Advertisement

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, EchoStar Corporation (NASDAQ:SATS) does carry debt. But should shareholders be worried about its use of debt?

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we examine debt levels, we first consider both cash and debt levels, together.

See our latest analysis for EchoStar

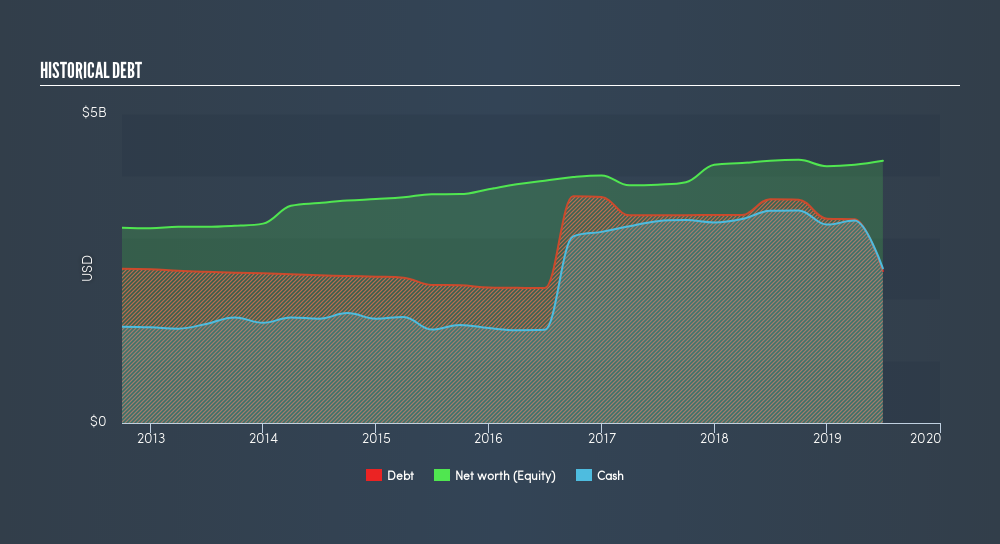

What Is EchoStar's Debt?

You can click the graphic below for the historical numbers, but it shows that EchoStar had US$2.46b of debt in June 2019, down from US$3.62b, one year before. However, its balance sheet shows it holds US$2.50b in cash, so it actually has US$42.9m net cash.

How Healthy Is EchoStar's Balance Sheet?

According to the last reported balance sheet, EchoStar had liabilities of US$471.7m due within 12 months, and liabilities of US$3.24b due beyond 12 months. Offsetting these obligations, it had cash of US$2.50b as well as receivables valued at US$215.5m due within 12 months. So it has liabilities totalling US$990.3m more than its cash and near-term receivables, combined.

EchoStar has a market capitalization of US$3.80b, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. But it's clear that we should definitely closely examine whether it can manage its debt without dilution. Despite its noteworthy liabilities, EchoStar boasts net cash, so it's fair to say it does not have a heavy debt load!

Unfortunately, EchoStar's EBIT flopped 19% over the last four quarters. If that sort of decline is not arrested, then the managing its debt will be harder than selling broccoli flavoured ice-cream for a premium. There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if EchoStar can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. EchoStar may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. Over the most recent three years, EchoStar recorded free cash flow worth 71% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Summing up

Although EchoStar's balance sheet isn't particularly strong, due to the total liabilities, it is clearly positive to see that it has net cash of US$43m. And it impressed us with free cash flow of US$203m, being 71% of its EBIT. So while EchoStar does not have a great balance sheet, it's certainly not too bad. Even though EchoStar lost money on the bottom line, its positive EBIT suggests the business itself has potential. So you might want to check outhow earnings have been trending over the last few years.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About NasdaqGS:SATS

EchoStar

Provides networking technologies and services in the United States and internationally.

Fair value low.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|31.2% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|24.4% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|13.5% overvalued

DA

Community Contributor