Stock Analysis

Bannari Amman Sugars Limited's (NSE:BANARISUG) Business Is Trailing The Market But Its Shares Aren't

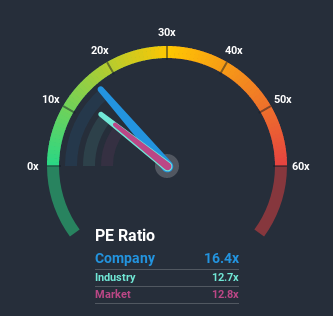

When close to half the companies in India have price-to-earnings ratios (or "P/E's") below 12x, you may consider Bannari Amman Sugars Limited (NSE:BANARISUG) as a stock to potentially avoid with its 16.4x P/E ratio. However, the P/E might be high for a reason and it requires further investigation to determine if it's justified.

The earnings growth achieved at Bannari Amman Sugars over the last year would be more than acceptable for most companies. It might be that many expect the respectable earnings performance to beat most other companies over the coming period, which has increased investors’ willingness to pay up for the stock. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

Check out our latest analysis for Bannari Amman Sugars

Is There Enough Growth For Bannari Amman Sugars?

The only time you'd be truly comfortable seeing a P/E as high as Bannari Amman Sugars' is when the company's growth is on track to outshine the market.

If we review the last year of earnings growth, the company posted a terrific increase of 26%. Still, incredibly EPS has fallen 39% in total from three years ago, which is quite disappointing. So unfortunately, we have to acknowledge that the company has not done a great job of growing earnings over that time.

This is in contrast to the rest of the market, which is expected to decline by 3.2% over the next year, or less than the company's recent medium-term annualised earnings decline.

With this information, it's strange that Bannari Amman Sugars is trading at a higher P/E in comparison. In general, when earnings shrink rapidly the P/E premium often shrinks too, which could set up shareholders for future disappointment. Maintaining these prices will be extremely difficult to achieve as a continuation of recent earnings trends is likely to weigh down the shares eventually.

The Final Word

Using the price-to-earnings ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

Our examination of Bannari Amman Sugars revealed its sharp three-year contraction in earnings isn't impacting its high P/E anywhere near as much as we would have predicted, given the market is set to shrink less severely. When we see below average earnings, we suspect the share price is at risk of declining, sending the high P/E lower. We're also cautious about the company's ability to stay its recent medium-term course and resist even greater pain to its business from the broader market turmoil. Unless the company's relative performance improves markedly, it's very challenging to accept these prices as being reasonable.

We don't want to rain on the parade too much, but we did also find 3 warning signs for Bannari Amman Sugars (1 makes us a bit uncomfortable!) that you need to be mindful of.

Of course, you might also be able to find a better stock than Bannari Amman Sugars. So you may wish to see this free collection of other companies that sit on P/E's below 20x and have grown earnings strongly.

When trading Bannari Amman Sugars or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're helping make it simple.

Find out whether Bannari Amman Sugars is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About NSEI:BANARISUG

Bannari Amman Sugars

Engages in the manufacture and sale of sugar in India.

Flawless balance sheet with acceptable track record.