Advertisement

Greg Yull became the CEO of Intertape Polymer Group Inc. (TSE:ITP) in 2010. First, this article will compare CEO compensation with compensation at similar sized companies. Then we'll look at a snap shot of the business growth. And finally we will reflect on how common stockholders have fared in the last few years, as a secondary measure of performance. The aim of all this is to consider the appropriateness of CEO pay levels.

View our latest analysis for Intertape Polymer Group

How Does Greg Yull's Compensation Compare With Similar Sized Companies?

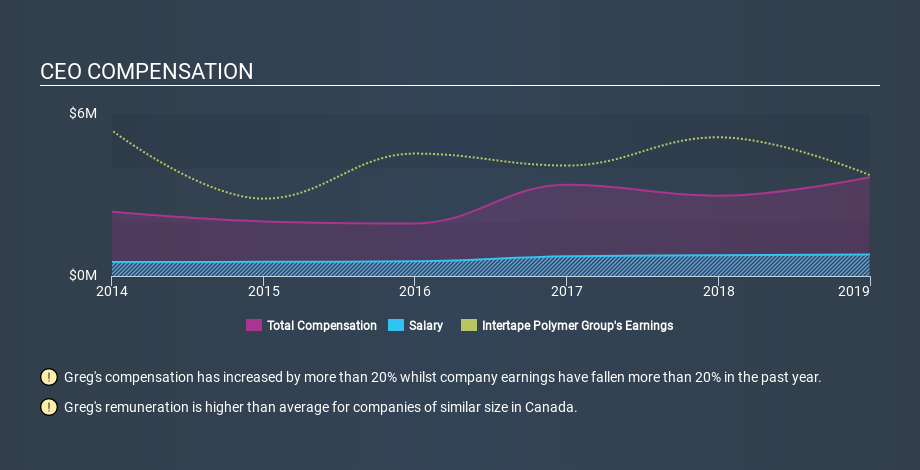

Our data indicates that Intertape Polymer Group Inc. is worth CA$973m, and total annual CEO compensation was reported as US$3.7m for the year to December 2018. While we always look at total compensation first, we note that the salary component is less, at US$800k. We note that more than half of the total compensation is not the salary; and performance requirements may apply to this non-salary portion. We examined companies with market caps from US$400m to US$1.6b, and discovered that the median CEO total compensation of that group was US$1.6m.

Thus we can conclude that Greg Yull receives more in total compensation than the median of a group of companies in the same market, and of similar size to Intertape Polymer Group Inc.. However, this doesn't necessarily mean the pay is too high. A closer look at the performance of the underlying business will give us a better idea about whether the pay is particularly generous.

You can see, below, how CEO compensation at Intertape Polymer Group has changed over time.

Is Intertape Polymer Group Inc. Growing?

On average over the last three years, Intertape Polymer Group Inc. has shrunk earnings per share by 7.1% each year (measured with a line of best fit). In the last year, its revenue is up 15%.

Sadly for shareholders, earnings per share are actually down, over three years. While the revenue growth is good to see, it is outweighed by the fact that earnings per share are down, over three years. These factors suggest that the business performance wouldn't really justify a high pay packet for the CEO. You might want to check this free visual report on analyst forecasts for future earnings.

Has Intertape Polymer Group Inc. Been A Good Investment?

Given the total loss of 23% over three years, many shareholders in Intertape Polymer Group Inc. are probably rather dissatisfied, to say the least. This suggests it would be unwise for the company to pay the CEO too generously.

In Summary...

We compared total CEO remuneration at Intertape Polymer Group Inc. with the amount paid at companies with a similar market capitalization. As discussed above, we discovered that the company pays more than the median of that group.

Earnings per share have not grown in three years, and the revenue growth fails to impress us. Just as bad, share price gains for investors have failed to materialize, over the same period. In our opinion the CEO might be paid too generously! Whatever your view on compensation, you might want to check if insiders are buying or selling Intertape Polymer Group shares (free trial).

Important note: Intertape Polymer Group may not be the best stock to buy. You might find something better in this list of interesting companies with high ROE and low debt.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About TSX:ITP

Intertape Polymer Group

Intertape Polymer Group Inc. provides packaging and protective solutions for the industrial markets in North America, Europe, and internationally.

Undervalued with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Eva Live ·

This small cap is building the AI workforce of the future

Fair Value:US$7.4353.2% undervalued

71 followersusers have followed this narrative

0 commentsusers have commented on this narrative

15 likesusers have liked this narrative

TR

tripledub on lululemon athletica ·

Lululemon Got Boring Right About the Time It Got Cheap. That's Usually the Point

Fair Value:US$22043.1% undervalued

20 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative

WO

woodworthfund on Kraft Heinz ·

Kraft Heinz (KHC): Less Drama, More Ketchup

Fair Value:US$3532.8% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

CA

Canderous on PetroTal ·

Beyond 2026, Beyond a Double

Fair Value:CA$1.8168.5% undervalued

23 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

Recently Updated Narratives

IV

Ivoed on OCI ·

OCI is not being priced on asset value. That is the opportunity.

Fair Value:€6.5643.8% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

IV

Ivoed on Kinepolis Group ·

Kinepolis Group Set to Achieve 22.52% Revenue Growth Boost, Experts Dream

Fair Value:€4839.0% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

IV

Ivoed on Salesforce ·

Salesforce Future Value Could Reach $263 as Market Remains Short-Sighted

Fair Value:US$26331.5% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8591.0% undervalued

114 followersusers have followed this narrative

2 commentsusers have commented on this narrative

31 likesusers have liked this narrative

TR

tripledub on Meta Platforms ·

The $135 Billion Bet That Should Make Every Shareholder Nervous

Fair Value:US$74018.2% undervalued

39 followersusers have followed this narrative

3 commentsusers have commented on this narrative

33 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$268.6116.8% undervalued

1187 followersusers have followed this narrative

7 commentsusers have commented on this narrative

34 likesusers have liked this narrative