Advertisement

- Italy

- /

- Other Utilities

- /

- BIT:A2A

Is A2A (BIT:A2A) Using Too Much Debt?

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital. It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. As with many other companies A2A S.p.A. (BIT:A2A) makes use of debt. But should shareholders be worried about its use of debt?

When Is Debt Dangerous?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first step when considering a company's debt levels is to consider its cash and debt together.

View 4 warning signs we detected for A2A

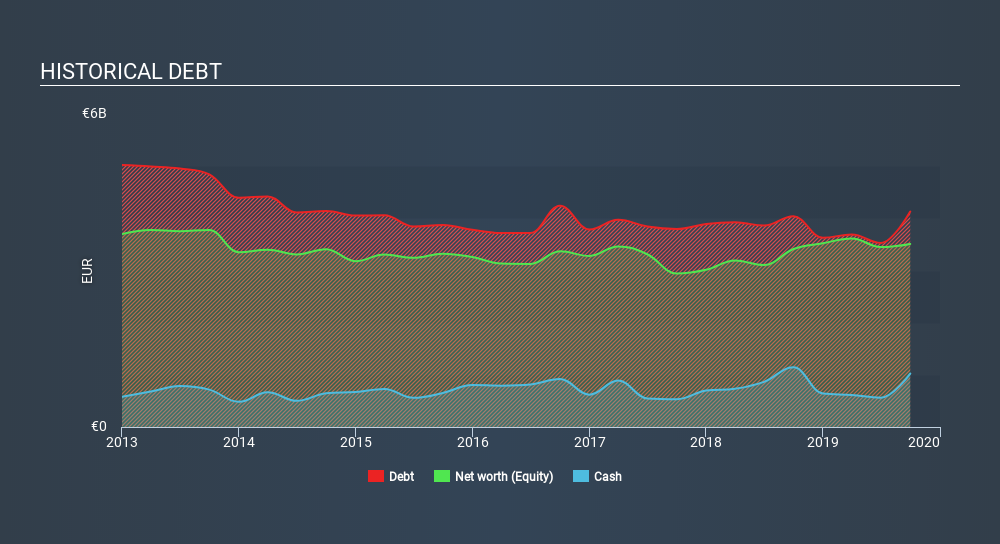

What Is A2A's Net Debt?

As you can see below, A2A had €4.10b of debt, at September 2019, which is about the same the year before. You can click the chart for greater detail. However, it also had €1.02b in cash, and so its net debt is €3.08b.

How Healthy Is A2A's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that A2A had liabilities of €2.76b due within 12 months and liabilities of €4.46b due beyond that. Offsetting these obligations, it had cash of €1.02b as well as receivables valued at €1.72b due within 12 months. So its liabilities total €4.48b more than the combination of its cash and short-term receivables.

This is a mountain of leverage relative to its market capitalization of €5.22b. Should its lenders demand that it shore up the balance sheet, shareholders would likely face severe dilution.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

A2A's debt is 2.6 times its EBITDA, and its EBIT cover its interest expense 5.8 times over. Taken together this implies that, while we wouldn't want to see debt levels rise, we think it can handle its current leverage. Unfortunately, A2A saw its EBIT slide 4.6% in the last twelve months. If that earnings trend continues then its debt load will grow heavy like the heart of a polar bear watching its sole cub. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine A2A's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Over the most recent three years, A2A recorded free cash flow worth 65% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This cold hard cash means it can reduce its debt when it wants to.

Our View

A2A's level of total liabilities and EBIT growth rate definitely weigh on it, in our esteem. But it seems to be able to convert EBIT to free cash flow without much trouble. We should also note that Integrated Utilities industry companies like A2A commonly do use debt without problems. We think that A2A's debt does make it a bit risky, after considering the aforementioned data points together. That's not necessarily a bad thing, since leverage can boost returns on equity, but it is something to be aware of. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. For example, we've discovered 4 warning signs for A2A (of which 1 is major) which any shareholder or potential investor should be aware of.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About BIT:A2A

A2A

Engages in the production, sale, and distribution of gas and electricity, and district heating in Italy and internationally.

Established dividend payer with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

VA

valuebull on Eva Live ·

Is this the AI replacing marketing professionals?

Fair Value:US$7.4349.5% undervalued

41 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

TR

tripledub on Microsoft ·

Everyone's Terrified Microsoft Will Keep Spending. I'm Terrified They'll Stop.

Fair Value:US$3956.3% undervalued

6 followersusers have followed this narrative

3 commentsusers have commented on this narrative

9 likesusers have liked this narrative

RO

Robbo on Tesla ·

The academically fascinating Tesla

Fair Value:US$301.1k% overvalued

12 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

AH

AHaron on Eli Lilly ·

Eli Lilly: A Pipeline-Driven Growth Story Trading 30% Below What the Business Is Actually Worth

Fair Value:US$1.48k37.7% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

Recently Updated Narratives

AL

alegget on Walt Disney ·

The happiest company on Earth, also perennially misunderstood.

Fair Value:US$134.6328.4% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

REElax on Volta Metals ·

Springer REE deposit valuation

Fair Value:CA$3.593.7% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AR

artoflosing on Tesla ·

Is Tesla a Stock or a Call Option? - A valuation nightmare!

Fair Value:US$30023.9% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

YA

Yang_ on SoFi Technologies ·

SoFi Technologies: The Apex Aggregator and the Infrastructure of the Modern Financial System

Fair Value:US$22.9830.9% undervalued

51 followersusers have followed this narrative

0 commentsusers have commented on this narrative

36 likesusers have liked this narrative

PD

pdixit1 on Vertiv Holdings Co ·

The Infrastructure AI Cannot Be Built Without

Fair Value:US$408.6438.7% undervalued

40 followersusers have followed this narrative

3 commentsusers have commented on this narrative

18 likesusers have liked this narrative

ZA

ZayaanS on Pro Medicus ·

Pro Medicus: The Market Is Confusing a Lumpy Quarter With a Broken Business

Fair Value:AU$196.7840.6% undervalued

34 followersusers have followed this narrative

7 commentsusers have commented on this narrative

21 likesusers have liked this narrative