Advertisement

- United States

- /

- Aerospace & Defense

- /

- NYSE:MOG.A

Does Moog Inc. (NYSE:MOG.A) Create Value For Shareholders?

While some investors are already well versed in financial metrics (hat tip), this article is for those who would like to learn about Return On Equity (ROE) and why it is important. We'll use ROE to examine Moog Inc. (NYSE:MOG.A), by way of a worked example.

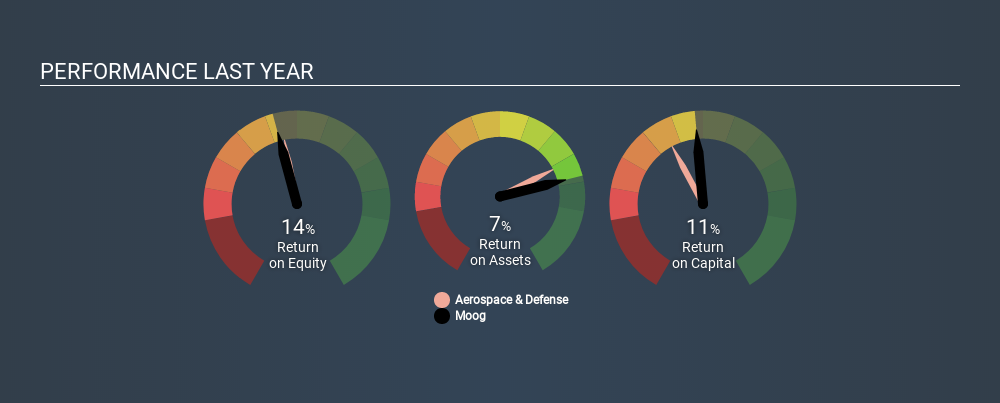

Our data shows Moog has a return on equity of 14% for the last year. Another way to think of that is that for every $1 worth of equity in the company, it was able to earn $0.14.

Check out our latest analysis for Moog

How Do You Calculate ROE?

The formula for return on equity is:

Return on Equity = Net Profit ÷ Shareholders' Equity

Or for Moog:

14% = US$180m ÷ US$1.3b (Based on the trailing twelve months to September 2019.)

It's easy to understand the 'net profit' part of that equation, but 'shareholders' equity' requires further explanation. It is all earnings retained by the company, plus any capital paid in by shareholders. Shareholders' equity can be calculated by subtracting the total liabilities of the company from the total assets of the company.

What Does Return On Equity Signify?

ROE measures a company's profitability against the profit it retains, and any outside investments. The 'return' is the yearly profit. The higher the ROE, the more profit the company is making. So, all else equal, investors should like a high ROE. That means it can be interesting to compare the ROE of different companies.

Does Moog Have A Good ROE?

One simple way to determine if a company has a good return on equity is to compare it to the average for its industry. The limitation of this approach is that some companies are quite different from others, even within the same industry classification. You can see in the graphic below that Moog has an ROE that is fairly close to the average for the Aerospace & Defense industry (14%).

That's not overly surprising. ROE can give us a view about company quality, but many investors also look to other factors, such as whether there are insiders buying shares. I will like Moog better if I see some big insider buys. While we wait, check out this free list of growing companies with considerable, recent, insider buying.

How Does Debt Impact Return On Equity?

Most companies need money -- from somewhere -- to grow their profits. The cash for investment can come from prior year profits (retained earnings), issuing new shares, or borrowing. In the case of the first and second options, the ROE will reflect this use of cash, for growth. In the latter case, the use of debt will improve the returns, but will not change the equity. Thus the use of debt can improve ROE, albeit along with extra risk in the case of stormy weather, metaphorically speaking.

Moog's Debt And Its 14% ROE

Moog has a debt to equity ratio of 0.63, which is far from excessive. Its very respectable ROE, combined with only modest debt, suggests the business is in good shape. Judicious use of debt to improve returns can certainly be a good thing, although it does elevate risk slightly and reduce future optionality.

The Bottom Line On ROE

Return on equity is one way we can compare the business quality of different companies. In my book the highest quality companies have high return on equity, despite low debt. All else being equal, a higher ROE is better.

But when a business is high quality, the market often bids it up to a price that reflects this. Profit growth rates, versus the expectations reflected in the price of the stock, are a particularly important to consider. So I think it may be worth checking this free report on analyst forecasts for the company.

But note: Moog may not be the best stock to buy. So take a peek at this free list of interesting companies with high ROE and low debt.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About NYSE:MOG.A

Moog

Designs, manufactures, and integrates precision motion and fluid controls and controls systems for original equipment manufacturers and end users in the aerospace, defense, and industrial markets in the United States, Germany, and internationally.

Excellent balance sheet with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Gain Therapeutics ·

The Market Is Sleeping on This Parkinson's Biotech - And I Think That's a Mistake

Fair Value:US$7.672.0% undervalued

31 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative

KI

Kingman1152 on NVIDIA ·

NVIDIA will see a profit margin surge of 55% in the next 5 years

Fair Value:US$305.233.9% undervalued

58 followersusers have followed this narrative

1 commentusers have commented on this narrative

19 likesusers have liked this narrative

TE

TechMegaTrends on Bambuser ·

Bambuser is today the only listed company in Europe that simultaneously possesses an 85% gross margin, proprietary AI infrastructure for the

Fair Value:SEK 238.2686.6% undervalued

34 followersusers have followed this narrative

0 commentsusers have commented on this narrative

15 likesusers have liked this narrative

HE

HedgeY on Constellium ·

Constellium jet another cyclical aluminum processor, or a mispriced aluminum platform?

Fair Value:US$3413.0% undervalued

9 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

Recently Updated Narratives

MA

Martimmfonseca on Extreme Networks ·

Extreme Networks Could Reach $52 Over the Next Five Years

Fair Value:US$5265.4% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

Martimmfonseca on Himax Technologies ·

Himax Technologies Could Reach $17 Over the Next Five Years

Fair Value:US$1734.7% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

Martimmfonseca on ACM Research ·

ACM Research Could Reach $61–$91 Over the Next Five Years

Fair Value:US$6117.0% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TR

tripledub on Microsoft ·

Everyone's Terrified Microsoft Will Keep Spending. I'm Terrified They'll Stop.

Fair Value:US$3957.0% overvalued

52 followersusers have followed this narrative

3 commentsusers have commented on this narrative

43 likesusers have liked this narrative

KI

Kingman1152 on NVIDIA ·

NVIDIA will see a profit margin surge of 55% in the next 5 years

Fair Value:US$305.233.9% undervalued

58 followersusers have followed this narrative

1 commentusers have commented on this narrative

19 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$579.5727.1% undervalued

1368 followersusers have followed this narrative

2 commentsusers have commented on this narrative

11 likesusers have liked this narrative