Advertisement

- United States

- /

- Retail REITs

- /

- NYSE:WSR

Is Whitestone REIT's (NYSE:WSR) CEO Pay Fair?

In 2006 Jim Mastandrea was appointed CEO of Whitestone REIT (NYSE:WSR). This analysis aims first to contrast CEO compensation with other companies that have similar market capitalization. After that, we will consider the growth in the business. And finally - as a second measure of performance - we will look at the returns shareholders have received over the last few years. This method should give us information to assess how appropriately the company pays the CEO.

View our latest analysis for Whitestone REIT

How Does Jim Mastandrea's Compensation Compare With Similar Sized Companies?

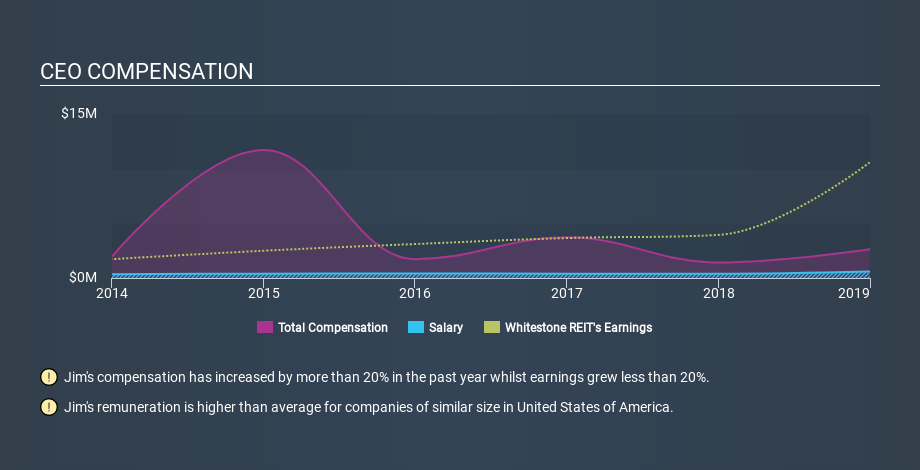

Our data indicates that Whitestone REIT is worth US$564m, and total annual CEO compensation was reported as US$2.6m for the year to December 2018. While we always look at total compensation first, we note that the salary component is less, at US$600k. We further remind readers that the CEO may face performance requirements to receive the non-salary part of the total compensation. As part of our analysis we looked at companies in the same jurisdiction, with market capitalizations of US$200m to US$800m. The median total CEO compensation was US$1.7m.

As you can see, Jim Mastandrea is paid more than the median CEO pay at companies of a similar size, in the same market. However, this does not necessarily mean Whitestone REIT is paying too much. A closer look at the performance of the underlying business will give us a better idea about whether the pay is particularly generous.

You can see, below, how CEO compensation at Whitestone REIT has changed over time.

Is Whitestone REIT Growing?

Whitestone REIT has increased its earnings per share (EPS) by an average of 34% a year, over the last three years (using a line of best fit). It saw its revenue drop 3.7% over the last year.

This shows that the company has improved itself over the last few years. Good news for shareholders. Revenue growth is a real positive for growth, but ultimately profits are more important. It could be important to check this free visual depiction of what analysts expect for the future.

Has Whitestone REIT Been A Good Investment?

With a total shareholder return of 23% over three years, Whitestone REIT shareholders would, in general, be reasonably content. But they probably wouldn't be so happy as to think the CEO should be paid more than is normal, for companies around this size.

In Summary...

We examined the amount Whitestone REIT pays its CEO, and compared it to the amount paid by similar sized companies. We found that it pays well over the median amount paid in the benchmark group.

Importantly, though, the company has impressed with its earnings per share growth, over three years. Looking at the same time period, we think that the shareholder returns are respectable. You might wish to research management further, but on this analysis, considering the EPS growth, we wouldn't call the CEO pay problematic. CEO compensation is one thing, but it is also interesting to check if the CEO is buying or selling Whitestone REIT (free visualization of insider trades).

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies, that have HIGH return on equity and low debt.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About NYSE:WSR

Whitestone REIT

A community-centered real estate investment trust (REIT) that acquires, owns, operates, and develops open-air, retail centers located in some of the fastest growing markets in the country: Phoenix, Austin, Dallas-Fort Worth, Houston and San Antonio.

Moderate risk and good value.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Virtuix Holdings ·

From a “Shark Tank” Snub to an Air Force “Yes”: Why Virtuix at $3.50 May Be the Market’s Most Mispriced AI Story

Fair Value:US$7.559.3% undervalued

32 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

HE

HedgeY on IonQ ·

The Best-Funded Quantum Platform and Still a Stock Priced for Perfection

Fair Value:US$4811.0% overvalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5446.8% undervalued

11 followersusers have followed this narrative

1 commentusers have commented on this narrative

5 likesusers have liked this narrative

IV

Ivoed on Netflix ·

Netflix’s Business Quality Is Clear. The Harder Question Is Whether The Stock Is Still Cheap

Fair Value:US$8212.9% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

Recently Updated Narratives

AN

andre_santos on NIKE ·

Nike - A Fundamental and Historical Valuation

Fair Value:US$36.8311.5% overvalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TR

TripleS on AnaptysBio ·

ANAB has a scaling and rising royalty stream, one up and coming new royalty, a loan that dies in 2027 which will result in a doubling

Fair Value:US$9025.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

GE

Germaine on MM Computer Systems Berhad ·

MM Computer Systems' Latest Contract Wins Reinforce Growth Momentum After Listing

Fair Value:RM 0.3313.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75031.5% undervalued

79 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9635.9% undervalued

62 followersusers have followed this narrative

9 commentsusers have commented on this narrative

19 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7441.2% undervalued

68 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative