- Hong Kong

- /

- Real Estate

- /

- SEHK:683

Read This Before Considering Kerry Properties Limited (HKG:683) For Its Upcoming 1.5% Dividend

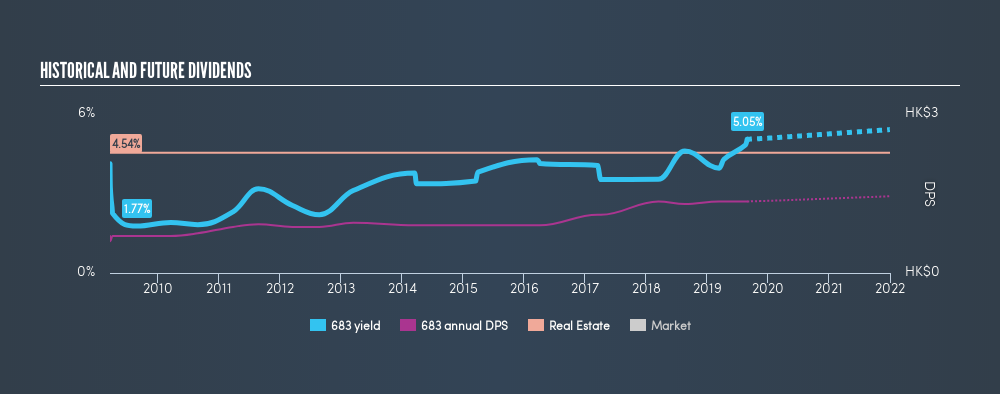

Readers hoping to buy Kerry Properties Limited (HKG:683) for its dividend will need to make their move shortly, as the stock is about to trade ex-dividend. You can purchase shares before the 3rd of September in order to receive the dividend, which the company will pay on the 17th of September.

Kerry Properties's next dividend payment will be HK$0.40 per share, on the back of last year when the company paid a total of HK$1.35 to shareholders. Last year's total dividend payments show that Kerry Properties has a trailing yield of 5.0% on the current share price of HK$26.75. Dividends are a major contributor to investment returns for long term holders, but only if the dividend continues to be paid. That's why we should always check whether the dividend payments appear sustainable, and if the company is growing.

View our latest analysis for Kerry Properties

Dividends are typically paid out of company income, so if a company pays out more than it earned, its dividend is usually at a higher risk of being cut. Fortunately Kerry Properties's payout ratio is modest, at just 28% of profit. A useful secondary check can be to evaluate whether Kerry Properties generated enough free cash flow to afford its dividend. Luckily it paid out just 12% of its free cash flow last year.

It's positive to see that Kerry Properties's dividend is covered by both profits and cash flow, since this is generally a sign that the dividend is sustainable, and a lower payout ratio usually suggests a greater margin of safety before the dividend gets cut.

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Have Earnings And Dividends Been Growing?

Stocks with flat earnings can still be attractive dividend payers, but it is important to be more conservative with your approach and demand a greater margin for safety when it comes to dividend sustainability. If business enters a downturn and the dividend is cut, the company could see its value fall precipitously. With that in mind, we're not enthused to see that Kerry Properties's earnings per share have remained effectively flat over the past five years. Better than seeing them fall off a cliff, for sure, but the best dividend stocks grow their earnings meaningfully over the long run.

Another key way to measure a company's dividend prospects is by measuring its historical rate of dividend growth. Kerry Properties has delivered an average of 6.8% per year annual increase in its dividend, based on the past ten years of dividend payments.

To Sum It Up

Is Kerry Properties worth buying for its dividend? Earnings per share have been flat, although at least the company is paying out a low and conservative percentage of both its earnings and cash flow. It's definitely not great to see earnings falling, but at least there may be some buffer before the dividend gets cut. Overall we're not hugely bearish on the stock, but there are likely better dividend investments out there.

Wondering what the future holds for Kerry Properties? See what the 11 analysts we track are forecasting, with this visualisation of its historical and future estimated earnings and cash flow

A common investment mistake is buying the first interesting stock you see. Here you can find a list of promising dividend stocks with a greater than 2% yield and an upcoming dividend.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About SEHK:683

Kerry Properties

An investment holding company, engages in the development, investment, management, and trading of properties in Hong Kong, Mainland China, and the Asia Pacific region.

Reasonable growth potential average dividend payer.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Title: Market Sentiment Is Dead Wrong — Here's Why PSEC Deserves a Second Look

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion