Advertisement

- Singapore

- /

- Real Estate

- /

- SGX:ADN

Is First Sponsor Group (SGX:ADN) A Risky Investment?

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital. It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that First Sponsor Group Limited (SGX:ADN) does use debt in its business. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

Check out our latest analysis for First Sponsor Group

How Much Debt Does First Sponsor Group Carry?

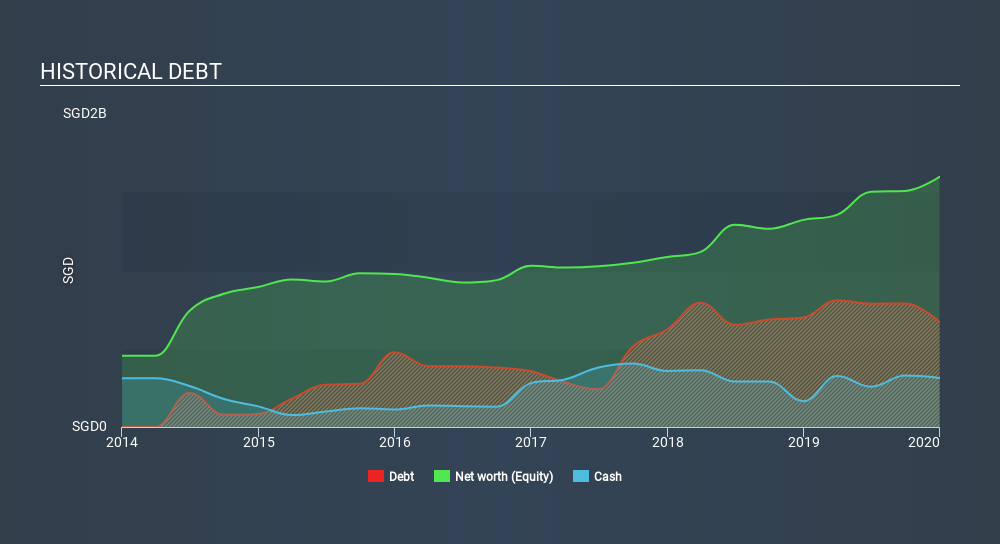

You can click the graphic below for the historical numbers, but it shows that First Sponsor Group had S$670.6m of debt in December 2019, down from S$699.3m, one year before. However, it does have S$313.4m in cash offsetting this, leading to net debt of about S$357.2m.

A Look At First Sponsor Group's Liabilities

Zooming in on the latest balance sheet data, we can see that First Sponsor Group had liabilities of S$663.3m due within 12 months and liabilities of S$498.7m due beyond that. Offsetting this, it had S$313.4m in cash and S$353.2m in receivables that were due within 12 months. So its liabilities total S$495.4m more than the combination of its cash and short-term receivables.

First Sponsor Group has a market capitalization of S$1.06b, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. However, it is still worthwhile taking a close look at its ability to pay off debt.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

First Sponsor Group's net debt to EBITDA ratio of about 2.2 suggests only moderate use of debt. And its strong interest cover of 1k times, makes us even more comfortable. We saw First Sponsor Group grow its EBIT by 6.7% in the last twelve months. Whilst that hardly knocks our socks off it is a positive when it comes to debt. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine First Sponsor Group's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So we always check how much of that EBIT is translated into free cash flow. During the last three years, First Sponsor Group burned a lot of cash. While investors are no doubt expecting a reversal of that situation in due course, it clearly does mean its use of debt is more risky.

Our View

First Sponsor Group's conversion of EBIT to free cash flow and level of total liabilities definitely weigh on it, in our esteem. But the good news is it seems to be able to cover its interest expense with its EBIT with ease. Taking the abovementioned factors together we do think First Sponsor Group's debt poses some risks to the business. While that debt can boost returns, we think the company has enough leverage now. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. For instance, we've identified 2 warning signs for First Sponsor Group that you should be aware of.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About SGX:ADN

First Sponsor Group

An investment holding company, invests in, develops, and sells residential and commercial properties in the People’s Republic of China, Europe, and internationally.

Reasonable growth potential second-rate dividend payer.

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Conexeu Sciences ·

This small biotech is developing technology that could potentially change how tissue is rebuilt

Fair Value:US$25.3451.9% undervalued

50 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

HE

HedgeY on Quanta Services ·

The Picks-and-Shovels Leader of the Grid Supercycle

Fair Value:US$7104.2% overvalued

52 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

FU

FundamentalFlow on Karman Holdings ·

KRMN — Karman Space & Defense: Down 58% from Peak, Is the Market Mispricing a Hypergrowth Defense Compounder?

Fair Value:US$105.654.8% undervalued

34 followersusers have followed this narrative

2 commentsusers have commented on this narrative

16 likesusers have liked this narrative

DO

Double_Bubbler on Invinity Energy Systems ·

Invinity Energy Systems: All About That BESS

Fair Value:UK£161.9% undervalued

40 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

Recently Updated Narratives

AS

AstrisCorporateAdvisory on INTLOOP ·

Renewed focus on business investment

Fair Value:JP¥4.17k61.0% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

GE

Germaine on Hartanah Kenyalang Berhad ·

Hartanah Kenyalang Berhad (Bursa: 0359): A Hidden Gem in the Malaysian Construction Sector?

Fair Value:RM 0.13419.2% overvalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

JA

Jacobm2488123 on Netflix ·

Netflix's Revenue Surge Will Hit 18% Despite Market Lows

Fair Value:US$115.9137.1% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7443.8% undervalued

67 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9639.1% undervalued

61 followersusers have followed this narrative

9 commentsusers have commented on this narrative

17 likesusers have liked this narrative

HE

HedgeY on AST SpaceMobile ·

AST SpaceMobile: The Boldest Direct-to-Cell Bet in Public Markets

Fair Value:US$17056.9% undervalued

51 followersusers have followed this narrative

0 commentsusers have commented on this narrative

13 likesusers have liked this narrative