Advertisement

- Australia

- /

- Electrical

- /

- ASX:RFT

Is Rectifier Technologies (ASX:RFT) Using Too Much Debt?

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital. It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that Rectifier Technologies Limited (ASX:RFT) does use debt in its business. But the real question is whether this debt is making the company risky.

What Risk Does Debt Bring?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we think about a company's use of debt, we first look at cash and debt together.

View our latest analysis for Rectifier Technologies

What Is Rectifier Technologies's Net Debt?

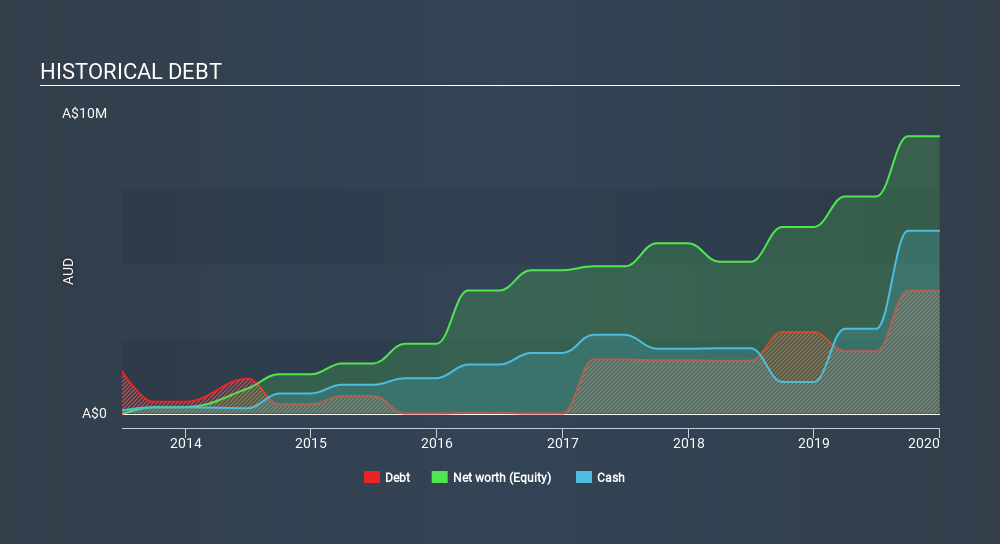

The image below, which you can click on for greater detail, shows that at December 2019 Rectifier Technologies had debt of AU$3.55m, up from AU$2.72m in one year. However, it does have AU$6.10m in cash offsetting this, leading to net cash of AU$2.55m.

How Strong Is Rectifier Technologies's Balance Sheet?

We can see from the most recent balance sheet that Rectifier Technologies had liabilities of AU$4.61m falling due within a year, and liabilities of AU$3.74m due beyond that. Offsetting these obligations, it had cash of AU$6.10m as well as receivables valued at AU$3.02m due within 12 months. So it actually has AU$762.3k more liquid assets than total liabilities.

This state of affairs indicates that Rectifier Technologies's balance sheet looks quite solid, as its total liabilities are just about equal to its liquid assets. So while it's hard to imagine that the AU$54.7m company is struggling for cash, we still think it's worth monitoring its balance sheet. Simply put, the fact that Rectifier Technologies has more cash than debt is arguably a good indication that it can manage its debt safely.

Even more impressive was the fact that Rectifier Technologies grew its EBIT by 134% over twelve months. That boost will make it even easier to pay down debt going forward. The balance sheet is clearly the area to focus on when you are analysing debt. But it is Rectifier Technologies's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. Rectifier Technologies may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. In the last three years, Rectifier Technologies created free cash flow amounting to 4.8% of its EBIT, an uninspiring performance. That limp level of cash conversion undermines its ability to manage and pay down debt.

Summing up

While we empathize with investors who find debt concerning, you should keep in mind that Rectifier Technologies has net cash of AU$2.55m, as well as more liquid assets than liabilities. And we liked the look of last year's 134% year-on-year EBIT growth. So we don't think Rectifier Technologies's use of debt is risky. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. Be aware that Rectifier Technologies is showing 2 warning signs in our investment analysis , you should know about...

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

Love or hate this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned. Thank you for reading.

About ASX:RFT

Rectifier Technologies

Designs and manufactures power rectifiers in Australia, Asia, North America, South America, Europe, and Oceania.

Mediocre balance sheet with low risk.

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Upside Gold ·

An Undervalued 3.3Moz Gold Project in Canada

Fair Value:CA$5.0775.1% undervalued

139 followersusers have followed this narrative

1 commentusers have commented on this narrative

22 likesusers have liked this narrative

YA

Yang_ on SoFi Technologies ·

SoFi Technologies: The Apex Aggregator and the Infrastructure of the Modern Financial System

Fair Value:US$22.9822.7% undervalued

44 followersusers have followed this narrative

0 commentsusers have commented on this narrative

33 likesusers have liked this narrative

KO

Kouj on CSL ·

CSL: The Dip Is the Opportunity

Fair Value:AU$1559.3% undervalued

19 followersusers have followed this narrative

0 commentsusers have commented on this narrative

15 likesusers have liked this narrative

GA

GavrielH on DHT Holdings ·

DHT Holdings, inc: Strait of Hormuz Risk Amidst US-Israel vs Iran Tensions Spikes VLCC Rates.

Fair Value:US$3653.2% undervalued

15 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Recently Updated Narratives

BI

Bigd on Volatus Aerospace ·

Strong buy

Fair Value:CA$1.0521.9% undervalued

7 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

VE

Vestra on Costco Wholesale ·

Costco Wholesale Corp (COST): Operational Moats and the Membership Flywheel

Fair Value:US$1.09k7.1% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VE

Vestra on Alibaba Group Holding ·

Alibaba Group Holding Ltd (BABA): The Agentic AI Shift and "OpenClaw" Transformation

Fair Value:US$199.6132.3% undervalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

KA

kabz2342 on Nu Holdings ·

Nu holdings will continue to disrupt the South American banking market

Fair Value:US$64.378.4% undervalued

53 followersusers have followed this narrative

3 commentsusers have commented on this narrative

29 likesusers have liked this narrative

YA

Yang_ on SoFi Technologies ·

SoFi Technologies: The Apex Aggregator and the Infrastructure of the Modern Financial System

Fair Value:US$22.9822.7% undervalued

44 followersusers have followed this narrative

0 commentsusers have commented on this narrative

33 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$59633.6% undervalued

1310 followersusers have followed this narrative

2 commentsusers have commented on this narrative

10 likesusers have liked this narrative

Trending Discussion

DA

daqui_luis on Corticeira Amorim S.G.P.S ·

Great analysis on a great and solid company with a dominant position in the Cork Market.

1

|0