Advertisement

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. As with many other companies GOME Retail Holdings Limited (HKG:493) makes use of debt. But should shareholders be worried about its use of debt?

When Is Debt A Problem?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

Check out our latest analysis for GOME Retail Holdings

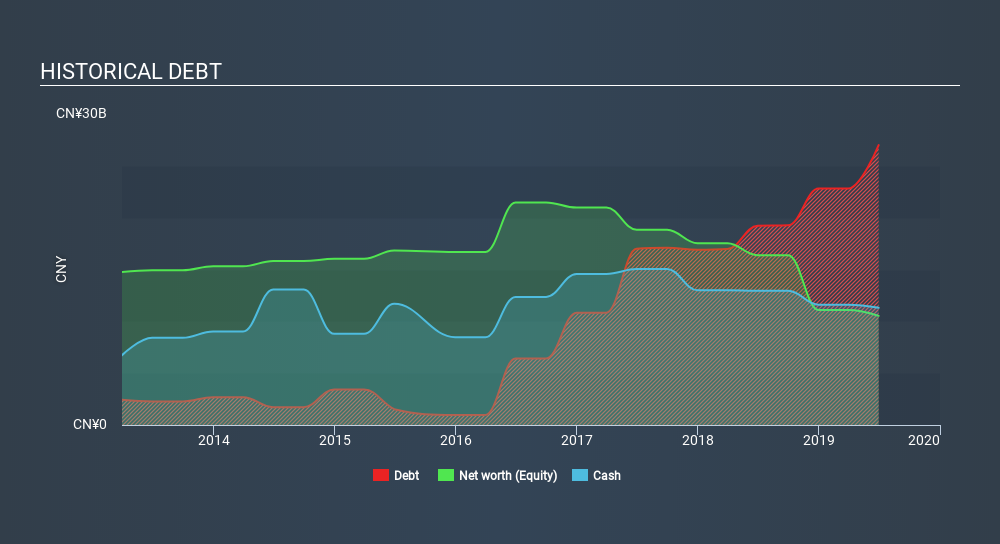

What Is GOME Retail Holdings's Net Debt?

You can click the graphic below for the historical numbers, but it shows that as of June 2019 GOME Retail Holdings had CN¥27.0b of debt, an increase on CN¥19.2b, over one year. However, it also had CN¥11.3b in cash, and so its net debt is CN¥15.7b.

A Look At GOME Retail Holdings's Liabilities

We can see from the most recent balance sheet that GOME Retail Holdings had liabilities of CN¥50.2b falling due within a year, and liabilities of CN¥17.7b due beyond that. Offsetting this, it had CN¥11.3b in cash and CN¥2.34b in receivables that were due within 12 months. So its liabilities total CN¥54.2b more than the combination of its cash and short-term receivables.

The deficiency here weighs heavily on the CN¥16.5b company itself, as if a child were struggling under the weight of an enormous back-pack full of books, his sports gear, and a trumpet. So we'd watch its balance sheet closely, without a doubt. At the end of the day, GOME Retail Holdings would probably need a major re-capitalization if its creditors were to demand repayment. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if GOME Retail Holdings can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

In the last year GOME Retail Holdings had negative earnings before interest and tax, and actually shrunk its revenue by 6.2%, to CN¥64b. We would much prefer see growth.

Caveat Emptor

Over the last twelve months GOME Retail Holdings produced an earnings before interest and tax (EBIT) loss. Its EBIT loss was a whopping CN¥3.2b. Combining this information with the significant liabilities we already touched on makes us very hesitant about this stock, to say the least. That said, it is possible that the company will turn its fortunes around. But we think that is unlikely, given it is low on liquid assets, and burned through CN¥2.8b in the last year. So we consider this a high risk stock and we wouldn't be at all surprised if the company asks shareholders for money before long. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. To that end, you should be aware of the 1 warning sign we've spotted with GOME Retail Holdings .

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About SEHK:493

GOME Retail Holdings

Operates and manages retail stores in the People’s Republic of China.

Low with imperfect balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

Vita Life Sciences Set for a 12.72% Revenue Growth While Tackling Operational Challenges

Fair Value AU$2.42|9.5% undervalued

RO

Community Contributor

Vossloh rides a €500 billion wave to boost growth and earnings in the next decade

Fair Value €78.41|7.2% undervalued

CH

Community Contributor

Intuitive Surgical Will Transform Healthcare with 12% Revenue Growth

Fair Value US$325.55|56.5% overvalued

UN

Community Contributor