Advertisement

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about. It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that Electrozink Open Joint-Stock Company (MCX:ELTZ) does use debt in its business. But is this debt a concern to shareholders?

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

See our latest analysis for Electrozink

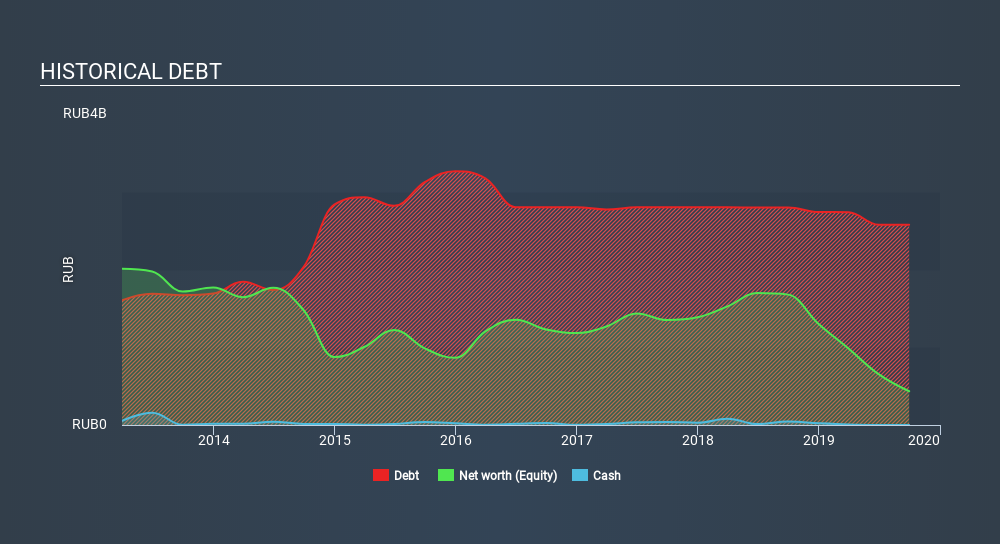

How Much Debt Does Electrozink Carry?

You can click the graphic below for the historical numbers, but it shows that Electrozink had ₽2.58b of debt in September 2019, down from ₽2.80b, one year before. Net debt is about the same, since the it doesn't have much cash.

A Look At Electrozink's Liabilities

According to the last reported balance sheet, Electrozink had liabilities of ₽3.48b due within 12 months, and liabilities of ₽65.2m due beyond 12 months. Offsetting these obligations, it had cash of ₽268.0k as well as receivables valued at ₽457.4m due within 12 months. So its liabilities total ₽3.09b more than the combination of its cash and short-term receivables.

The deficiency here weighs heavily on the ₽210.6m company itself, as if a child were struggling under the weight of an enormous back-pack full of books, his sports gear, and a trumpet. So we'd watch its balance sheet closely, without a doubt. After all, Electrozink would likely require a major re-capitalisation if it had to pay its creditors today. When analysing debt levels, the balance sheet is the obvious place to start. But it is Electrozink's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Over 12 months, Electrozink made a loss at the EBIT level, and saw its revenue drop to ₽1.3b, which is a fall of 76%. That makes us nervous, to say the least.

Caveat Emptor

Not only did Electrozink's revenue slip over the last twelve months, but it also produced negative earnings before interest and tax (EBIT). Indeed, it lost a very considerable ₽2.2b at the EBIT level. Reflecting on this and the significant total liabilities, it's hard to know what to say about the stock because of our intense dis-affinity for it. Sure, the company might have a nice story about how they are going on to a brighter future. But the reality is that it is low on liquid assets relative to liabilities, and it lost ₽1.2b in the last year. So we're about as excited about owning this stock as hiking up a snowy mountain with wet socks on in the rain. It's too risky for us. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. Like risks, for instance. Every company has them, and we've spotted 4 warning signs for Electrozink (of which 2 can't be ignored!) you should know about.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About MISX:ELTZ

Electrozink

Electrozink Public Joint-Stock Company produces and sells various non-ferrous metallurgy products in Russia.

Good value with worrying balance sheet.

Market Insights

Advertisement

Community Narratives

Vita Life Sciences Set for a 12.72% Revenue Growth While Tackling Operational Challenges

Fair Value AU$2.42|8.7% undervalued

RO

Community Contributor

Vossloh rides a €500 billion wave to boost growth and earnings in the next decade

Fair Value €78.41|6.3% undervalued

CH

Community Contributor

Intuitive Surgical Will Transform Healthcare with 12% Revenue Growth

Fair Value US$325.55|56.5% overvalued

UN

Community Contributor