Advertisement

- United States

- /

- Aerospace & Defense

- /

- NYSE:DCO

Is Ducommun Incorporated's (NYSE:DCO) High P/E Ratio A Problem For Investors?

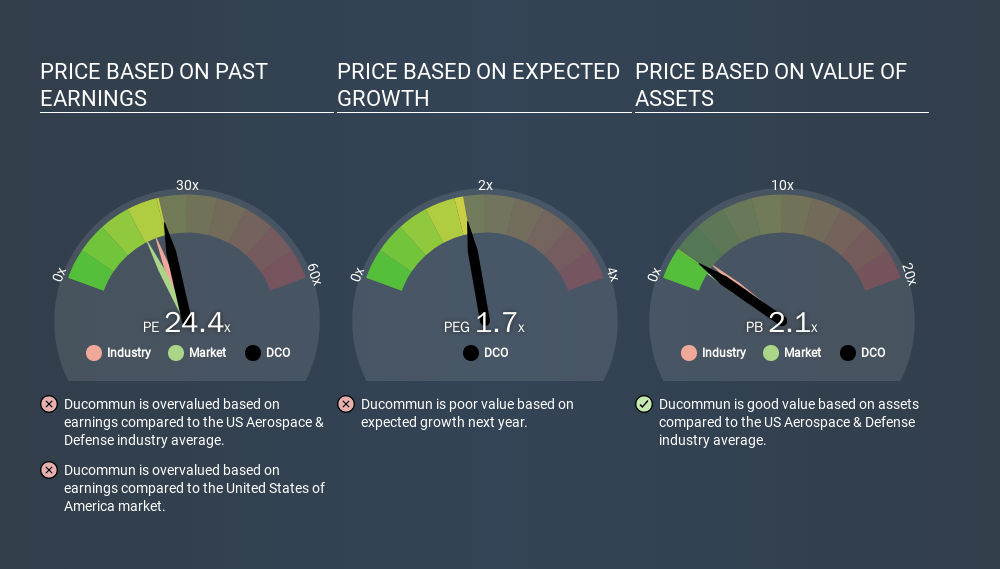

This article is for investors who would like to improve their understanding of price to earnings ratios (P/E ratios). We'll apply a basic P/E ratio analysis to Ducommun Incorporated's (NYSE:DCO), to help you decide if the stock is worth further research. Ducommun has a price to earnings ratio of 24.45, based on the last twelve months. That is equivalent to an earnings yield of about 4.1%.

View our latest analysis for Ducommun

How Do I Calculate A Price To Earnings Ratio?

The formula for P/E is:

Price to Earnings Ratio = Price per Share ÷ Earnings per Share (EPS)

Or for Ducommun:

P/E of 24.45 = $51.67 ÷ $2.11 (Based on the year to September 2019.)

Is A High Price-to-Earnings Ratio Good?

A higher P/E ratio means that buyers have to pay a higher price for each $1 the company has earned over the last year. All else being equal, it's better to pay a low price -- but as Warren Buffett said, 'It's far better to buy a wonderful company at a fair price than a fair company at a wonderful price.

Does Ducommun Have A Relatively High Or Low P/E For Its Industry?

One good way to get a quick read on what market participants expect of a company is to look at its P/E ratio. The image below shows that Ducommun has a higher P/E than the average (21.2) P/E for companies in the aerospace & defense industry.

Its relatively high P/E ratio indicates that Ducommun shareholders think it will perform better than other companies in its industry classification. The market is optimistic about the future, but that doesn't guarantee future growth. So further research is always essential. I often monitor director buying and selling.

How Growth Rates Impact P/E Ratios

Generally speaking the rate of earnings growth has a profound impact on a company's P/E multiple. Earnings growth means that in the future the 'E' will be higher. That means unless the share price increases, the P/E will reduce in a few years. Then, a lower P/E should attract more buyers, pushing the share price up.

Notably, Ducommun grew EPS by a whopping 35% in the last year. And earnings per share have improved by 13% annually, over the last five years. I'd therefore be a little surprised if its P/E ratio was not relatively high.

Remember: P/E Ratios Don't Consider The Balance Sheet

It's important to note that the P/E ratio considers the market capitalization, not the enterprise value. In other words, it does not consider any debt or cash that the company may have on the balance sheet. Hypothetically, a company could reduce its future P/E ratio by spending its cash (or taking on debt) to achieve higher earnings.

