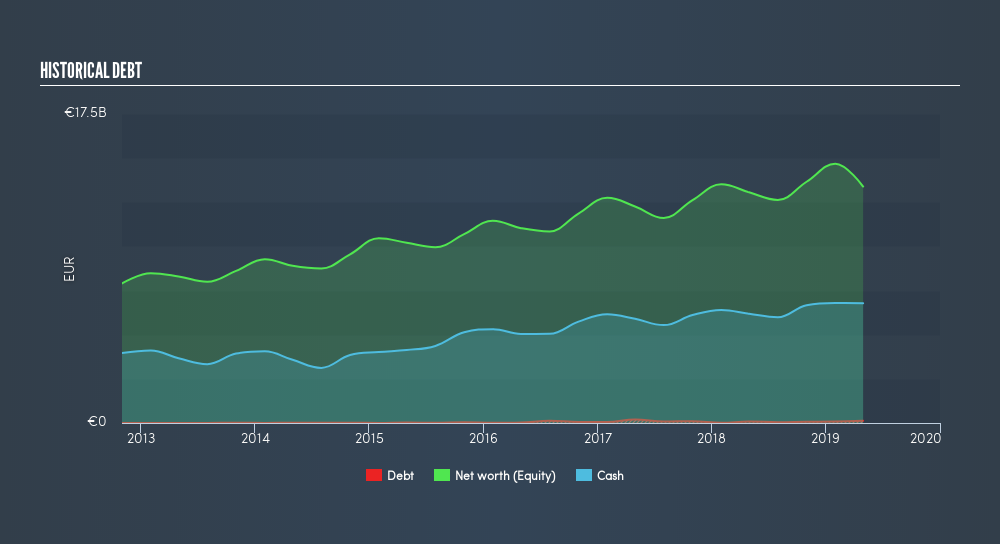

Currently Industria de Diseño Textil has €124m on its balance sheet, which requires regular interest payments. This requires the business to have enough cash to meet these upcoming interest expenses. With an interest coverage ratio of 172x, Industria de Diseño Textil produces sufficient earnings (EBIT) to cover its interest payments. Anything above 3x is considered safe practice. Moreover, its operating cash flows amply covers its total debt by more than 2x, which is higher than the bare minimum requirement of 0.2x. And, a given, its liquidity ratio holds up well with cash and other liquid assets exceeding upcoming liabilities, meaning ITX's financial strength will continue to let it thrive in a fickle market.

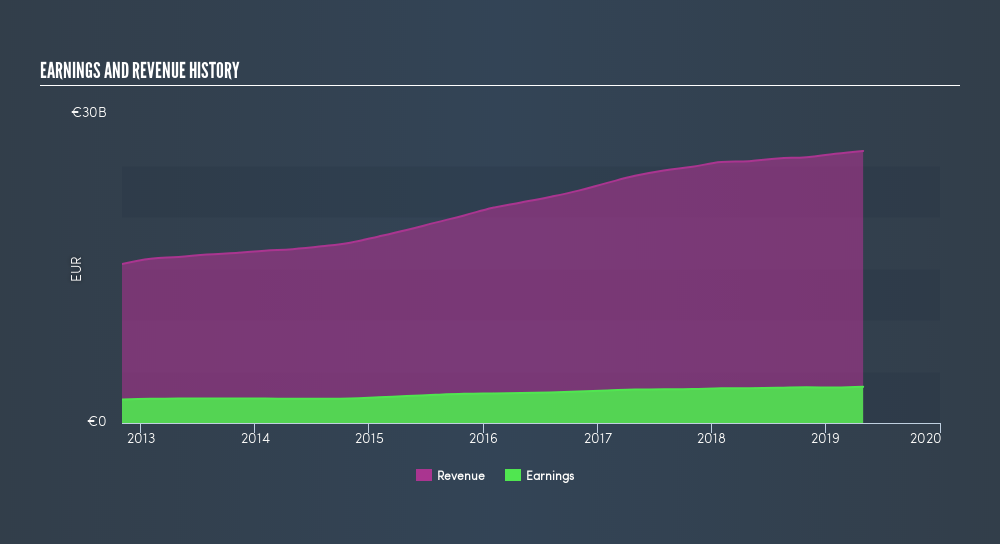

ITX’s year-on-year earnings growth has been positive over the past five years, with an average annual growth rate of 8.3%, beating the industry growth rate of 7.8%. It has also returned an ROE of 26% recently, above the industry return of 9.9%. This continuous market outperformance demonstrates a strong track record of delivering robust returns over many years, raising my confidence in Industria de Diseño Textil as a long-term hold.

Next Steps:

Industria de Diseño Textil makes for a robust long-term investment based on its scale, financial health and track record. Remember, in bear markets, sell-offs can be unjustified. Ask yourself, has anything really changed with Industria de Diseño Textil? If not, then why not scoop it up at a discount? Lining your portfolio with a few well-established companies can reduce your risk and help you scale your wealth in the long run. One thing you should remember though, is to do your homework. Do your own research, come up with your point of view. Below is a list I've put together of other things you should consider before you buy:- Future Outlook: What are well-informed industry analysts predicting for ITX’s future growth? Take a look at our free research report of analyst consensus for ITX’s outlook.

- Valuation: What is ITX worth today? Is the stock undervalued, even when its growth outlook is factored into its intrinsic value? The intrinsic value infographic in our free research report helps visualize whether ITX is currently mispriced by the market.

- Other High-Performing Stocks: Are there other stocks that provide better prospects with proven track records? Explore our free list of these great stocks here.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About BME:ITX

Industria de Diseño Textil

Engages in the retail and online distribution of clothing, footwear, accessories, and household products in Spain, rest of Europe, the Americas, Asia, and internationally.

Flawless balance sheet with solid track record and pays a dividend.

Market Insights

Advertisement

Community Narratives

Vita Life Sciences Set for a 12.72% Revenue Growth While Tackling Operational Challenges

Fair Value AU$2.42|8.7% undervalued

RO

Community Contributor

Vossloh rides a €500 billion wave to boost growth and earnings in the next decade

Fair Value €78.41|7.2% undervalued

CH

Community Contributor

Intuitive Surgical Will Transform Healthcare with 12% Revenue Growth

Fair Value US$325.55|56.5% overvalued

UN

Community Contributor