Advertisement

Want to participate in a short research study? Help shape the future of investing tools and you could win a $250 gift card!

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. As with many other companies. GenMark Diagnostics, Inc. (NASDAQ:GNMK) makes use of debt. But the real question is whether this debt is making the company risky.

What Risk Does Debt Bring?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

View our latest analysis for GenMark Diagnostics

How Much Debt Does GenMark Diagnostics Carry?

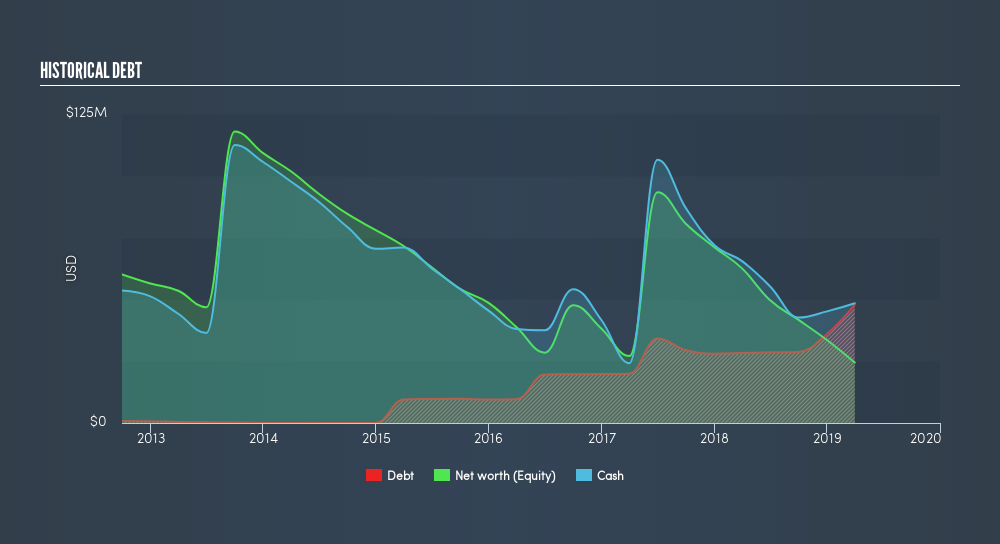

The image below, which you can click on for greater detail, shows that at March 2019 GenMark Diagnostics had debt of US$47.8m, up from US$28.3m in one year. However, its balance sheet shows it holds US$48.4m in cash, so it actually has US$601.0k net cash.

A Look At GenMark Diagnostics's Liabilities

According to the last reported balance sheet, GenMark Diagnostics had liabilities of US$17.7m due within 12 months, and liabilities of US$54.5m due beyond 12 months. Offsetting this, it had US$48.4m in cash and US$9.17m in receivables that were due within 12 months. So its liabilities total US$14.6m more than the combination of its cash and short-term receivables.

Given GenMark Diagnostics has a market capitalization of US$361.0m, it's hard to believe these liabilities pose much threat. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward. GenMark Diagnostics boasts net cash, so it's fair to say it does not have a heavy debt load! There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine GenMark Diagnostics's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

In the last year GenMark Diagnostics managed to grow its revenue by 18%, to US$72m. We usually like to see faster growth from unprofitable companies, but each to their own.

So How Risky Is GenMark Diagnostics?

Statistically speaking companies that lose money are riskier than those that make money. And in the last year GenMark Diagnostics had negative earnings before interest and tax (EBIT), truth be told. Indeed, in that time it burnt through US$37m of cash and made a loss of US$51m. However, it has net cash of US$48m, so it has a bit of time before it will need more capital. Overall, we'd say the stock is a bit risky, and we're usually very cautious until we see positive free cash flow. For riskier companies like GenMark Diagnostics I always like to keep an eye on whether insiders are buying or selling. So click here if you want to find out for yourself.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|33.3% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|23.4% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|8.5% overvalued

DA

Community Contributor