Such spending might be good or bad, overall, but the key point here is that you need to look at debt to understand the P/E ratio in context.

Ducommun's Balance Sheet

Ducommun has net debt equal to 37% of its market cap. While it's worth keeping this in mind, it isn't a worry.

The Bottom Line On Ducommun's P/E Ratio

Ducommun trades on a P/E ratio of 24.4, which is above its market average of 18.6. While the company does use modest debt, its recent earnings growth is superb. So on this analysis a high P/E ratio seems reasonable.

Investors have an opportunity when market expectations about a stock are wrong. If the reality for a company is better than it expects, you can make money by buying and holding for the long term. So this free visualization of the analyst consensus on future earnings could help you make the right decision about whether to buy, sell, or hold.

But note: Ducommun may not be the best stock to buy. So take a peek at this free list of interesting companies with strong recent earnings growth (and a P/E ratio below 20).

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About NYSE:DCO

Ducommun

Provides engineering and manufacturing services for products and applications used in the aerospace and defense, industrial, medical, and other industries in the United States.

Excellent balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Optimi Health ·

The Only Psychedelic Company Already Selling MDMA and Psilocybin to Real Patients, Yet Priced Like It Doesn’t Exist

Fair Value:US$1158.7% undervalued

32 followersusers have followed this narrative

2 commentsusers have commented on this narrative

6 likesusers have liked this narrative

WE

WealthAP on Novo Nordisk ·

Novo Nordisk (NVO): Is the "Easy Growth" Story Over?

Fair Value:DKK 407.7721.6% undervalued

48 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

VA

ValueInvestingSubstack on Zoetis ·

Zoetis down -50% over the past year

Fair Value:US$92.9220.2% undervalued

14 followersusers have followed this narrative

0 commentsusers have commented on this narrative

7 likesusers have liked this narrative

CE

CentryResearch on Centrus Energy ·

Centrus Energy: The Next Nuclear Bottleneck Isn't Reactors. It's Fuel.

Fair Value:US$1908.3% undervalued

11 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

Recently Updated Narratives

AL

Alice3D on ServiceNow ·

NOW is an established SAAS positioned for accelerated growth over the next 5 years.

Fair Value:US$15538.4% undervalued

23 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

EP

Epstein_Research on Silver Storm Mining ·

Silver Storm Mining, oversold silver junior

Fair Value:CA$278.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

ST

StoxEurope on KBC Group ·

KBC Group (ENXTBR:KBC) Valuation Deep-Dive: Why Dividend and Book Value Models Point in Opposite Directions.

Fair Value:€116.944.9% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75029.1% undervalued

101 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

BE

benjamin_lvieq on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6514.6% undervalued

69 followersusers have followed this narrative

2 commentsusers have commented on this narrative

10 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5449.5% undervalued

64 followersusers have followed this narrative

3 commentsusers have commented on this narrative

11 likesusers have liked this narrative

Trending Discussion

ST

StoxEurope on Koninklijke Ahold Delhaize ·

I ran Ahold Delhaize through a three-model triangulation — DCF, dividend discount, and residual income — with every assumption published and tagged as fact or assumption. The interesting result isn't a number, it's a disagreement: the point estimates run from €20,03 (RIM) through €27,64 (DDM) to €64,91 (DCF), and the pairwise overlaps form two disjoint segments — €20,36–€21,54 and €39,60–€44,56. Between €21,54 and €39,60, no two of the three models agree. [img]https://staticm.fastcomments.com/1784197249786-1000x1000-ad-range-strip.png[/img] Most of the spread is lens properties rather than company drama. A dividend model structurally can't see the roughly half of shareholder returns Ahold pays through buybacks. The book is ~96 % goodwill from the 2016 merger, which pins the residual-income reading low. And ~83 % of the DCF's value sits beyond the explicit five years, so it leans hard on the terminal assumptions. Three honest lenses, three honest answers — the disagreement is the information. Disclosures Position disclosure: The author holds no position in Ahold Delhaize as at 9 July 2026. This valuation is a StoxEurope opinion, based on honest research. Mistakes are possible. This is not investment advice. Do your own research. This article demonstrates a valuation methodology. It is not an investment recommendation, is not personalised to any reader's circumstances, and every figure in it depends entirely on the stated assumptions

1

|0