Advertisement

- United States

- /

- Specialty Stores

- /

- NasdaqGS:TSCO

Is Tractor Supply Company (NASDAQ:TSCO) Potentially Undervalued?

Tractor Supply Company (NASDAQ:TSCO), which is in the specialty retail business, and is based in United States, saw a double-digit share price rise of over 10% in the past couple of months on the NASDAQGS. As a mid-cap stock with high coverage by analysts, you could assume any recent changes in the company’s outlook is already priced into the stock. However, what if the stock is still a bargain? Today I will analyse the most recent data on Tractor Supply’s outlook and valuation to see if the opportunity still exists.

View our latest analysis for Tractor Supply

Is Tractor Supply still cheap?

Great news for investors – Tractor Supply is still trading at a fairly cheap price. According to my valuation, the intrinsic value for the stock is $112.46, which is above what the market is valuing the company at the moment. This indicates a potential opportunity to buy low. Tractor Supply’s share price also seems relatively stable compared to the rest of the market, as indicated by its low beta. If you believe the share price should eventually reach its true value, a low beta could suggest it is unlikely to rapidly do so anytime soon, and once it’s there, it may be hard to fall back down into an attractive buying range.

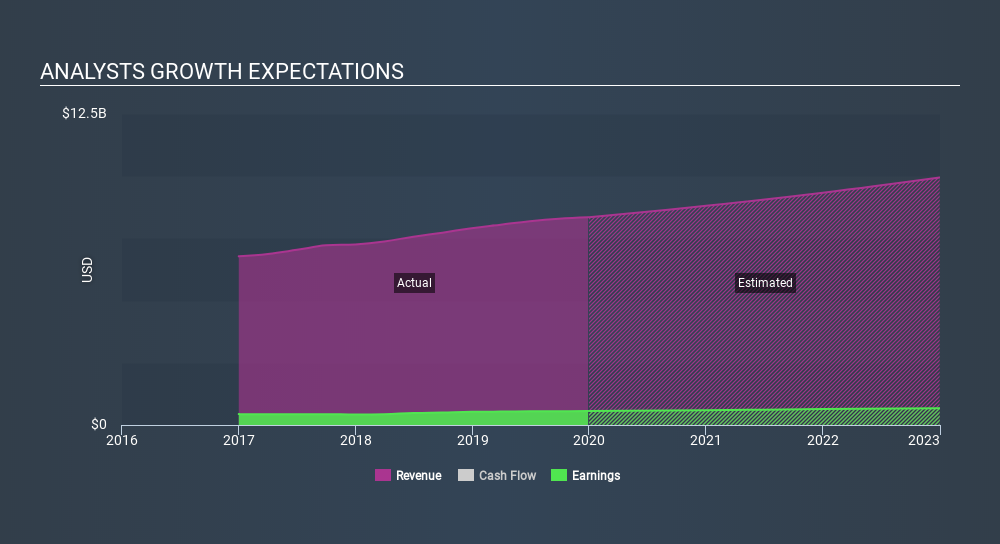

Can we expect growth from Tractor Supply?

Future outlook is an important aspect when you’re looking at buying a stock, especially if you are an investor looking for growth in your portfolio. Although value investors would argue that it’s the intrinsic value relative to the price that matter the most, a more compelling investment thesis would be high growth potential at a cheap price. Tractor Supply’s earnings growth are expected to be in the teens in the upcoming years, indicating a solid future ahead. This should lead to robust cash flows, feeding into a higher share value.

What this means for you:

Are you a shareholder? Since TSCO is currently undervalued, it may be a great time to increase your holdings in the stock. With a positive outlook on the horizon, it seems like this growth has not yet been fully factored into the share price. However, there are also other factors such as capital structure to consider, which could explain the current undervaluation.

Are you a potential investor? If you’ve been keeping an eye on TSCO for a while, now might be the time to enter the stock. Its buoyant future outlook isn’t fully reflected in the current share price yet, which means it’s not too late to buy TSCO. But before you make any investment decisions, consider other factors such as the track record of its management team, in order to make a well-informed buy.

Price is just the tip of the iceberg. Dig deeper into what truly matters – the fundamentals – before you make a decision on Tractor Supply. You can find everything you need to know about Tractor Supply in the latest infographic research report. If you are no longer interested in Tractor Supply, you can use our free platform to see my list of over 50 other stocks with a high growth potential.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About NasdaqGS:TSCO

Tractor Supply

Operates as a rural lifestyle retailer in the United States.

Average dividend payer and fair value.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Giftify ·

Giftify ($GIFT): A Small-Cap Incentives Platform with More ScaleThan Its Valuation Suggests

Fair Value:US$2.551.6% undervalued

15 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

TR

tripledub on Meta Platforms ·

The $135 Billion Bet That Should Make Every Shareholder Nervous

Fair Value:US$58016.4% overvalued

27 followersusers have followed this narrative

3 commentsusers have commented on this narrative

26 likesusers have liked this narrative

TH

TheBestInvestor on Lockheed Martin ·

Orbit + Aero + Defense

Fair Value:US$673.8823.8% undervalued

14 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on Steppe Gold ·

A case for Steppe Gold, bear case CAD $4, base case CAD $15, bull case CAD $25

Fair Value:CA$2594.4% undervalued

21 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Recently Updated Narratives

DA

davidlsander on Ubisoft Entertainment ·

Is Ubisoft the Market’s Biggest Pricing Error? Why Forensic Value Points to €33 Per Share

Fair Value:€33.886.0% undervalued

78 followersusers have followed this narrative

7 commentsusers have commented on this narrative

1 likeusers have liked this narrative

RO

RockeTeller on Thor Explorations ·

West Africa's 20 Baggers Gold Play (Nigeria/Senegal)

Fair Value:CA$3295.7% undervalued

11 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

WH

Whiskas24 on Objective ·

High-quality GovTech with a real moat but not enough upside yet

Fair Value:AU$15.121.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TR

tripledub on Microsoft ·

Everyone's Terrified Microsoft Will Keep Spending. I'm Terrified They'll Stop.

Fair Value:US$3957.5% overvalued

52 followersusers have followed this narrative

3 commentsusers have commented on this narrative

43 likesusers have liked this narrative

KI

Kingman1152 on NVIDIA ·

NVIDIA will see a profit margin surge of 55% in the next 5 years

Fair Value:US$305.231.8% undervalued

65 followersusers have followed this narrative

1 commentusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$579.5726.7% undervalued

1387 followersusers have followed this narrative

2 commentsusers have commented on this narrative

11 likesusers have liked this narrative

Trending Discussion

TA

Taurustunez88 on Dangote Sugar Refinery ·

With the N500b rights issue, I believe Dangote sugar refinery’s loss due to FX pressures will be dra...

1

|0

CL

Claysikes on Taiwan Semiconductor Manufacturing ·

Geopolitical risks balance a monopoly with current and future demand - Pricing in that risk is the c...

0

|0