Advertisement

Jonathan Murphy became the CEO of Assura Plc (LON:AGR) in 2016, and we think it's a good time to look at the executive's compensation against the backdrop of overall company performance. This analysis will also evaluate the appropriateness of CEO compensation when taking into account the earnings and shareholder returns of the company.

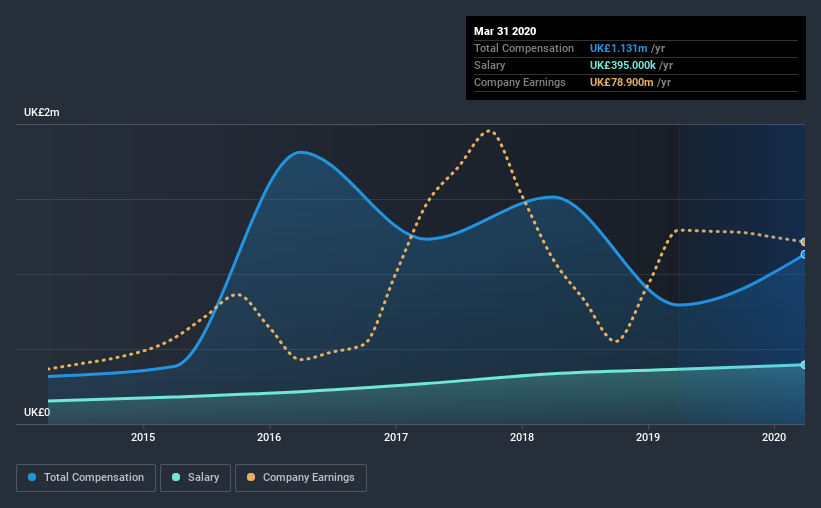

See our latest analysis for Assura

Comparing Assura Plc's CEO Compensation With the industry

At the time of writing, our data shows that Assura Plc has a market capitalization of UK£2.0b, and reported total annual CEO compensation of UK£1.1m for the year to March 2020. That's a notable increase of 42% on last year. While we always look at total compensation first, our analysis shows that the salary component is less, at UK£395k.

For comparison, other companies in the same industry with market capitalizations ranging between UK£1.6b and UK£5.1b had a median total CEO compensation of UK£1.5m. This suggests that Assura remunerates its CEO largely in line with the industry average. Furthermore, Jonathan Murphy directly owns UK£1.7m worth of shares in the company, implying that they are deeply invested in the company's success.

| Component | 2020 | 2019 | Proportion (2020) |

| Salary | UK£395k | UK£365k | 35% |

| Other | UK£736k | UK£429k | 65% |

| Total Compensation | UK£1.1m | UK£794k | 100% |

On an industry level, roughly 39% of total compensation represents salary and 61% is other remuneration. Assura sets aside a smaller share of compensation for salary, in comparison to the overall industry. If total compensation is slanted towards non-salary benefits, it indicates that CEO pay is linked to company performance.

A Look at Assura Plc's Growth Numbers

Assura Plc has reduced its earnings per share by 17% a year over the last three years. In the last year, its revenue is up 8.9%.

Overall this is not a very positive result for shareholders. The modest increase in revenue in the last year isn't enough to make us overlook the disappointing change in earnings per share. These factors suggest that the business performance wouldn't really justify a high pay packet for the CEO. Historical performance can sometimes be a good indicator on what's coming up next but if you want to peer into the company's future you might be interested in this free visualization of analyst forecasts.

Has Assura Plc Been A Good Investment?

Boasting a total shareholder return of 40% over three years, Assura Plc has done well by shareholders. This strong performance might mean some shareholders don't mind if the CEO were to be paid more than is normal for a company of its size.

In Summary...

As we touched on above, Assura Plc is currently paying a compensation that's close to the median pay for CEOs of companies belonging to the same industry and with similar market capitalizations. This doesn't look good when you see that earnings growth over the last three years has been negative. But on the bright side, shareholder returns have moved northward during the same period. We wouldn't say CEO compensation is too high, but shareholders might think performance needs to be improved before paying any more.

We can learn a lot about a company by studying its CEO compensation trends, along with looking at other aspects of the business. We identified 3 warning signs for Assura (1 is concerning!) that you should be aware of before investing here.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

When trading Assura or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account.Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About LSE:AGR

Assura

Assura plc is the UK's leading specialist healthcare property investor and developer.

Established dividend payer with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

Vita Life Sciences Set for a 12.72% Revenue Growth While Tackling Operational Challenges

Fair Value AU$2.42|8.7% undervalued

RO

Community Contributor

Vossloh rides a €500 billion wave to boost growth and earnings in the next decade

Fair Value €78.41|7.2% undervalued

CH

Community Contributor

Intuitive Surgical Will Transform Healthcare with 12% Revenue Growth

Fair Value US$325.55|56.5% overvalued

UN

Community Contributor