Advertisement

- Hong Kong

- /

- Semiconductors

- /

- SEHK:1665

Does Pentamaster International (HKG:1665) Have A Healthy Balance Sheet?

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital. So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. As with many other companies Pentamaster International Limited (HKG:1665) makes use of debt. But is this debt a concern to shareholders?

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

View our latest analysis for Pentamaster International

How Much Debt Does Pentamaster International Carry?

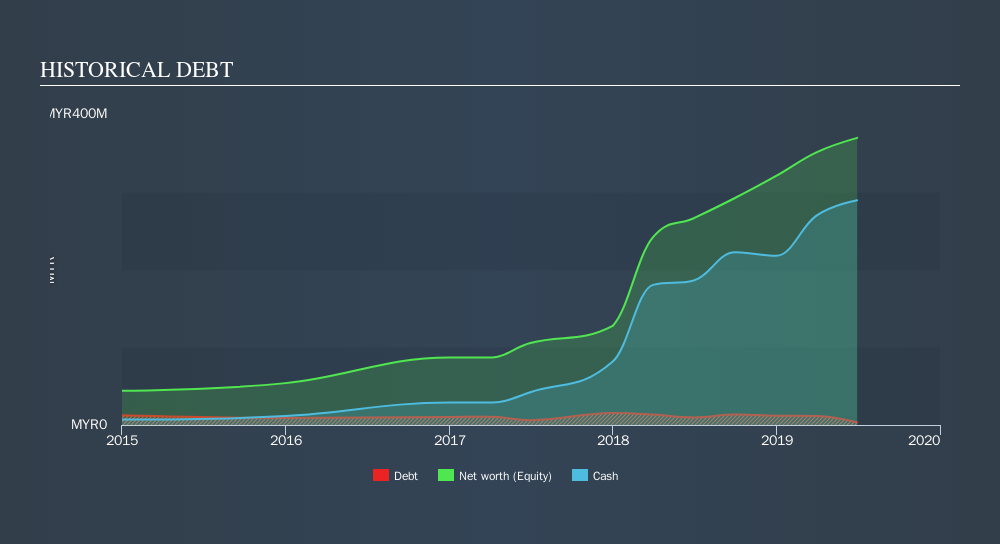

You can click the graphic below for the historical numbers, but it shows that Pentamaster International had RM3.50m of debt in June 2019, down from RM9.89m, one year before. But it also has RM289.1m in cash to offset that, meaning it has RM285.6m net cash.

A Look At Pentamaster International's Liabilities

We can see from the most recent balance sheet that Pentamaster International had liabilities of RM171.1m falling due within a year, and liabilities of RM131.0k due beyond that. Offsetting this, it had RM289.1m in cash and RM56.4m in receivables that were due within 12 months. So it actually has RM174.2m more liquid assets than total liabilities.

This surplus suggests that Pentamaster International has a conservative balance sheet, and could probably eliminate its debt without much difficulty. Succinctly put, Pentamaster International boasts net cash, so it's fair to say it does not have a heavy debt load!

In addition to that, we're happy to report that Pentamaster International has boosted its EBIT by 79%, thus reducing the spectre of future debt repayments. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Pentamaster International's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. Pentamaster International may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. During the last three years, Pentamaster International generated free cash flow amounting to a very robust 81% of its EBIT, more than we'd expect. That puts it in a very strong position to pay down debt.

Summing up

While we empathize with investors who find debt concerning, you should keep in mind that Pentamaster International has net cash of RM285.6m, as well as more liquid assets than liabilities. And it impressed us with free cash flow of RM106m, being 81% of its EBIT. So we don't think Pentamaster International's use of debt is risky. Another factor that would give us confidence in Pentamaster International would be if insiders have been buying shares: if you're conscious of that signal too, you can find out instantly by clicking this link.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About SEHK:1665

Pentamaster International

An investment holding company, provides automation manufacturing and technology solutions in Malaysia and internationally.

Flawless balance sheet with reasonable growth potential.

Market Insights

Advertisement

Community Narratives

A case for TSXV:USA to reach USD $5.00 - $9.00 (CAD $7.30–$12.29) by 2029.

Fair Value CA$12.29|91.2% undervalued

AG

Community Contributor

DLocal's Future Growth Fueled by 35% Revenue and Profit Margin Boosts

Fair Value US$195.39|94.1% undervalued

WY

Community Contributor

Historically Cheap, but the Margin of Safety Is Still Thin

Fair Value SEK 232.58|13.2% undervalued

MA

Community Contributor