Advertisement

- United States

- /

- Medical Equipment

- /

- NasdaqGS:TRIB

Are Trinity Biotech plc's (NASDAQ:TRIB) Interest Costs Too High?

While small-cap stocks, such as Trinity Biotech plc (NASDAQ:TRIB) with its market cap of US$62m, are popular for their explosive growth, investors should also be aware of their balance sheet to judge whether the company can survive a downturn. Companies operating in the Medical Equipment industry, in particular ones that run negative earnings, are more likely to be higher risk. Assessing first and foremost the financial health is essential. Here are a few basic checks that are good enough to have a broad overview of the company’s financial strength. Though, given that I have not delve into the company-specifics, I suggest you dig deeper yourself into TRIB here.

How does TRIB’s operating cash flow stack up against its debt?

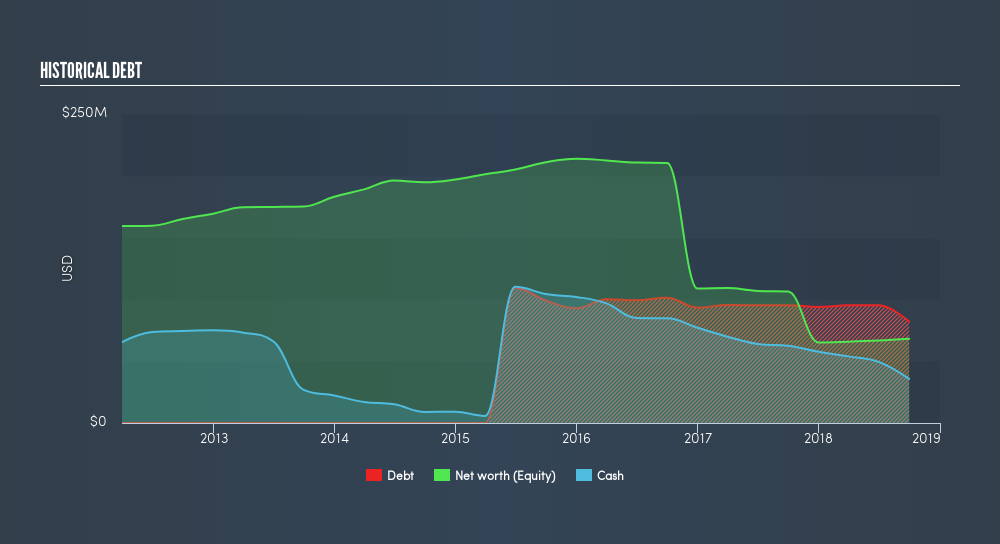

Over the past year, TRIB has reduced its debt from US$95m to US$82m – this includes long-term debt. With this reduction in debt, TRIB currently has US$36m remaining in cash and short-term investments , ready to deploy into the business. Additionally, TRIB has produced cash from operations of US$7.1m during the same period of time, resulting in an operating cash to total debt ratio of 8.6%, signalling that TRIB’s current level of operating cash is not high enough to cover debt. This ratio can also be a sign of operational efficiency for loss making businesses since metrics such as return on asset (ROA) requires a positive net income. In TRIB’s case, it is able to generate 0.086x cash from its debt capital.

Can TRIB pay its short-term liabilities?

At the current liabilities level of US$21m, the company has been able to meet these obligations given the level of current assets of US$93m, with a current ratio of 4.48x. Having said that, a ratio above 3x may be considered excessive by some investors.

Does TRIB face the risk of succumbing to its debt-load?

Since total debt levels have outpaced equities, TRIB is a highly leveraged company. This is not uncommon for a small-cap company given that debt tends to be lower-cost and at times, more accessible. However, since TRIB is currently loss-making, sustainability of its current state of operations becomes a concern. Running high debt, while not yet making money, can be risky in unexpected downturns as liquidity may dry up, making it hard to operate.

Next Steps:

Although TRIB’s debt level is towards the higher end of the spectrum, its cash flow coverage seems adequate to meet obligations which means its debt is being efficiently utilised. This may mean this is an optimal capital structure for the business, given that it is also meeting its short-term commitment. I admit this is a fairly basic analysis for TRIB's financial health. Other important fundamentals need to be considered alongside. You should continue to research Trinity Biotech to get a better picture of the small-cap by looking at:

- Historical Performance: What has TRIB's returns been like over the past? Go into more detail in the past track record analysis and take a look at the free visual representations of our analysis for more clarity.

- Other High-Performing Stocks: Are there other stocks that provide better prospects with proven track records? Explore our free list of these great stocks here.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About NasdaqGS:TRIB

Trinity Biotech

Acquires, together with its subsidiaries, develops, acquires, manufactures, and markets medical diagnostic products for the clinical laboratory and point-of-care (POC) segments of the diagnostic market in the Americas, Asia, Africa, and Europe.

Moderate and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

Vita Life Sciences Set for a 12.72% Revenue Growth While Tackling Operational Challenges

Fair Value AU$2.42|8.7% undervalued

RO

Community Contributor

Vossloh rides a €500 billion wave to boost growth and earnings in the next decade

Fair Value €78.41|7.2% undervalued

CH

Community Contributor

Intuitive Surgical Will Transform Healthcare with 12% Revenue Growth

Fair Value US$325.55|56.5% overvalued

UN

Community Contributor