Advertisement

- United States

- /

- Electronic Equipment and Components

- /

- NasdaqGS:CDW

Does CDW (NASDAQ:CDW) Have A Healthy Balance Sheet?

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. Importantly, CDW Corporation (NASDAQ:CDW) does carry debt. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

See our latest analysis for CDW

What Is CDW's Debt?

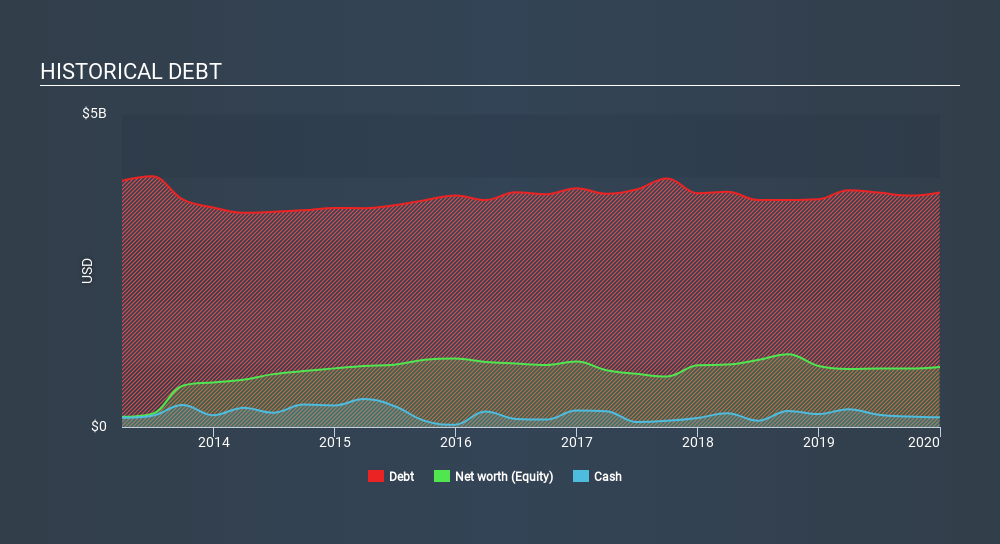

The chart below, which you can click on for greater detail, shows that CDW had US$3.75b in debt in December 2019; about the same as the year before. On the flip side, it has US$154.0m in cash leading to net debt of about US$3.59b.

How Strong Is CDW's Balance Sheet?

The latest balance sheet data shows that CDW had liabilities of US$3.49b due within a year, and liabilities of US$3.55b falling due after that. Offsetting these obligations, it had cash of US$154.0m as well as receivables valued at US$3.40b due within 12 months. So it has liabilities totalling US$3.49b more than its cash and near-term receivables, combined.

CDW has a very large market capitalization of US$16.3b, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. But it's clear that we should definitely closely examine whether it can manage its debt without dilution.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

CDW has net debt to EBITDA of 2.6 suggesting it uses a fair bit of leverage to boost returns. But the high interest coverage of 7.1 suggests it can easily service that debt. If CDW can keep growing EBIT at last year's rate of 15% over the last year, then it will find its debt load easier to manage. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine CDW's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Over the most recent three years, CDW recorded free cash flow worth 77% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This cold hard cash means it can reduce its debt when it wants to.

Our View

The good news is that CDW's demonstrated ability to convert EBIT to free cash flow delights us like a fluffy puppy does a toddler. But, on a more sombre note, we are a little concerned by its net debt to EBITDA. Taking all this data into account, it seems to us that CDW takes a pretty sensible approach to debt. While that brings some risk, it can also enhance returns for shareholders. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. Consider risks, for instance. Every company has them, and we've spotted 2 warning signs for CDW you should know about.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About NasdaqGS:CDW

CDW

Provides information technology (IT) solutions in the United States, the United Kingdom, and Canada.

Undervalued with excellent balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Giftify ·

Giftify ($GIFT): A Small-Cap Incentives Platform with More ScaleThan Its Valuation Suggests

Fair Value:US$2.551.6% undervalued

13 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

TR

tripledub on Meta Platforms ·

The $135 Billion Bet That Should Make Every Shareholder Nervous

Fair Value:US$58016.4% overvalued

27 followersusers have followed this narrative

3 commentsusers have commented on this narrative

26 likesusers have liked this narrative

TH

TheBestInvestor on Lockheed Martin ·

Orbit + Aero + Defense

Fair Value:US$673.8823.8% undervalued

14 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on Steppe Gold ·

A case for Steppe Gold, bear case CAD $4, base case CAD $15, bull case CAD $25

Fair Value:CA$2594.4% undervalued

21 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Recently Updated Narratives

RO

Robbo on HiTech Group Australia ·

A baby being thrown out with the AI bathwater?

Fair Value:AU$1.7541.7% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

SO

sorkdhkddlek on Intuitive Machines ·

Strategic Expansion Meets Valuation Reality at $23

Fair Value:US$2311.0% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

SO

sorkdhkddlek on American Electric Power Company ·

AEP: Capturing the Scarcity Value of the American Power Grid

Fair Value:US$11319.2% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TR

tripledub on Microsoft ·

Everyone's Terrified Microsoft Will Keep Spending. I'm Terrified They'll Stop.

Fair Value:US$3957.5% overvalued

52 followersusers have followed this narrative

3 commentsusers have commented on this narrative

43 likesusers have liked this narrative

KI

Kingman1152 on NVIDIA ·

NVIDIA will see a profit margin surge of 55% in the next 5 years

Fair Value:US$305.231.8% undervalued

65 followersusers have followed this narrative

1 commentusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$579.5726.7% undervalued

1387 followersusers have followed this narrative

2 commentsusers have commented on this narrative

11 likesusers have liked this narrative

Trending Discussion

TA

Taurustunez88 on Dangote Sugar Refinery ·

With the N500b rights issue, I believe Dangote sugar refinery’s loss due to FX pressures will be dra...

1

|0

SI

Simply Wall St User on Black Diamond Group ·

I'm guessing but is ATCO the only other Canadian competitor? And who in the US?

0

|0