Stock Analysis

- United States

- /

- Aerospace & Defense

- /

- NYSE:DCO

We Think Shareholders May Want To Consider A Review Of Ducommun Incorporated's (NYSE:DCO) CEO Compensation Package

Key Insights

- Ducommun to hold its Annual General Meeting on 24th of April

- Salary of US$959.7k is part of CEO Steve Oswald's total remuneration

- The overall pay is 167% above the industry average

- Ducommun's EPS declined by 24% over the past three years while total shareholder loss over the past three years was 9.3%

The results at Ducommun Incorporated (NYSE:DCO) have been quite disappointing recently and CEO Steve Oswald bears some responsibility for this. Shareholders can take the chance to hold the board and management accountable for the unsatisfactory performance at the next AGM on 24th of April. This will be also be a chance where they can challenge the board on company direction and vote on resolutions such as executive remuneration. The data we present below explains why we think CEO compensation is not consistent with recent performance.

See our latest analysis for Ducommun

Comparing Ducommun Incorporated's CEO Compensation With The Industry

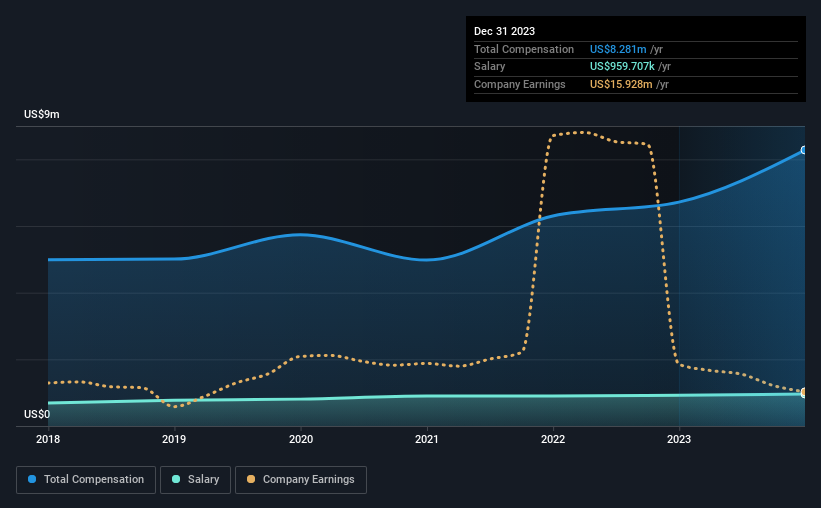

At the time of writing, our data shows that Ducommun Incorporated has a market capitalization of US$811m, and reported total annual CEO compensation of US$8.3m for the year to December 2023. Notably, that's an increase of 23% over the year before. We think total compensation is more important but our data shows that the CEO salary is lower, at US$960k.

On comparing similar companies from the American Aerospace & Defense industry with market caps ranging from US$400m to US$1.6b, we found that the median CEO total compensation was US$3.1m. Hence, we can conclude that Steve Oswald is remunerated higher than the industry median. Moreover, Steve Oswald also holds US$20m worth of Ducommun stock directly under their own name, which reveals to us that they have a significant personal stake in the company.

| Component | 2023 | 2022 | Proportion (2023) |

| Salary | US$960k | US$924k | 12% |

| Other | US$7.3m | US$5.8m | 88% |

| Total Compensation | US$8.3m | US$6.7m | 100% |

On an industry level, roughly 22% of total compensation represents salary and 78% is other remuneration. In Ducommun's case, non-salary compensation represents a greater slice of total remuneration, in comparison to the broader industry. If total compensation is slanted towards non-salary benefits, it indicates that CEO pay is linked to company performance.

Ducommun Incorporated's Growth

Over the last three years, Ducommun Incorporated has shrunk its earnings per share by 24% per year. It achieved revenue growth of 6.2% over the last year.

Overall this is not a very positive result for shareholders. And the modest revenue growth over 12 months isn't much comfort against the reduced EPS. These factors suggest that the business performance wouldn't really justify a high pay packet for the CEO. Looking ahead, you might want to check this free visual report on analyst forecasts for the company's future earnings..

Has Ducommun Incorporated Been A Good Investment?

Given the total shareholder loss of 9.3% over three years, many shareholders in Ducommun Incorporated are probably rather dissatisfied, to say the least. So shareholders would probably want the company to be less generous with CEO compensation.

In Summary...

Given that shareholders haven't seen any positive returns on their investment, not to mention the lack of earnings growth, this may suggest that few of them would be willing to award the CEO with a pay rise. At the upcoming AGM, they can question the management's plans and strategies to turn performance around and reassess their investment thesis in regards to the company.

While it is important to pay attention to CEO remuneration, investors should also consider other elements of the business. That's why we did some digging and identified 3 warning signs for Ducommun that you should be aware of before investing.

Of course, you might find a fantastic investment by looking at a different set of stocks. So take a peek at this free list of interesting companies.

Valuation is complex, but we're helping make it simple.

Find out whether Ducommun is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:DCO

Ducommun

Ducommun Incorporated provides engineering and manufacturing services for products and applications used primarily in the aerospace and defense, industrial, medical, and other industries in the United States.

Adequate balance sheet and fair value.