Advertisement

As global markets react to new U.S. tariffs, Asian stocks have shown resilience, with China's indices rising amid hopes for additional economic stimulus. In such an environment, dividend stocks in Asia can offer a stable income stream and potential growth opportunities for investors looking to diversify their portfolios.

Top 10 Dividend Stocks In Asia

| Name | Dividend Yield | Dividend Rating |

| Yamato Kogyo (TSE:5444) | 4.38% | ★★★★★★ |

| Wuliangye YibinLtd (SZSE:000858) | 5.07% | ★★★★★★ |

| NCD (TSE:4783) | 4.34% | ★★★★★★ |

| Japan Excellent (TSE:8987) | 4.28% | ★★★★★★ |

| HUAYU Automotive Systems (SHSE:600741) | 4.34% | ★★★★★★ |

| Guangxi LiuYao Group (SHSE:603368) | 4.39% | ★★★★★★ |

| GakkyushaLtd (TSE:9769) | 4.49% | ★★★★★★ |

| E J Holdings (TSE:2153) | 4.98% | ★★★★★★ |

| DoshishaLtd (TSE:7483) | 4.08% | ★★★★★★ |

| Daicel (TSE:4202) | 4.78% | ★★★★★★ |

Click here to see the full list of 1201 stocks from our Top Asian Dividend Stocks screener.

Here we highlight a subset of our preferred stocks from the screener.

