Advertisement

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about. So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. Importantly, DWF Group plc (LON:DWF) does carry debt. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first step when considering a company's debt levels is to consider its cash and debt together.

Check out our latest analysis for DWF Group

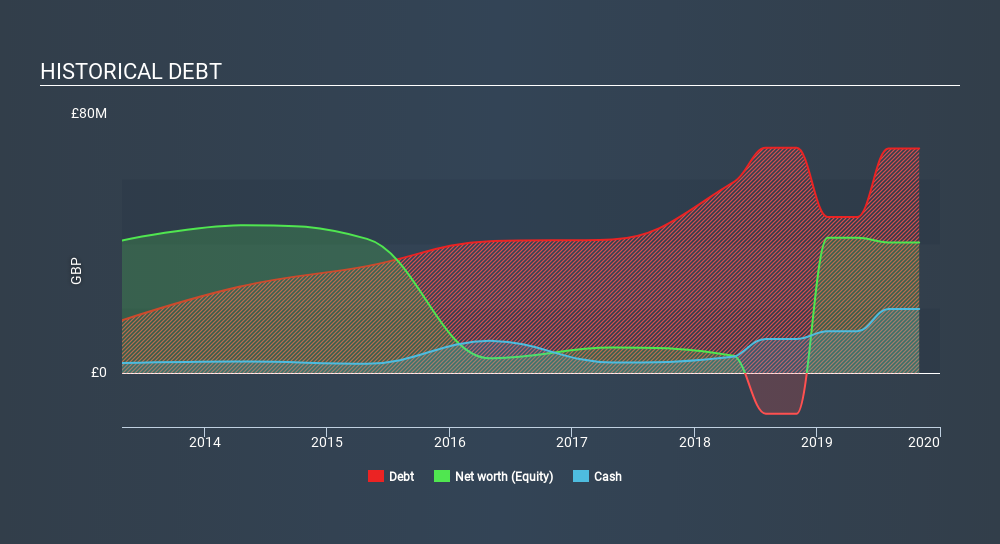

How Much Debt Does DWF Group Carry?

The chart below, which you can click on for greater detail, shows that DWF Group had UK£69.4m in debt in October 2019; about the same as the year before. However, it also had UK£19.8m in cash, and so its net debt is UK£49.5m.

How Strong Is DWF Group's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that DWF Group had liabilities of UK£96.9m due within 12 months and liabilities of UK£140.2m due beyond that. Offsetting these obligations, it had cash of UK£19.8m as well as receivables valued at UK£161.5m due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by UK£55.8m.

Given DWF Group has a market capitalization of UK£305.5m, it's hard to believe these liabilities pose much threat. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

DWF Group's net debt of 2.0 times EBITDA suggests graceful use of debt. And the fact that its trailing twelve months of EBIT was 8.6 times its interest expenses harmonizes with that theme. If DWF Group can keep growing EBIT at last year's rate of 15% over the last year, then it will find its debt load easier to manage. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine DWF Group's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So it's worth checking how much of that EBIT is backed by free cash flow. During the last three years, DWF Group burned a lot of cash. While investors are no doubt expecting a reversal of that situation in due course, it clearly does mean its use of debt is more risky.

Our View

DWF Group's conversion of EBIT to free cash flow was a real negative on this analysis, although the other factors we considered were considerably better. In particular, we thought its interest cover was a positive. Looking at all this data makes us feel a little cautious about DWF Group's debt levels. While we appreciate debt can enhance returns on equity, we'd suggest that shareholders keep close watch on its debt levels, lest they increase. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. Take risks, for example - DWF Group has 3 warning signs (and 1 which is a bit concerning) we think you should know about.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About LSE:DWF

DWF Group

DWF Group plc provides integrated legal and business services in Europe, the Middle East, Asia, Australia, and North America.

Adequate balance sheet and fair value.

Market Insights

Advertisement

Community Narratives

Vita Life Sciences Set for a 12.72% Revenue Growth While Tackling Operational Challenges

Fair Value AU$2.42|8.7% undervalued

RO

Community Contributor

Vossloh rides a €500 billion wave to boost growth and earnings in the next decade

Fair Value €78.41|7.2% undervalued

CH

Community Contributor

Intuitive Surgical Will Transform Healthcare with 12% Revenue Growth

Fair Value US$325.55|56.5% overvalued

UN

Community Contributor