Advertisement

- South Korea

- /

- Hospitality

- /

- KOSE:A032350

Asian Value Stock Highlights Featuring Lotte Tour Development And 2 More Discounted Picks

Simply Wall St

Reviewed by Simply Wall St

Amidst escalating geopolitical tensions and fluctuating trade talks, Asian markets have experienced mixed performances, with some indices showing resilience despite broader global uncertainties. In this environment, identifying undervalued stocks can be particularly appealing for investors seeking opportunities that may offer growth potential at a discounted price.

Top 10 Undervalued Stocks Based On Cash Flows In Asia

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Taiyo Yuden (TSE:6976) | ¥2356.50 | ¥4700.51 | 49.9% |

| Shenzhen Techwinsemi Technology (SZSE:001309) | CN¥127.36 | CN¥252.41 | 49.5% |

| Shenzhen KSTAR Science and Technology (SZSE:002518) | CN¥21.78 | CN¥43.41 | 49.8% |

| Range Intelligent Computing Technology Group (SZSE:300442) | CN¥42.92 | CN¥85.28 | 49.7% |

| Polaris Holdings (TSE:3010) | ¥217.00 | ¥428.50 | 49.4% |

| PixArt Imaging (TPEX:3227) | NT$221.00 | NT$436.29 | 49.3% |

| Pansoft (SZSE:300996) | CN¥14.19 | CN¥27.97 | 49.3% |

| Good Will Instrument (TWSE:2423) | NT$44.00 | NT$87.14 | 49.5% |

| Food & Life Companies (TSE:3563) | ¥6534.00 | ¥12865.95 | 49.2% |

| Dive (TSE:151A) | ¥921.00 | ¥1829.36 | 49.7% |

Let's uncover some gems from our specialized screener.

