Advertisement

- United States

- /

- Software

- /

- NasdaqGS:VRNT

Is Verint Systems Inc. (NASDAQ:VRNT) Potentially Undervalued?

Verint Systems Inc. (NASDAQ:VRNT), which is in the software business, and is based in United States, received a lot of attention from a substantial price movement on the NASDAQGS over the last few months, increasing to $62.27 at one point, and dropping to the lows of $52.9. Some share price movements can give investors a better opportunity to enter into the stock, and potentially buy at a lower price. A question to answer is whether Verint Systems's current trading price of $54.31 reflective of the actual value of the mid-cap? Or is it currently undervalued, providing us with the opportunity to buy? Let’s take a look at Verint Systems’s outlook and value based on the most recent financial data to see if there are any catalysts for a price change.

View our latest analysis for Verint Systems

Is Verint Systems still cheap?

According to my valuation model, Verint Systems seems to be fairly priced at around 7.6% below my intrinsic value, which means if you buy Verint Systems today, you’d be paying a reasonable price for it. And if you believe that the stock is really worth $58.8, then there isn’t much room for the share price grow beyond what it’s currently trading. So, is there another chance to buy low in the future? Given that Verint Systems’s share is fairly volatile (i.e. its price movements are magnified relative to the rest of the market) this could mean the price can sink lower, giving us an opportunity to buy later on. This is based on its high beta, which is a good indicator for share price volatility.

Can we expect growth from Verint Systems?

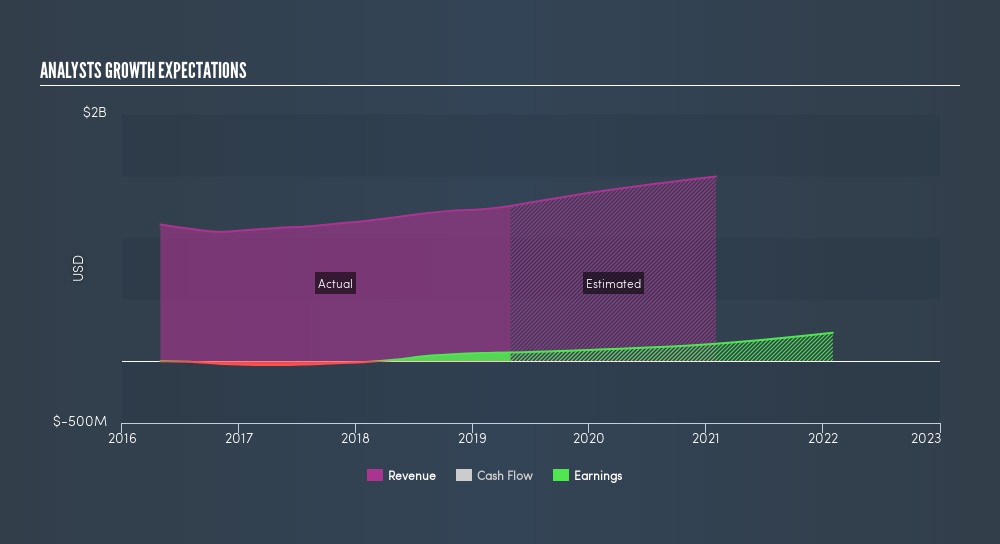

Investors looking for growth in their portfolio may want to consider the prospects of a company before buying its shares. Although value investors would argue that it’s the intrinsic value relative to the price that matter the most, a more compelling investment thesis would be high growth potential at a cheap price. Verint Systems’s earnings over the next few years are expected to double, indicating a very optimistic future ahead. This should lead to stronger cash flows, feeding into a higher share value.

What this means for you:

Are you a shareholder? It seems like the market has already priced in VRNT’s positive outlook, with shares trading around its fair value. However, there are also other important factors which we haven’t considered today, such as the financial strength of the company. Have these factors changed since the last time you looked at the stock? Will you have enough conviction to buy should the price fluctuates below the true value?

Are you a potential investor? If you’ve been keeping an eye on VRNT, now may not be the most advantageous time to buy, given it is trading around its fair value. However, the optimistic prospect is encouraging for the company, which means it’s worth diving deeper into other factors such as the strength of its balance sheet, in order to take advantage of the next price drop.

Price is just the tip of the iceberg. Dig deeper into what truly matters – the fundamentals – before you make a decision on Verint Systems. You can find everything you need to know about Verint Systems in the latest infographic research report. If you are no longer interested in Verint Systems, you can use our free platform to see my list of over 50 other stocks with a high growth potential.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About NasdaqGS:VRNT

Verint Systems

Provides customer engagement solutions worldwide.

Undervalued with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

DA

davidlsander on Optimi Health ·

OPTH: A licensed manufacturer already selling MDMA while peers still wait on trials

Fair Value:US$1259.6% undervalued

14 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

FU

FundamentalFlow on Vertiv Holdings Co ·

The Short and Long Term Compounder of Liquid Cooling industry.

Fair Value:US$45040.0% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

JO

John_Eric on SPX Technologies ·

I Fell in Love With a Data-Center Cooling Stock. Then I Opened the Filings.

Fair Value:US$2034.6% overvalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

TR

tripledub on GQG Partners ·

The Cheap Genius Problem

Fair Value:AU$2.4541.2% undervalued

14 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

Recently Updated Narratives

RC

rcb9 on Palantir Technologies ·

The Fifty-Five Percent Margin Is A Tax Holiday, Not The Business

Fair Value:US$91.8590.8% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

KL

Klim on PetroTal ·

PetroTal: Betting On a Production Recovery

Fair Value:CA$0.8542.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DA

david_1211213 on Robo.ai ·

Robo.ai (AIIO): A Long-Term Bullish Technical Setup

Fair Value:US$5.6443.6% undervalued

1 followerusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on NVIDIA ·

The company that went from selling GPUs to gamers to becoming the AI arms dealer of the 21st century.

Fair Value:US$28022.3% undervalued

294 followersusers have followed this narrative

9 commentsusers have commented on this narrative

16 likesusers have liked this narrative

CU

CubanEros on Microsoft ·

A wonderful business at reasonable price.

Fair Value:US$419.9120.5% overvalued

156 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

KI

KiwiInvest on Amazon.com ·

Amazon's high growth, high tech segments propel its profits, while traditional segments plod along

Fair Value:US$475.0941.5% undervalued

177 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

Trending Discussion

IA

ian_oii7z on Woodside Energy Group ·

Hey James! Thank you but I am not sure if I am reading this correctly as your analysis opens with "At A$36.602 per share, Woodside Energy Group (ASX: WDS) appears reasonably valued based on its existing operations and near-term production growth." I would like to say that the last time that WDS was above $36.00 per share was in October 2023, so I am a little confused by your statement w.r.t. current prices etc . Can you please explain?

1

|0

GE

george_b177x on Bloom Energy ·

Brilliant analysis. Great company with proven product and service!

0

|0