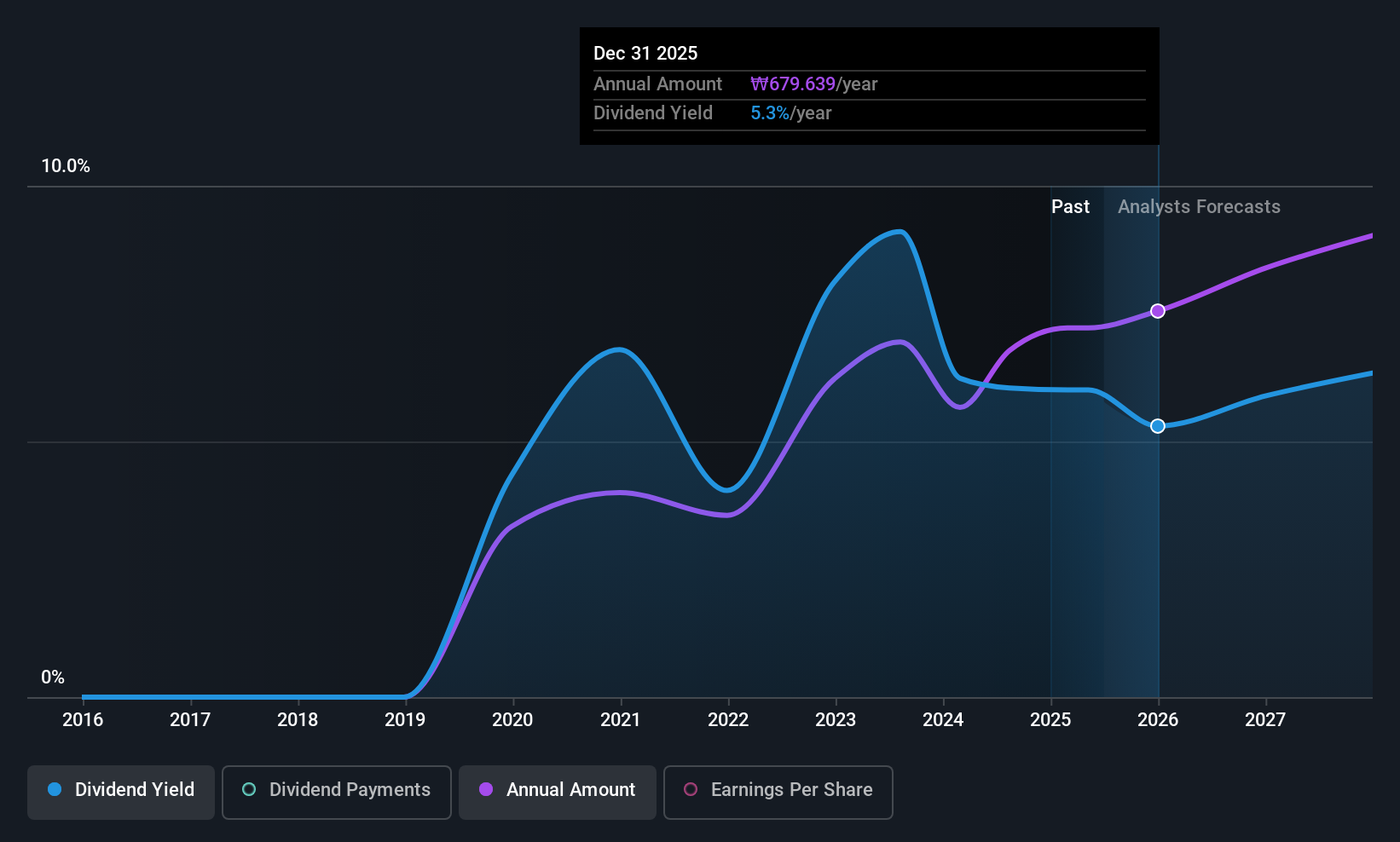

BNK Financial Group (KOSE:A138930)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: BNK Financial Group Inc., along with its subsidiaries, offers a range of financial products and services both in South Korea and internationally, with a market cap of ₩5.02 trillion.

Operations: BNK Financial Group's revenue is primarily derived from its subsidiaries, including Busan Bank (₩1.29 trillion), Gyeongnam Bank (₩954.54 billion), BNK Capital (₩179.62 billion), BNK Savings Bank (₩43.35 billion), and BNK Investments Securities (₩76.07 billion).

Dividend Yield: 4.1%

BNK Financial Group's dividend yield is in the top 25% of the Korean market, offering a competitive return. However, its track record shows volatility and unreliability, with dividends paid for less than 10 years and experiencing significant drops. Despite this, current and forecasted payout ratios suggest dividends are well-covered by earnings at 33.9% and expected to be 28.1%. Recent Q1 net income was KRW 166.6 billion, supporting dividend sustainability efforts despite past inconsistencies.

- Click here to discover the nuances of BNK Financial Group with our detailed analytical dividend report.

- Our comprehensive valuation report raises the possibility that BNK Financial Group is priced lower than what may be justified by its financials.

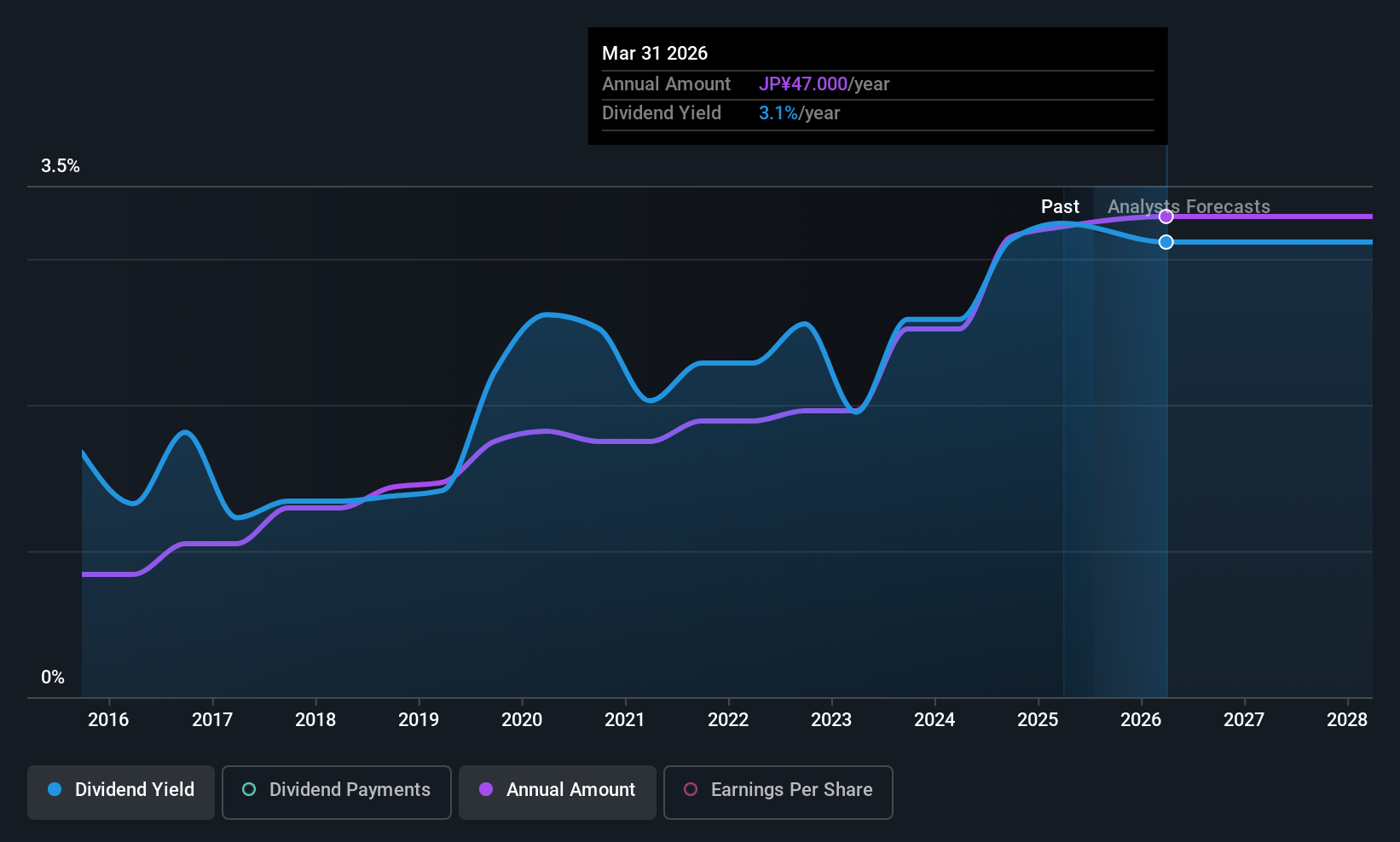

Hirakawa Hewtech (TSE:5821)

Simply Wall St Dividend Rating: ★★★★★☆

Overview: Hirakawa Hewtech Corp. is engaged in the manufacturing and sale of cables, assemblies, electric and electronic equipment, as well as medical equipment and parts both in Japan and internationally, with a market cap of ¥26.21 billion.

Operations: Hirakawa Hewtech Corp.'s revenue segments include the production and distribution of cables, assemblies, electric and electronic equipment, along with medical equipment and parts.

Dividend Yield: 3.2%

Hirakawa Hewtech's dividend reliability is underscored by stable and growing payouts over the past decade, with recent increases from ¥18.00 to ¥23.00 per share and expectations of further rises. The company's dividends are well-covered by earnings (payout ratio: 25.6%) and cash flows (cash payout ratio: 36.4%), ensuring sustainability despite a yield of 3.16% being below Japan's top quartile payers. Recent board decisions on treasury shares disposal may influence future financial strategies.

- Click to explore a detailed breakdown of our findings in Hirakawa Hewtech's dividend report.

- The analysis detailed in our Hirakawa Hewtech valuation report hints at an inflated share price compared to its estimated value.

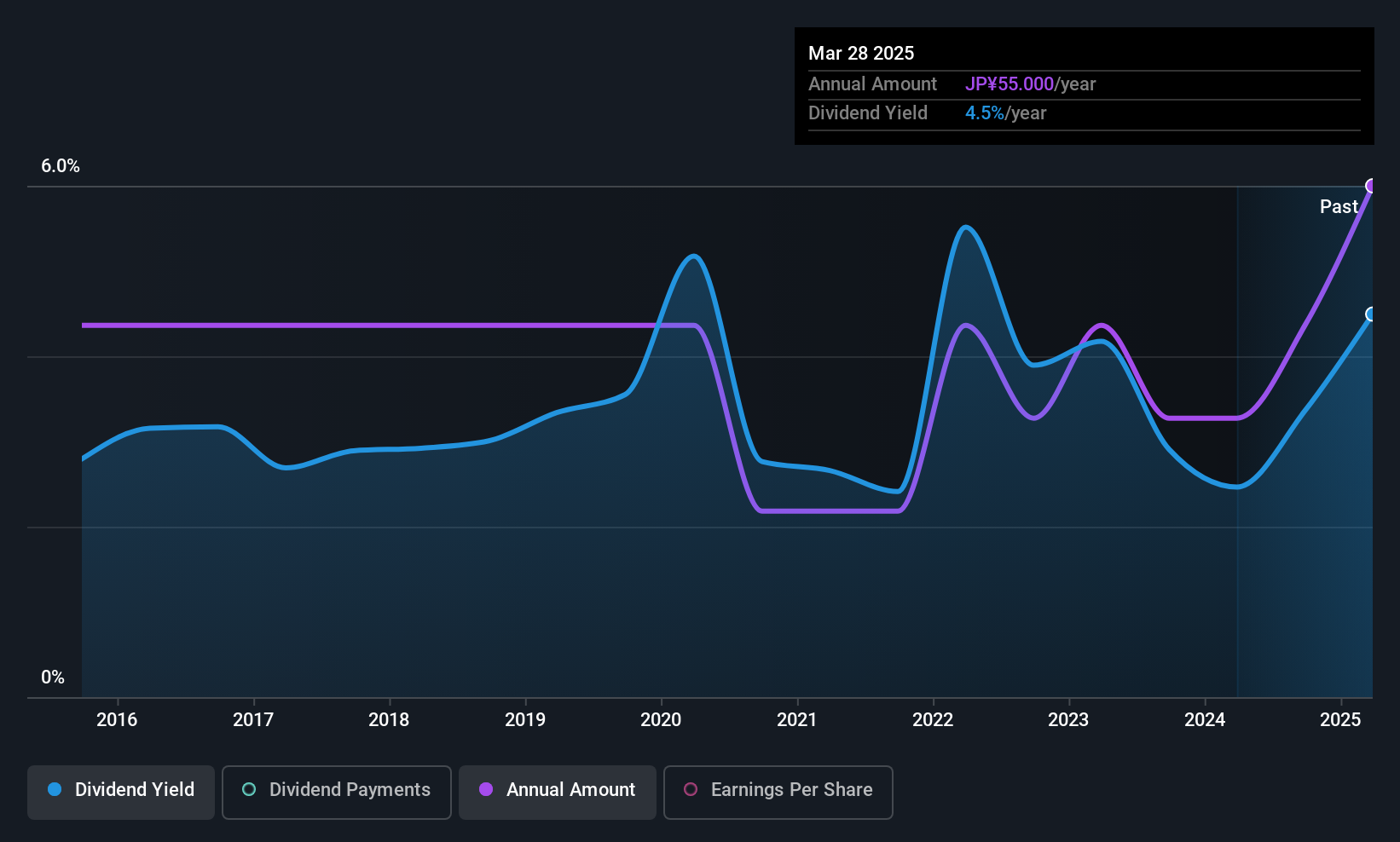

Komori (TSE:6349)

Simply Wall St Dividend Rating: ★★★★★☆

Overview: Komori Corporation manufactures, sells, and repairs printing presses across Japan, North America, Europe, and Greater China with a market cap of ¥83.73 billion.

Operations: Komori Corporation's revenue is primarily derived from its operations in the manufacturing, sales, and repair of printing presses across various regions including Japan, North America, Europe, and Greater China.

Dividend Yield: 4.4%

Komori's dividend profile is marked by a volatile track record despite recent increases, with dividends well-covered by earnings (payout ratio: 29.6%) and cash flows (cash payout ratio: 25.2%). The yield of 4.44% ranks in Japan's top quartile, yet the company recently reduced its guidance from ¥48 to ¥35 per share for fiscal year-end March 2026. Executive changes and a renewed takeover defense policy may affect future strategic direction.

- Delve into the full analysis dividend report here for a deeper understanding of Komori.

- Our valuation report unveils the possibility Komori's shares may be trading at a discount.

Turning Ideas Into Actions

- Embark on your investment journey to our 1201 Top Asian Dividend Stocks selection here.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Komori might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:6349

Komori

Engages in the manufacture, sale, and repair of printing presses in Japan, North America, Europe, and Greater China.

Excellent balance sheet established dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|33.3% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|23.4% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|8.5% overvalued

DA

Community Contributor