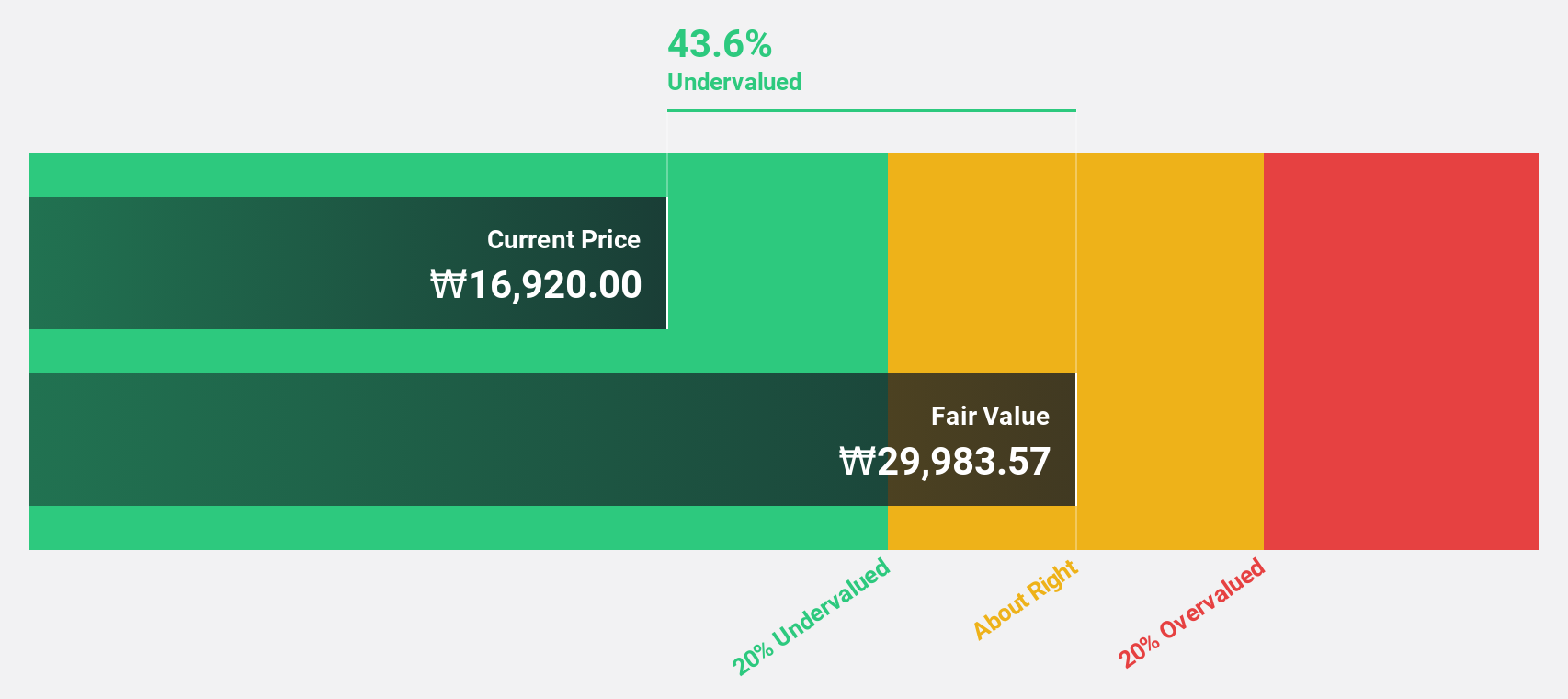

Lotte Tour Development (KOSE:A032350)

Overview: Lotte Tour Development Co., Ltd., along with its subsidiaries, provides travel and tourism services in South Korea and has a market cap of approximately ₩1.12 trillion.

Operations: The company's revenue is primarily derived from the Dream Tower Integrated Resort Division at ₩396.33 billion, followed by the Travel Related Service Sector (excluding Internet Journalism) at ₩88.05 billion, and the Internet Media Sector at ₩2.80 million.

Estimated Discount To Fair Value: 48.6%

Lotte Tour Development is trading at ₩14,690, significantly below its estimated fair value of ₩28,567.61. Despite a net loss reduction from the previous year and forecasted annual earnings growth of 100.42%, the company remains undervalued by over 20%. Revenue is expected to grow at 13.7% annually, outpacing the Korean market average of 6.8%. However, its return on equity is projected to remain low at 3.1% in three years.

- The analysis detailed in our Lotte Tour Development growth report hints at robust future financial performance.

- Delve into the full analysis health report here for a deeper understanding of Lotte Tour Development.

