Advertisement

- United Kingdom

- /

- IT

- /

- AIM:SYS

Does SysGroup (LON:SYS) Have A Healthy Balance Sheet?

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital. When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. As with many other companies SysGroup plc (LON:SYS) makes use of debt. But the more important question is: how much risk is that debt creating?

When Is Debt Dangerous?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

Check out our latest analysis for SysGroup

How Much Debt Does SysGroup Carry?

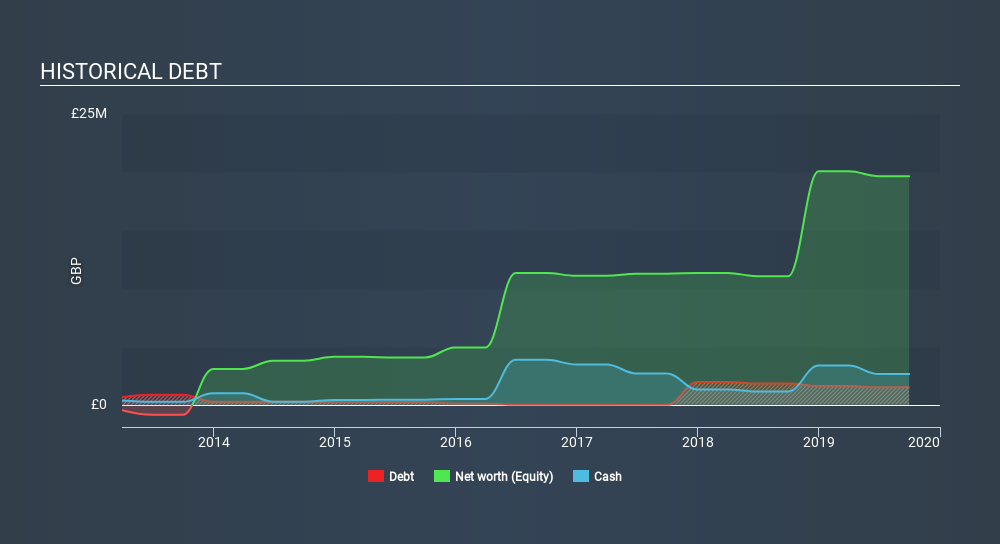

As you can see below, SysGroup had UK£1.51m of debt at September 2019, down from UK£1.83m a year prior. However, its balance sheet shows it holds UK£2.65m in cash, so it actually has UK£1.14m net cash.

A Look At SysGroup's Liabilities

We can see from the most recent balance sheet that SysGroup had liabilities of UK£6.42m falling due within a year, and liabilities of UK£3.11m due beyond that. Offsetting these obligations, it had cash of UK£2.65m as well as receivables valued at UK£1.17m due within 12 months. So it has liabilities totalling UK£5.72m more than its cash and near-term receivables, combined.

While this might seem like a lot, it is not so bad since SysGroup has a market capitalization of UK£14.8m, and so it could probably strengthen its balance sheet by raising capital if it needed to. But it's clear that we should definitely closely examine whether it can manage its debt without dilution. Despite its noteworthy liabilities, SysGroup boasts net cash, so it's fair to say it does not have a heavy debt load!

Shareholders should be aware that SysGroup's EBIT was down 43% last year. If that decline continues then paying off debt will be harder than selling foie gras at a vegan convention. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine SysGroup's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. While SysGroup has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. Over the last two years, SysGroup actually produced more free cash flow than EBIT. There's nothing better than incoming cash when it comes to staying in your lenders' good graces.

Summing up

Although SysGroup's balance sheet isn't particularly strong, due to the total liabilities, it is clearly positive to see that it has net cash of UK£1.14m. The cherry on top was that in converted 245% of that EBIT to free cash flow, bringing in UK£902k. So although we see some areas for improvement, we're not too worried about SysGroup's balance sheet. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. To that end, you should learn about the 3 warning signs we've spotted with SysGroup (including 1 which is is concerning) .

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About AIM:SYS

SysGroup

Provides managed information technology services specializing in the delivery of cloud, data, and security services to power AI and ML transformation in the United Kingdom and internationally.

Excellent balance sheet with slight risk.

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Giftify ·

Giftify ($GIFT): A Small-Cap Incentives Platform with More ScaleThan Its Valuation Suggests

Fair Value:US$2.564.5% undervalued

62 followersusers have followed this narrative

2 commentsusers have commented on this narrative

12 likesusers have liked this narrative

BE

benjamin_lvieq on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6526.7% undervalued

16 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

JD

JD009 on Celsius Holdings ·

From $5M to $2B: Why the 2024 Crash Was the Best Buying Opportunity in Consumer Stocks

Fair Value:US$55.4346.2% undervalued

5 followersusers have followed this narrative

1 commentusers have commented on this narrative

6 likesusers have liked this narrative

WA

Wavefarer on Accenture ·

High-quality global services company facing an AI-driven valuation reset.

Fair Value:US$30154.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

RO

RockeTeller on Silver Mines ·

Australia’s Largest Undeveloped Silver Project Just Got a Low-Cost Makeover

Fair Value:AU$4.1996.8% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VA

Valtersa on Saudi National Bank ·

Projected Fair Value of Saudi National Bank Reaches 52

Fair Value:ر.س5227.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

ON

Ontological on AmanahRaya Real Estate Investment Trust ·

Income Focused ARREIT

Fair Value:RM 0.21104.8% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75028.3% undervalued

89 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5450.8% undervalued

62 followersusers have followed this narrative

3 commentsusers have commented on this narrative

11 likesusers have liked this narrative

CE

Ceazar on Conexeu Sciences ·

This small biotech is developing technology that could potentially change how tissue is rebuilt

Fair Value:US$25.3459.2% undervalued

60 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative