Advertisement

- Hong Kong

- /

- Consumer Durables

- /

- SEHK:3882

Here's Why Sky Light Holdings (HKG:3882) Can Manage Its Debt Responsibly

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about. So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We note that Sky Light Holdings Limited (HKG:3882) does have debt on its balance sheet. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we examine debt levels, we first consider both cash and debt levels, together.

View our latest analysis for Sky Light Holdings

How Much Debt Does Sky Light Holdings Carry?

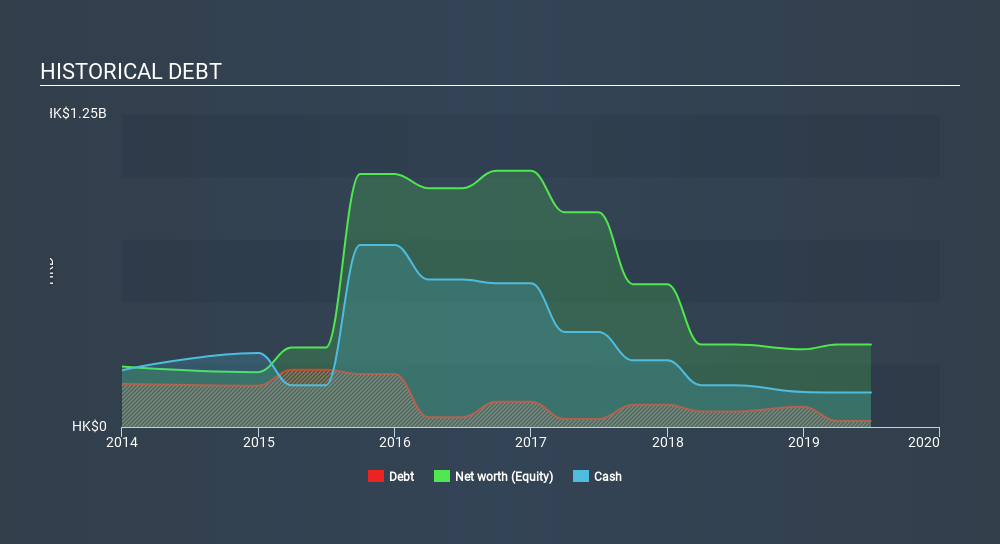

You can click the graphic below for the historical numbers, but it shows that as of June 2019 Sky Light Holdings had HK$24.3m of debt, an increase on HK$62.0, over one year. But it also has HK$138.2m in cash to offset that, meaning it has HK$113.9m net cash.

How Strong Is Sky Light Holdings's Balance Sheet?

We can see from the most recent balance sheet that Sky Light Holdings had liabilities of HK$184.2m falling due within a year, and liabilities of HK$44.0m due beyond that. Offsetting these obligations, it had cash of HK$138.2m as well as receivables valued at HK$55.1m due within 12 months. So its liabilities total HK$34.9m more than the combination of its cash and short-term receivables.

Of course, Sky Light Holdings has a market capitalization of HK$285.8m, so these liabilities are probably manageable. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time. Despite its noteworthy liabilities, Sky Light Holdings boasts net cash, so it's fair to say it does not have a heavy debt load!

It was also good to see that despite losing money on the EBIT line last year, Sky Light Holdings turned things around in the last 12 months, delivering and EBIT of HK$121m. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Sky Light Holdings can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. While Sky Light Holdings has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. Over the last year, Sky Light Holdings reported free cash flow worth 7.7% of its EBIT, which is really quite low. For us, cash conversion that low sparks a little paranoia about is ability to extinguish debt.

Summing up

Although Sky Light Holdings's balance sheet isn't particularly strong, due to the total liabilities, it is clearly positive to see that it has net cash of HK$113.9m. So we don't have any problem with Sky Light Holdings's use of debt. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. Case in point: We've spotted 4 warning signs for Sky Light Holdings you should be aware of, and 2 of them are concerning.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About SEHK:3882

Sky Light Holdings

An investment holding company, manufactures and distributes home surveillance cameras, digital imaging products, and other related products in the United States, Mainland China, the European Union, Hong Kong, and internationally.

Excellent balance sheet with weak fundamentals.

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|32.0% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|21.7% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|0.5% overvalued

DA

Community Contributor