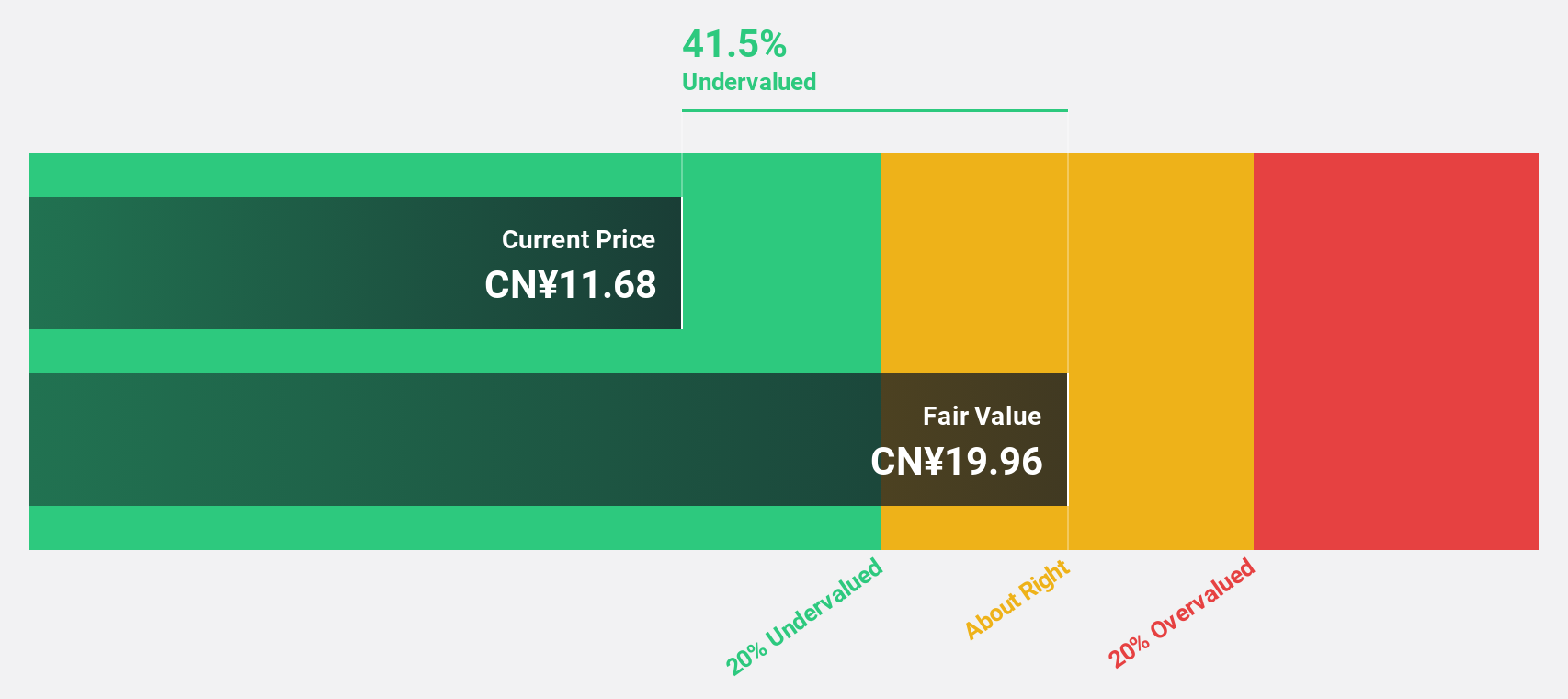

Fujian Longking (SHSE:600388)

Overview: Fujian Longking Co., Ltd. is involved in the manufacture and sale of environmental protection equipment globally, with a market cap of CN¥15.29 billion.

Operations: Fujian Longking generates its revenue from the global manufacture and sale of environmental protection equipment.

Estimated Discount To Fair Value: 39.6%

Fujian Longking is trading at CN¥12.11, well below its estimated fair value of CN¥20.05, suggesting it is undervalued by over 20%. Despite a decline in recent quarterly sales to CNY 1.97 billion from CNY 2.28 billion a year ago, earnings grew significantly last year and are forecast to grow annually by 26.61%, outpacing the Chinese market average of 23.2%. However, free cash flows do not adequately cover the dividend yield of 2.31%.

- Insights from our recent growth report point to a promising forecast for Fujian Longking's business outlook.

- Navigate through the intricacies of Fujian Longking with our comprehensive financial health report here.

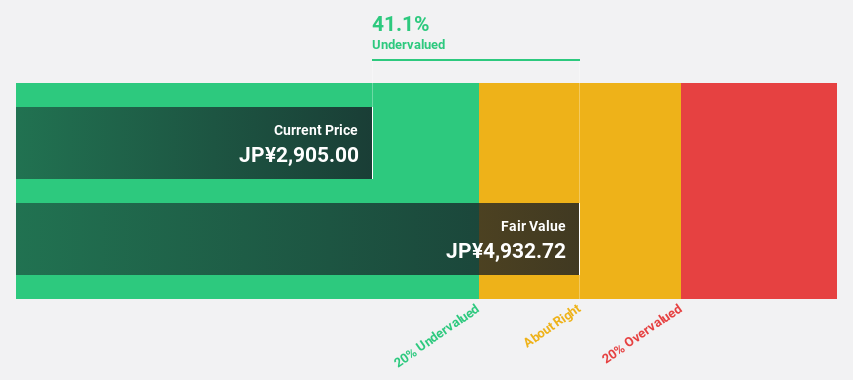

DMG Mori (TSE:6141)

Overview: DMG Mori Co., Ltd. is a global manufacturer and seller of machine tools, with a market cap of ¥440.76 billion.

Operations: The company's revenue is primarily derived from Machine Tools at ¥614.80 billion and Industrial Service at ¥225.18 billion, with additional contributions from corporate services totaling ¥1.71 million.

Estimated Discount To Fair Value: 36.3%

DMG Mori is trading at ¥3109, significantly below its estimated fair value of ¥4880.72, indicating it is undervalued by over 20%. Despite a volatile share price recently, earnings are projected to grow substantially at 24.46% annually over the next three years, outpacing the Japanese market average. However, profit margins have decreased from last year and dividends are not well covered by cash flows or earnings.

- Our earnings growth report unveils the potential for significant increases in DMG Mori's future results.

- Click here and access our complete balance sheet health report to understand the dynamics of DMG Mori.

Turning Ideas Into Actions

- Click here to access our complete index of 292 Undervalued Asian Stocks Based On Cash Flows.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About KOSE:A032350

Lotte Tour Development

Engages in the provision of travel and tourism services in South Korea.

Reasonable growth potential and fair value.

Market Insights

Advertisement

Community Narratives

Vita Life Sciences Set for a 12.72% Revenue Growth While Tackling Operational Challenges

Fair Value AU$2.42|12.0% undervalued

RO

Community Contributor

Vossloh rides a €500 billion wave to boost growth and earnings in the next decade

Fair Value €78.41|5.2% undervalued

CH

Community Contributor

Intuitive Surgical Will Transform Healthcare with 12% Revenue Growth

Fair Value US$325.55|57.3% overvalued

UN

Community Contributor