Advertisement

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk. It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, Sheung Yue Group Holdings Limited (HKG:1633) does carry debt. But the more important question is: how much risk is that debt creating?

When Is Debt Dangerous?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

Check out our latest analysis for Sheung Yue Group Holdings

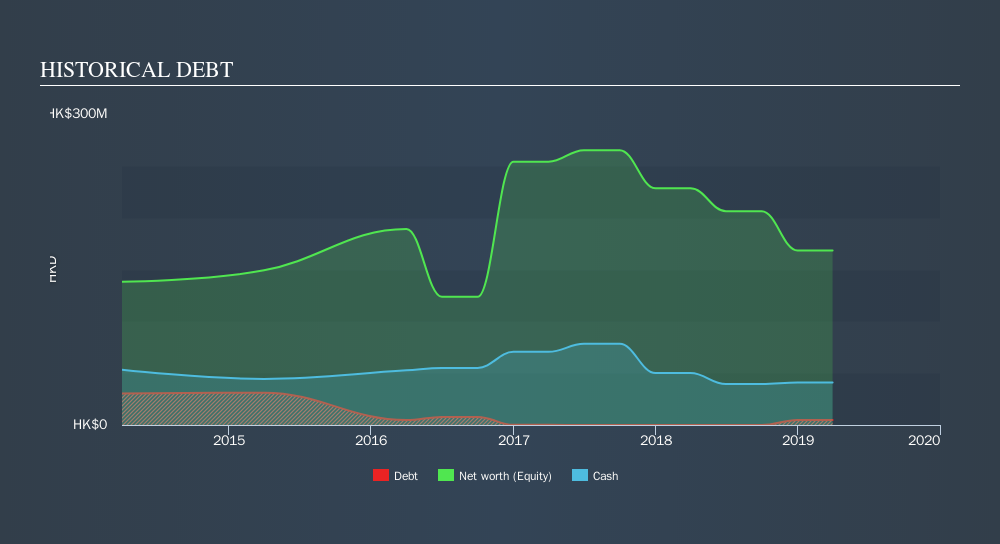

What Is Sheung Yue Group Holdings's Debt?

As you can see below, at the end of March 2019, Sheung Yue Group Holdings had HK$4.37m of debt, up from HK$2.32m a year ago. Click the image for more detail. However, it does have HK$41.0m in cash offsetting this, leading to net cash of HK$36.6m.

How Strong Is Sheung Yue Group Holdings's Balance Sheet?

According to the balance sheet data, Sheung Yue Group Holdings had liabilities of HK$59.0m due within 12 months, but no longer term liabilities. On the other hand, it had cash of HK$41.0m and HK$105.1m worth of receivables due within a year. So it actually has HK$87.1m more liquid assets than total liabilities.

This surplus strongly suggests that Sheung Yue Group Holdings has a rock-solid balance sheet (and the debt is of no concern whatsoever). With this in mind one could posit that its balance sheet is as strong as beautiful a rare rhino. Simply put, the fact that Sheung Yue Group Holdings has more cash than debt is arguably a good indication that it can manage its debt safely. There's no doubt that we learn most about debt from the balance sheet. But it is Sheung Yue Group Holdings's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Over 12 months, Sheung Yue Group Holdings reported revenue of HK$242m, which is a gain of 9.7%, although it did not report any earnings before interest and tax. We usually like to see faster growth from unprofitable companies, but each to their own.

So How Risky Is Sheung Yue Group Holdings?

We have no doubt that loss making companies are, in general, riskier than profitable ones. And we do note that Sheung Yue Group Holdings had negative earnings before interest and tax (EBIT), over the last year. And over the same period it saw negative free cash outflow of HK$16m and booked a HK$45m accounting loss. But at least it has HK$36.6m on the balance sheet to spend on growth, near-term. Even though its balance sheet seems sufficiently liquid, debt always makes us a little nervous if a company doesn't produce free cash flow regularly. For riskier companies like Sheung Yue Group Holdings I always like to keep an eye on the long term profit and revenue trends. Fortunately, you can click to see our interactive graph of its profit, revenue, and operating cashflow.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About SEHK:1633

Sheung Yue Group Holdings

An investment holding company, provides foundation work services to private and public sectors in Hong Kong and Macau.

Adequate balance sheet very low.

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|33.3% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|23.4% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|8.5% overvalued

DA

Community Contributor