Advertisement

- India

- /

- Consumer Durables

- /

- NSEI:BPL

BPL Limited's (NSE:BPL) Risks Elevated At These Prices

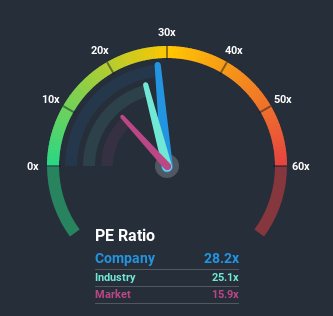

BPL Limited's (NSE:BPL) price-to-earnings (or "P/E") ratio of 28.2x might make it look like a strong sell right now compared to the market in India, where around half of the companies have P/E ratios below 15x and even P/E's below 8x are quite common. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/E.

With earnings growth that's exceedingly strong of late, BPL has been doing very well. It seems that many are expecting the strong earnings performance to beat most other companies over the coming period, which has increased investors’ willingness to pay up for the stock. If not, then existing shareholders might be a little nervous about the viability of the share price.

See our latest analysis for BPL

What Are Growth Metrics Telling Us About The High P/E?

There's an inherent assumption that a company should far outperform the market for P/E ratios like BPL's to be considered reasonable.

If we review the last year of earnings growth, the company posted a terrific increase of 308%. Still, incredibly EPS has fallen 93% in total from three years ago, which is quite disappointing. Accordingly, shareholders would have felt downbeat about the medium-term rates of earnings growth.

Comparing that to the market, which is predicted to deliver 10% growth in the next 12 months, the company's downward momentum based on recent medium-term earnings results is a sobering picture.

With this information, we find it concerning that BPL is trading at a P/E higher than the market. Apparently many investors in the company are way more bullish than recent times would indicate and aren't willing to let go of their stock at any price. There's a very good chance existing shareholders are setting themselves up for future disappointment if the P/E falls to levels more in line with the recent negative growth rates.

The Key Takeaway

Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

We've established that BPL currently trades on a much higher than expected P/E since its recent earnings have been in decline over the medium-term. Right now we are increasingly uncomfortable with the high P/E as this earnings performance is highly unlikely to support such positive sentiment for long. If recent medium-term earnings trends continue, it will place shareholders' investments at significant risk and potential investors in danger of paying an excessive premium.

We don't want to rain on the parade too much, but we did also find 3 warning signs for BPL (1 is significant!) that you need to be mindful of.

Of course, you might find a fantastic investment by looking at a few good candidates. So take a peek at this free list of companies with a strong growth track record, trading on a P/E below 20x.

When trading BPL or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if BPL might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About NSEI:BPL

BPL

Manufactures and sells consumer electronic products primarily in India.

Very low risk and overvalued.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Upside Gold ·

An Undervalued 3.3Moz Gold Project in Canada

Fair Value:CA$5.0775.1% undervalued

127 followersusers have followed this narrative

1 commentusers have commented on this narrative

21 likesusers have liked this narrative

YA

Yang_ on SoFi Technologies ·

SoFi Technologies: The Apex Aggregator and the Infrastructure of the Modern Financial System

Fair Value:US$22.9822.7% undervalued

41 followersusers have followed this narrative

0 commentsusers have commented on this narrative

32 likesusers have liked this narrative

KO

Kouj on CSL ·

CSL: The Dip Is the Opportunity

Fair Value:AU$1559.0% undervalued

17 followersusers have followed this narrative

0 commentsusers have commented on this narrative

13 likesusers have liked this narrative

GA

GavrielH on DHT Holdings ·

DHT Holdings, inc: Strait of Hormuz Risk Amidst US-Israel vs Iran Tensions Spikes VLCC Rates.

Fair Value:US$3653.2% undervalued

15 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Recently Updated Narratives

VE

Vestra on MasTec ·

MasTec Inc. (MTZ): The Infrastructure Super-Cycle and the $19 Billion Backlog Milestone

Fair Value:US$33613.7% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

SA

Sax on Super Retail Group ·

Fair Value Intriguingly Set at $11.54 for SUL Investors

Fair Value:AU$13.431.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VE

Vestra on Dell Technologies ·

Dell Technologies (DELL): The AI Infrastructure Super-Cycle and the $50 Billion Server Milestone

Fair Value:US$193.521.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

KA

kabz2342 on Nu Holdings ·

Nu holdings will continue to disrupt the South American banking market

Fair Value:US$64.378.4% undervalued

53 followersusers have followed this narrative

3 commentsusers have commented on this narrative

28 likesusers have liked this narrative

YA

Yang_ on SoFi Technologies ·

SoFi Technologies: The Apex Aggregator and the Infrastructure of the Modern Financial System

Fair Value:US$22.9822.7% undervalued

41 followersusers have followed this narrative

0 commentsusers have commented on this narrative

32 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$59633.6% undervalued

1309 followersusers have followed this narrative

2 commentsusers have commented on this narrative

10 likesusers have liked this narrative

Trending Discussion

DA

daqui_luis on Corticeira Amorim S.G.P.S ·

Great analysis on a great and solid company with a dominant position in the Cork Market.

1

|0