Advertisement

- United States

- /

- Aerospace & Defense

- /

- NYSE:HII

Here's How P/E Ratios Can Help Us Understand Huntington Ingalls Industries, Inc. (NYSE:HII)

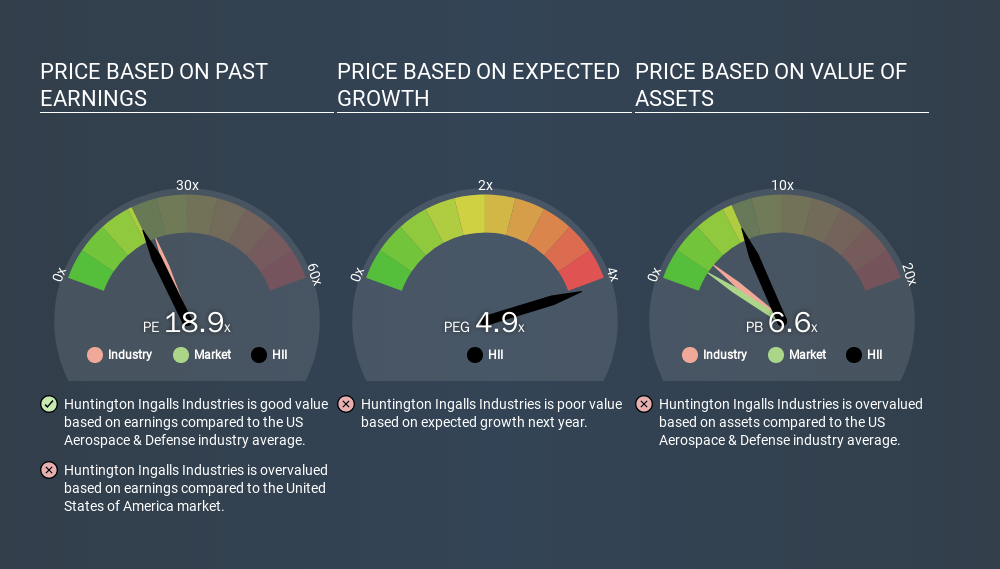

This article is written for those who want to get better at using price to earnings ratios (P/E ratios). To keep it practical, we'll show how Huntington Ingalls Industries, Inc.'s (NYSE:HII) P/E ratio could help you assess the value on offer. What is Huntington Ingalls Industries's P/E ratio? Well, based on the last twelve months it is 18.87. That is equivalent to an earnings yield of about 5.3%.

Check out our latest analysis for Huntington Ingalls Industries

How Do I Calculate Huntington Ingalls Industries's Price To Earnings Ratio?

The formula for price to earnings is:

Price to Earnings Ratio = Price per Share ÷ Earnings per Share (EPS)

Or for Huntington Ingalls Industries:

P/E of 18.87 = USD276.47 ÷ USD14.65 (Based on the year to September 2019.)

Is A High Price-to-Earnings Ratio Good?

A higher P/E ratio means that buyers have to pay a higher price for each USD1 the company has earned over the last year. That is not a good or a bad thing per se, but a high P/E does imply buyers are optimistic about the future.

How Does Huntington Ingalls Industries's P/E Ratio Compare To Its Peers?

The P/E ratio essentially measures market expectations of a company. If you look at the image below, you can see Huntington Ingalls Industries has a lower P/E than the average (21.0) in the aerospace & defense industry classification.

Its relatively low P/E ratio indicates that Huntington Ingalls Industries shareholders think it will struggle to do as well as other companies in its industry classification. Since the market seems unimpressed with Huntington Ingalls Industries, it's quite possible it could surprise on the upside. It is arguably worth checking if insiders are buying shares, because that might imply they believe the stock is undervalued.

How Growth Rates Impact P/E Ratios

P/E ratios primarily reflect market expectations around earnings growth rates. That's because companies that grow earnings per share quickly will rapidly increase the 'E' in the equation. That means even if the current P/E is high, it will reduce over time if the share price stays flat. Then, a lower P/E should attract more buyers, pushing the share price up.

Huntington Ingalls Industries's earnings per share fell by 5.4% in the last twelve months. But over the longer term (5 years) earnings per share have increased by 14%.

Remember: P/E Ratios Don't Consider The Balance Sheet

The 'Price' in P/E reflects the market capitalization of the company. So it won't reflect the advantage of cash, or disadvantage of debt. Hypothetically, a company could reduce its future P/E ratio by spending its cash (or taking on debt) to achieve higher earnings.

While growth expenditure doesn't always pay off, the point is that it is a good option to have; but one that the P/E ratio ignores.

Is Debt Impacting Huntington Ingalls Industries's P/E?

Huntington Ingalls Industries's net debt is 13% of its market cap. This could bring some additional risk, and reduce the number of investment options for management; worth remembering if you compare its P/E to businesses without debt.

The Bottom Line On Huntington Ingalls Industries's P/E Ratio

Huntington Ingalls Industries trades on a P/E ratio of 18.9, which is fairly close to the US market average of 18.6. With modest debt, and a lack of recent growth, it would seem the market is expecting improvement in earnings.

Investors have an opportunity when market expectations about a stock are wrong. People often underestimate remarkable growth -- so investors can make money when fast growth is not fully appreciated. So this free visualization of the analyst consensus on future earnings could help you make the right decision about whether to buy, sell, or hold.

You might be able to find a better buy than Huntington Ingalls Industries. If you want a selection of possible winners, check out this free list of interesting companies that trade on a P/E below 20 (but have proven they can grow earnings).

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About NYSE:HII

Huntington Ingalls Industries

Designs, builds, overhauls, and repairs military ships in the United States.

Good value average dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

WhiteCap Is Positioned To Profit Regardless Of Trump's Policy

Fair Value CA$22.60|61.5% undervalued

ST

Equity Analyst and Writer

Microsoft's Evolution Will Drive Revenue to New Heights Fueled by AI

Fair Value US$360.00|30.7% overvalued

BR

Community Contributor

A CASE FOR USD$2.50 (CAD$3.44) BY 2028 (A 5-10 BAGGER)

Fair Value CA$3.44|88.1% undervalued

AG

Community Contributor