Advertisement

- United States

- /

- REITS

- /

- NasdaqGS:GOOD

Earnings Update: Here's Why Analysts Just Lifted Their Gladstone Commercial Corporation Price Target To US$25.00

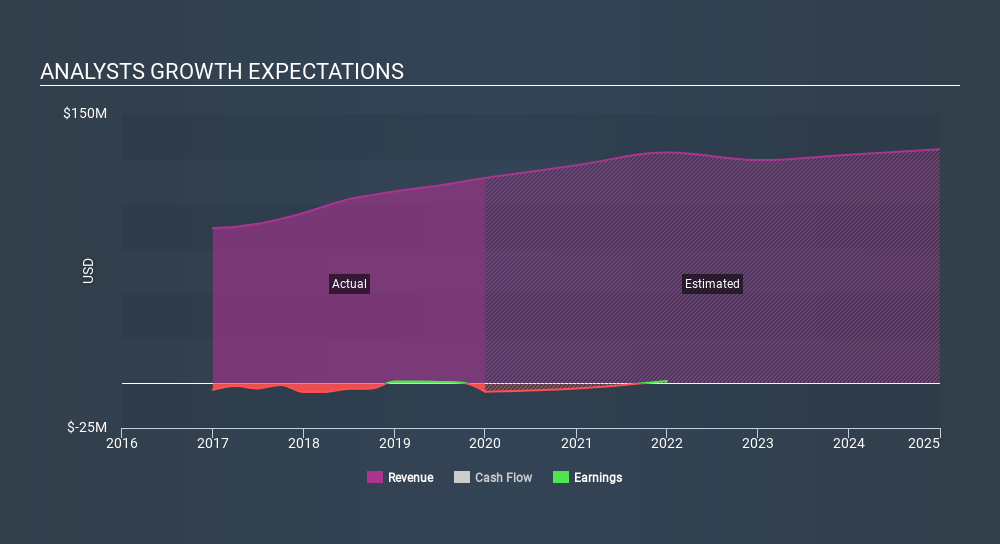

Gladstone Commercial Corporation (NASDAQ:GOOD) last week reported its latest annual results, which makes it a good time for investors to dive in and see if the business is performing in line with expectations. Revenues of US$114m arrived in line with expectations, although statutory losses per share were US$0.16, an impressive 1500% smaller than what broker models predicted. Earnings are an important time for investors, as they can track a company's performance, look at what top analysts are forecasting for next year, and see if there's been a change in sentiment towards the company. We thought readers would find it interesting to see analysts' latest (statutory) post-earnings forecasts for next year.

View our latest analysis for Gladstone Commercial

Taking into account the latest results, the most recent consensus for Gladstone Commercial from three analysts is for revenues of US$121.4m in 2020, which is a satisfactory 6.1% increase on its sales over the past 12 months. Per-share statutory losses are expected to explode, reaching US$0.09 per share. Before this earnings announcement, analysts had been forecasting revenues of US$122.6m and losses of US$0.073 per share in 2020. Analysts seem to have become more bearish following the latest results. While there were no changes to revenue forecasts, there was a large cut to EPS estimates.

Despite expectations of heavier losses next year, analysts have lifted their price target 13% to US$25.00, perhaps implying these losses are not expected to be recurring over the long term. That's not the only conclusion we can draw from this data however, as some investors also like to consider the spread in estimates when evaluating analyst price targets. There are some variant perceptions on Gladstone Commercial, with the most bullish analyst valuing it at US$26.00 and the most bearish at US$24.00 per share. Still, with such a tight range of estimates, it suggests analysts have a pretty good idea of what they think the company is worth.

It can also be useful to step back and take a broader view of how analyst forecasts compare to Gladstone Commercial's performance in recent years. We would highlight that Gladstone Commercial's revenue growth is expected to slow, with forecast 6.1% increase next year well below the historical 8.5%p.a. growth over the last five years. Juxtapose this against the other companies in the market with analyst coverage, which are forecast to grow their revenues (in aggregate) 5.0% next year. Factoring in the forecast slowdown in growth, it looks like analysts are expecting Gladstone Commercial to grow at about the same rate as the wider market.

The Bottom Line

The most important thing to take away is that analysts reconfirmed their loss per share estimates for next year. They also reconfirmed their revenue estimates, with the company predicted to grow at about the same rate as the wider market. There was also a nice increase in the price target, with analysts feeling that the intrinsic value of the business is improving.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. We have estimates - from multiple Gladstone Commercial analysts - going out to 2024, and you can see them free on our platform here.

You can also see whether Gladstone Commercial is carrying too much debt, and whether its balance sheet is healthy, for free on our platform here.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About NasdaqGS:GOOD

Gladstone Commercial

A real estate investment trust focused on acquiring, owning, and operating net leased industrial and office properties across the United States.

Second-rate dividend payer low.

Market Insights

Advertisement

Community Narratives

Vita Life Sciences Set for a 12.72% Revenue Growth While Tackling Operational Challenges

Fair Value AU$2.42|12.0% undervalued

RO

Community Contributor

Vossloh rides a €500 billion wave to boost growth and earnings in the next decade

Fair Value €78.41|5.2% undervalued

CH

Community Contributor

Intuitive Surgical Will Transform Healthcare with 12% Revenue Growth

Fair Value US$325.55|57.3% overvalued

UN

Community Contributor