Advertisement

- United States

- /

- Aerospace & Defense

- /

- NYSE:DCO

Are Ducommun's (NYSE:DCO) Statutory Earnings A Good Reflection Of Its Earnings Potential?

Statistically speaking it is less risky to invest in profitable companies than in unprofitable ones. That said, the current statutory profit is not always a good guide to a company's underlying profitability. This article will consider whether Ducommun's (NYSE:DCO) statutory profits are a good guide to its underlying earnings.

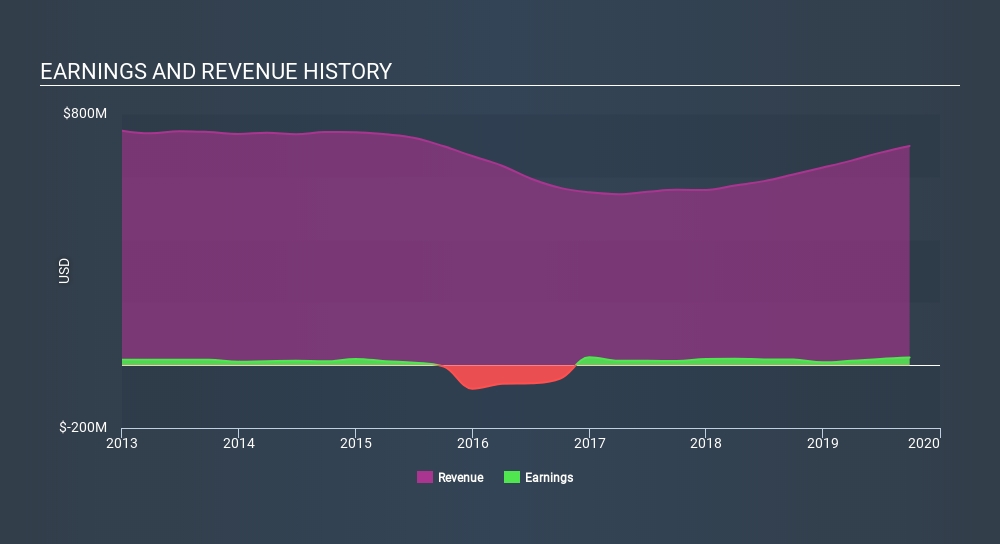

While Ducommun was able to generate revenue of US$698.3m in the last twelve months, we think its profit result of US$24.3m was more important. The good news is that the company managed to grow its revenue over the last three years, and also move from loss-making to profitable.

Check out our latest analysis for Ducommun

Not all profits are equal, and we can learn more about the nature of a company's past profitability by diving deeper into the financial statements. This article will focus on the impact unusual items have had on Ducommun's statutory earnings. That might leave you wondering what analysts are forecasting in terms of future profitability. Luckily, you can click here to see an interactive graph depicting future profitability, based on their estimates.

The Impact Of Unusual Items On Profit

Importantly, our data indicates that Ducommun's profit was reduced by US$7.0m, due to unusual items, over the last year. While deductions due to unusual items are disappointing in the first instance, there is a silver lining. We looked at thousands of listed companies and found that unusual items are very often one-off in nature. And that's hardly a surprise given these line items are considered unusual. Assuming those unusual expenses don't come up again, we'd therefore expect Ducommun to produce a higher profit next year, all else being equal.

Our Take On Ducommun's Profit Performance

Unusual items (expenses) detracted from Ducommun's earnings over the last year, but we might see an improvement next year. Because of this, we think Ducommun's earnings potential is at least as good as it seems, and maybe even better! And the EPS is up 35% over the last twelve months. The goal of this article has been to assess how well we can rely on the statutory earnings to reflect the company's potential, but there is plenty more to consider. Ultimately, this article has formed an opinion based on historical data. However, it can also be great to think about what analysts are forecasting for the future. At Simply Wall St, we have analyst estimates which you can view by clicking here.

Today we've zoomed in on a single data point to better understand the nature of Ducommun's profit. But there are plenty of other ways to inform your opinion of a company. For example, many people consider a high return on equity as an indication of favorable business economics, while others like to 'follow the money' and search out stocks that insiders are buying. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying to be useful.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About NYSE:DCO

Ducommun

Provides engineering and manufacturing services for products and applications used in the aerospace and defense, industrial, medical, and other industries in the United States.

Excellent balance sheet and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

WhiteCap Is Positioned To Profit Regardless Of Trump's Policy

Fair Value CA$22.60|61.5% undervalued

ST

Equity Analyst and Writer

Microsoft's Evolution Will Drive Revenue to New Heights Fueled by AI

Fair Value US$360.00|30.7% overvalued

BR

Community Contributor

A CASE FOR USD$2.50 (CAD$3.44) BY 2028 (A 5-10 BAGGER)

Fair Value CA$3.44|88.1% undervalued

AG

Community Contributor