Advertisement

- United States

- /

- Machinery

- /

- NasdaqGS:ERII

How Does Energy Recovery's (NASDAQ:ERII) P/E Compare To Its Industry, After The Share Price Drop?

Unfortunately for some shareholders, the Energy Recovery (NASDAQ:ERII) share price has dived 31% in the last thirty days. Even longer term holders have taken a real hit with the stock declining 23% in the last year.

Assuming nothing else has changed, a lower share price makes a stock more attractive to potential buyers. In the long term, share prices tend to follow earnings per share, but in the short term prices bounce around in response to short term factors (which are not always obvious). The implication here is that long term investors have an opportunity when expectations of a company are too low. Perhaps the simplest way to get a read on investors' expectations of a business is to look at its Price to Earnings Ratio (PE Ratio). Investors have optimistic expectations of companies with higher P/E ratios, compared to companies with lower P/E ratios.

See our latest analysis for Energy Recovery

How Does Energy Recovery's P/E Ratio Compare To Its Peers?

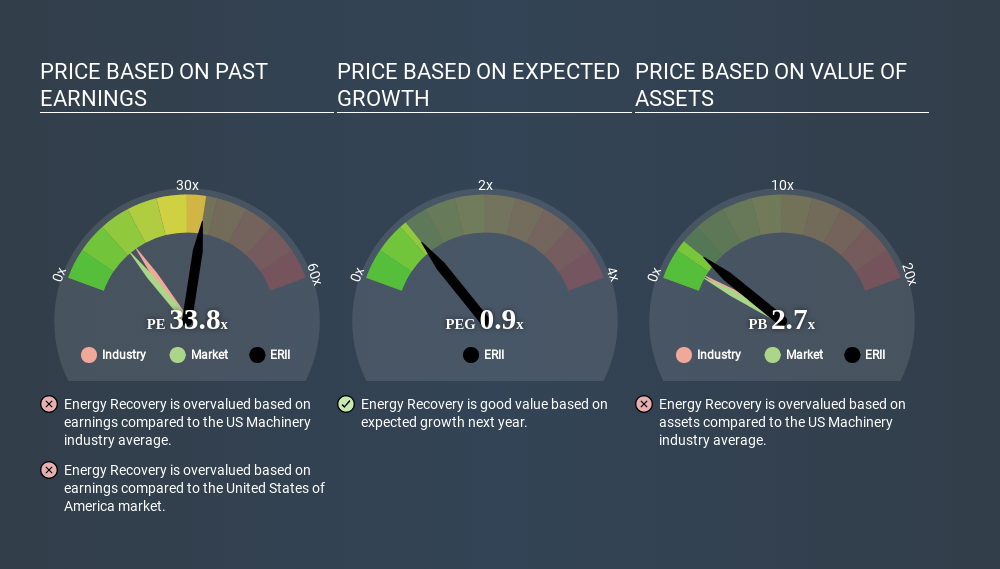

Energy Recovery's P/E of 33.76 indicates some degree of optimism towards the stock. The image below shows that Energy Recovery has a higher P/E than the average (15.0) P/E for companies in the machinery industry.

Its relatively high P/E ratio indicates that Energy Recovery shareholders think it will perform better than other companies in its industry classification. Shareholders are clearly optimistic, but the future is always uncertain. So investors should delve deeper. I like to check if company insiders have been buying or selling.

How Growth Rates Impact P/E Ratios

Probably the most important factor in determining what P/E a company trades on is the earnings growth. That's because companies that grow earnings per share quickly will rapidly increase the 'E' in the equation. Therefore, even if you pay a high multiple of earnings now, that multiple will become lower in the future. And as that P/E ratio drops, the company will look cheap, unless its share price increases.

Energy Recovery saw earnings per share decrease by 51% last year. But it has grown its earnings per share by 41% per year over the last three years.

Don't Forget: The P/E Does Not Account For Debt or Bank Deposits

One drawback of using a P/E ratio is that it considers market capitalization, but not the balance sheet. In other words, it does not consider any debt or cash that the company may have on the balance sheet. In theory, a company can lower its future P/E ratio by using cash or debt to invest in growth.

While growth expenditure doesn't always pay off, the point is that it is a good option to have; but one that the P/E ratio ignores.

How Does Energy Recovery's Debt Impact Its P/E Ratio?

Energy Recovery has net cash of US$85m. This is fairly high at 23% of its market capitalization. That might mean balance sheet strength is important to the business, but should also help push the P/E a bit higher than it would otherwise be.

The Bottom Line On Energy Recovery's P/E Ratio

Energy Recovery's P/E is 33.8 which is above average (13.0) in its market. The recent drop in earnings per share would make some investors cautious, but the healthy balance sheet means the company retains the potential for future growth. If this growth fails to materialise, the current high P/E could prove to be temporary, as the share price falls. Given Energy Recovery's P/E ratio has declined from 49.2 to 33.8 in the last month, we know for sure that the market is significantly less confident about the business today, than it was back then. For those who don't like to trade against momentum, that could be a warning sign, but a contrarian investor might want to take a closer look.

Investors should be looking to buy stocks that the market is wrong about. People often underestimate remarkable growth -- so investors can make money when fast growth is not fully appreciated. So this free visual report on analyst forecasts could hold the key to an excellent investment decision.

You might be able to find a better buy than Energy Recovery. If you want a selection of possible winners, check out this free list of interesting companies that trade on a P/E below 20 (but have proven they can grow earnings).

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About NasdaqGS:ERII

Energy Recovery

Designs, manufactures, and sells energy efficiency technology solutions in the United States, North, South and Latin America, the Middle East, Northern Africa, Asia, and Europe.

Flawless balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

WhiteCap Is Positioned To Profit Regardless Of Trump's Policy

Fair Value CA$22.60|60.9% undervalued

ST

Equity Analyst and Writer

Microsoft's Evolution Will Drive Revenue to New Heights Fueled by AI

Fair Value US$360.00|31.3% overvalued

BR

Community Contributor

A CASE FOR USD$2.50 (CAD$3.44) BY 2028 (A 5-10 BAGGER)

Fair Value CA$3.44|87.1% undervalued

AG

Community Contributor