Advertisement

Does Tongda Group Holdings Limited's (HKG:698) CEO Pay Matter?

Ya Nan Wang is the CEO of Tongda Group Holdings Limited (HKG:698). This report will, first, examine the CEO compensation levels in comparison to CEO compensation at companies of similar size. Next, we'll consider growth that the business demonstrates. Third, we'll reflect on the total return to shareholders over three years, as a second measure of business performance. The aim of all this is to consider the appropriateness of CEO pay levels.

View our latest analysis for Tongda Group Holdings

How Does Ya Nan Wang's Compensation Compare With Similar Sized Companies?

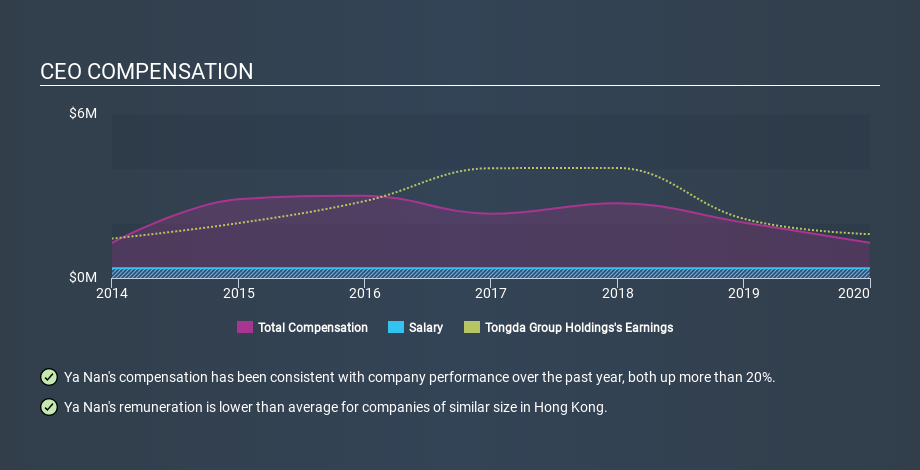

At the time of writing, our data says that Tongda Group Holdings Limited has a market cap of HK$2.8b, and reported total annual CEO compensation of HK$1.3m for the year to December 2019. That's below the compensation, last year. We think total compensation is more important but we note that the CEO salary is lower, at HK$360k. We further remind readers that the CEO may face performance requirements to receive the non-salary part of the total compensation. When we examined a selection of companies with market caps ranging from HK$1.6b to HK$6.2b, we found the median CEO total compensation was HK$3.2m.

Next, let's break down remuneration compositions to understand how the industry and company compare with each other. On a sector level, around 78% of total compensation represents salary and 22% is other remuneration. Readers will want to know that Tongda Group Holdings pays a modest slice of remuneration through salary, as compared to the wider sector.

Most shareholders would consider it a positive that Ya Nan Wang takes less total compensation than the CEOs of most similar size companies, leaving more for shareholders. Though positive, it's important we delve into the performance of the actual business. The graphic below shows how CEO compensation at Tongda Group Holdings has changed from year to year.

Is Tongda Group Holdings Limited Growing?

Over the last three years Tongda Group Holdings Limited has shrunk its earnings per share by an average of 34% per year (measured with a line of best fit). It achieved revenue growth of 3.2% over the last year.

Unfortunately, earnings per share have trended lower over the last three years. The modest increase in revenue in the last year isn't enough to make me overlook the disappointing change in earnings per share. These factors suggest that the business performance wouldn't really justify a high pay packet for the CEO. Shareholders might be interested in this free visualization of analyst forecasts.

Has Tongda Group Holdings Limited Been A Good Investment?

With a three year total loss of 78%, Tongda Group Holdings Limited would certainly have some dissatisfied shareholders. So shareholders would probably think the company shouldn't be too generous with CEO compensation.

In Summary...

It appears that Tongda Group Holdings Limited remunerates its CEO below most similar sized companies.

Ya Nan Wang is paid less than CEOs of similar size companies, but the company isn't growing and total shareholder returns have been disappointing. Considering all these factors, we'd stop short of saying the CEO pay is too high, but we don't think shareholders would want to see a pay rise before business performance improves. Shifting gears from CEO pay for a second, we've picked out 2 warning signs for Tongda Group Holdings that investors should be aware of in a dynamic business environment.

If you want to buy a stock that is better than Tongda Group Holdings, this free list of high return, low debt companies is a great place to look.

Love or hate this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned. Thank you for reading.

About SEHK:698

Tongda Group Holdings

An investment holding company, provides high-precision structural components for smart mobile communications and consumer electronic products.

Reasonable growth potential with adequate balance sheet.

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Unicycive Therapeutics ·

Looking to be second time lucky with a game-changing new product

Fair Value:US$21.5360.2% undervalued

137 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative

DE

Degen_GCR on Everpure ·

Second order memory play likely to double in a year

Fair Value:US$18053.4% undervalued

21 followersusers have followed this narrative

1 commentusers have commented on this narrative

15 likesusers have liked this narrative

DO

Double_Bubbler on Intuitive Machines ·

Intuitive Machines: To The Moon and Beyond!

Fair Value:US$42.313.7% undervalued

12 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

YI

yiannisz on AppLovin ·

AppLovin’s AI Engine Is Printing Profit

Fair Value:US$989.2451.0% undervalued

32 followersusers have followed this narrative

2 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

MR

MRT23 on CorMedix ·

CRMD is trading at 5.9x trough-year EBITDA with the market ascribing near-zero value to two near-term pipeline events

Fair Value:US$1233.9% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

KA

kapirey on Everpure ·

Everpure's AI Infrastructure Transition Will Boost Future Valuation

Fair Value:US$74.7812.1% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

KA

kapirey on IREN ·

IREN to Transform into AI Cloud Giant with Mirantis Acquisition

Fair Value:US$44.331.8% overvalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8589.9% undervalued

108 followersusers have followed this narrative

2 commentsusers have commented on this narrative

31 likesusers have liked this narrative

TR

tripledub on Meta Platforms ·

The $135 Billion Bet That Should Make Every Shareholder Nervous

Fair Value:US$74016.4% undervalued

37 followersusers have followed this narrative

3 commentsusers have commented on this narrative

33 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$268.6112.2% undervalued

1182 followersusers have followed this narrative

7 commentsusers have commented on this narrative

34 likesusers have liked this narrative