Advertisement

- India

- /

- Real Estate

- /

- NSEI:GEECEE

Lacklustre Performance Driving GeeCee Ventures Limited's (NSE:GEECEE) P/E

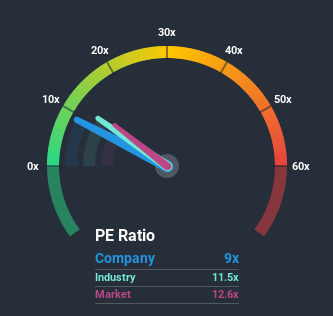

With a price-to-earnings (or "P/E") ratio of 9x GeeCee Ventures Limited (NSE:GEECEE) may be sending bullish signals at the moment, given that almost half of all companies in India have P/E ratios greater than 13x and even P/E's higher than 30x are not unusual. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's limited.

As an illustration, earnings have deteriorated at GeeCee Ventures over the last year, which is not ideal at all. It might be that many expect the disappointing earnings performance to continue or accelerate, which has repressed the P/E. However, if this doesn't eventuate then existing shareholders may be feeling optimistic about the future direction of the share price.

Check out our latest analysis for GeeCee Ventures

Does Growth Match The Low P/E?

There's an inherent assumption that a company should underperform the market for P/E ratios like GeeCee Ventures' to be considered reasonable.

Taking a look back first, the company's earnings per share growth last year wasn't something to get excited about as it posted a disappointing decline of 55%. This means it has also seen a slide in earnings over the longer-term as EPS is down 42% in total over the last three years. So unfortunately, we have to acknowledge that the company has not done a great job of growing earnings over that time.

Weighing that medium-term earnings trajectory against the broader market's one-year forecast for a contraction of 6.7% shows the market is more attractive on an annualised basis regardless.

With this information, it's not too hard to see why GeeCee Ventures is trading at a lower P/E in comparison. However, when earnings shrink rapidly P/E often shrinks too, which could set up shareholders for future disappointment regardless. Even just maintaining these prices will be difficult to achieve as recent earnings trends are already weighing down the shares heavily.

The Key Takeaway

The price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

We've established that GeeCee Ventures maintains its low P/E on the weakness of its recentthree-year earnings being even worse than the forecasts for a struggling market, as expected. Right now shareholders are accepting the low P/E as they concede future earnings probably won't provide any pleasant surprises. Although, we would be concerned whether the company can even maintain its medium-term level of performance under these tough market conditions. For now though, it's hard to see the share price rising strongly in the near future under these circumstances.

It is also worth noting that we have found 2 warning signs for GeeCee Ventures that you need to take into consideration.

Of course, you might also be able to find a better stock than GeeCee Ventures. So you may wish to see this free collection of other companies that sit on P/E's below 20x and have grown earnings strongly.

If you’re looking to trade GeeCee Ventures, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account.Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About NSEI:GEECEE

GeeCee Ventures

Engages in the real estate development, renewable energy, and financial service businesses in India.

Flawless balance sheet, good value and pays a dividend.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor