Stock Analysis

- South Africa

- /

- Metals and Mining

- /

- JSE:AMS

Anglo American Platinum Limited's (JSE:AMS) Business Is Yet to Catch Up With Its Share Price

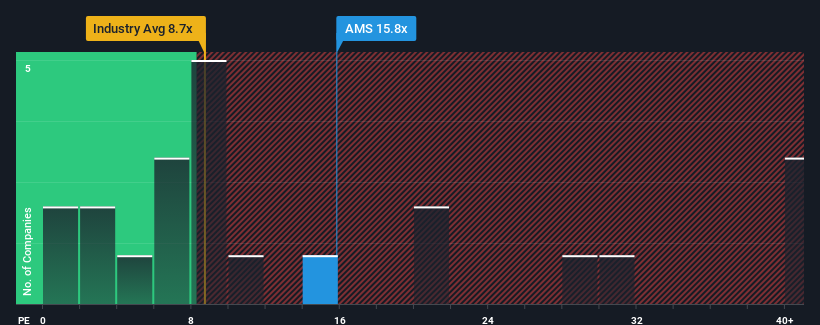

With a price-to-earnings (or "P/E") ratio of 15.8x Anglo American Platinum Limited (JSE:AMS) may be sending very bearish signals at the moment, given that almost half of all companies in South Africa have P/E ratios under 8x and even P/E's lower than 5x are not unusual. However, the P/E might be quite high for a reason and it requires further investigation to determine if it's justified.

Anglo American Platinum hasn't been tracking well recently as its declining earnings compare poorly to other companies, which have seen some growth on average. One possibility is that the P/E is high because investors think this poor earnings performance will turn the corner. If not, then existing shareholders may be extremely nervous about the viability of the share price.

Check out our latest analysis for Anglo American Platinum

Does Growth Match The High P/E?

There's an inherent assumption that a company should far outperform the market for P/E ratios like Anglo American Platinum's to be considered reasonable.

Retrospectively, the last year delivered a frustrating 73% decrease to the company's bottom line. The last three years don't look nice either as the company has shrunk EPS by 57% in aggregate. So unfortunately, we have to acknowledge that the company has not done a great job of growing earnings over that time.

Turning to the outlook, the next three years should generate growth of 8.3% per year as estimated by the twelve analysts watching the company. Meanwhile, the rest of the market is forecast to expand by 11% per year, which is noticeably more attractive.

In light of this, it's alarming that Anglo American Platinum's P/E sits above the majority of other companies. It seems most investors are hoping for a turnaround in the company's business prospects, but the analyst cohort is not so confident this will happen. Only the boldest would assume these prices are sustainable as this level of earnings growth is likely to weigh heavily on the share price eventually.

The Final Word

We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

We've established that Anglo American Platinum currently trades on a much higher than expected P/E since its forecast growth is lower than the wider market. When we see a weak earnings outlook with slower than market growth, we suspect the share price is at risk of declining, sending the high P/E lower. This places shareholders' investments at significant risk and potential investors in danger of paying an excessive premium.

Plus, you should also learn about these 2 warning signs we've spotted with Anglo American Platinum (including 1 which shouldn't be ignored).

If these risks are making you reconsider your opinion on Anglo American Platinum, explore our interactive list of high quality stocks to get an idea of what else is out there.

Valuation is complex, but we're helping make it simple.

Find out whether Anglo American Platinum is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Simply Wall St

About JSE:AMS

Anglo American Platinum

Anglo American Platinum Limited engages in the production and supply of platinum group metals, base metals, and precious metals in South Africa, Asia, Europe, North America, and internationally.

Flawless balance sheet and slightly overvalued.