Advertisement

Is Umang Dairies Limited (NSE:UMANGDAIRY) A Good Fit For Your Dividend Portfolio?

Today we'll take a closer look at Umang Dairies Limited (NSE:UMANGDAIRY) from a dividend investor's perspective. Owning a strong business and reinvesting the dividends is widely seen as an attractive way of growing your wealth. On the other hand, investors have been known to buy a stock because of its yield, and then lose money if the company's dividend doesn't live up to expectations.

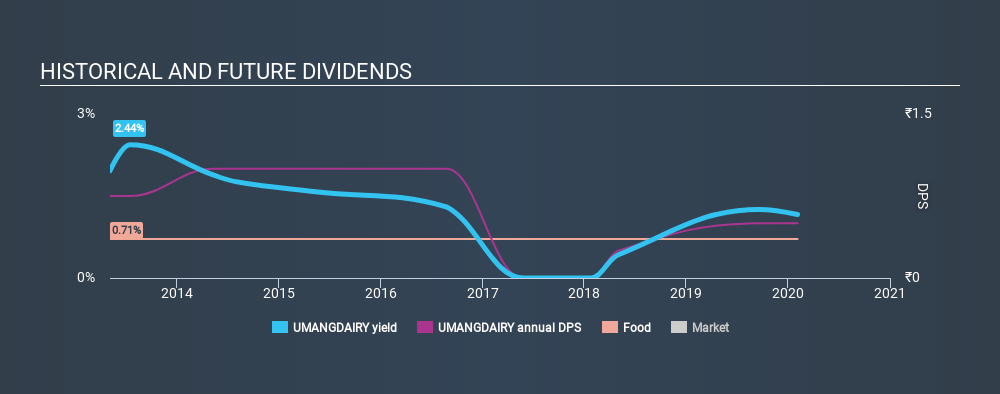

Investors might not know much about Umang Dairies's dividend prospects, even though it has been paying dividends for the last seven years and offers a 1.2% yield. A low yield is generally a turn-off, but if the prospects for earnings growth were strong, investors might be pleasantly surprised by the long-term results. Some simple analysis can offer a lot of insights when buying a company for its dividend, and we'll go through this below.

Explore this interactive chart for our latest analysis on Umang Dairies!

Payout ratios

Dividends are usually paid out of company earnings. If a company is paying more than it earns, then the dividend might become unsustainable - hardly an ideal situation. So we need to form a view on if a company's dividend is sustainable, relative to its net profit after tax. In the last year, Umang Dairies paid out 32% of its profit as dividends. This is a middling range that strikes a nice balance between paying dividends to shareholders, and retaining enough earnings to invest in future growth. One of the risks is that management reinvests the retained capital poorly instead of paying a higher dividend.

Consider getting our latest analysis on Umang Dairies's financial position here.

Dividend Volatility

Before buying a stock for its income, we want to see if the dividends have been stable in the past, and if the company has a track record of maintaining its dividend. Umang Dairies has been paying a dividend for the past seven years. It's good to see that Umang Dairies has been paying a dividend for a number of years. However, the dividend has been cut at least once in the past, and we're concerned that what has been cut once, could be cut again. During the past seven-year period, the first annual payment was ₹0.75 in 2013, compared to ₹0.50 last year. The dividend has shrunk at around 5.6% a year during that period. Umang Dairies's dividend hasn't shrunk linearly at 5.6% per annum, but the CAGR is a useful estimate of the historical rate of change.

We struggle to make a case for buying Umang Dairies for its dividend, given that payments have shrunk over the past seven years.

Dividend Growth Potential

With a relatively unstable dividend, and a poor history of shrinking dividends, it's even more important to see if EPS are growing. Over the past five years, it looks as though Umang Dairies's EPS have declined at around 11% a year. With this kind of significant decline, we always wonder what has changed in the business. Dividends are about stability, and Umang Dairies's earnings per share, which support the dividend, have been anything but stable.

Conclusion

When we look at a dividend stock, we need to form a judgement on whether the dividend will grow, if the company is able to maintain it in a wide range of economic circumstances, and if the dividend payout is sustainable. We're glad to see Umang Dairies has a low payout ratio, as this suggests earnings are being reinvested in the business. Second, earnings per share have been in decline, and its dividend has been cut at least once in the past. Umang Dairies might not be a bad business, but it doesn't show all of the characteristics we look for in a dividend stock.

Now, if you want to look closer, it would be worth checking out our free research on Umang Dairies management tenure, salary, and performance.

Looking for more high-yielding dividend ideas? Try our curated list of dividend stocks with a yield above 3%.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About NSEI:UMANGDAIRY

Slight and overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

A case for TSXV:USA to reach USD $5.00 - $9.00 (CAD $7.30–$12.29) by 2029.

Fair Value CA$12.29|91.2% undervalued

AG

Community Contributor

DLocal's Future Growth Fueled by 35% Revenue and Profit Margin Boosts

Fair Value US$195.39|94.1% undervalued

WY

Community Contributor

Historically Cheap, but the Margin of Safety Is Still Thin

Fair Value SEK 232.58|13.2% undervalued

MA

Community Contributor