Advertisement

Analysts Are Much More Bearish On PledPharma AB (STO:PLED) Than They Used To Be

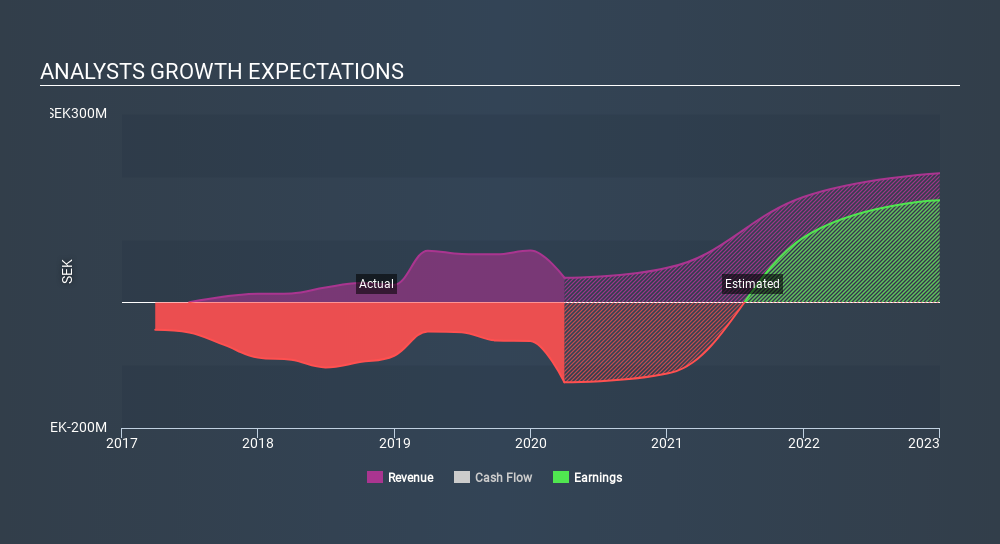

The latest analyst coverage could presage a bad day for PledPharma AB (STO:PLED), with the analysts making across-the-board cuts to their statutory estimates that might leave shareholders a little shell-shocked. Revenue and earnings per share (EPS) forecasts were both revised downwards, with analysts seeing grey clouds on the horizon.

Following the downgrade, the most recent consensus for PledPharma from its twin analysts is for revenues of kr55m in 2020 which, if met, would be a huge 40% increase on its sales over the past 12 months. The loss per share is expected to ameliorate slightly, reducing to kr2.35. Yet before this consensus update, the analysts had been forecasting revenues of kr107m and losses of kr2.11 per share in 2020. So there's been quite a change-up of views after the recent consensus updates, with the analysts making a serious cut to their revenue forecasts while also expecting losses per share to increase.

See our latest analysis for PledPharma

The consensus price target fell 39% to kr16.50, implicitly signalling that lower earnings per share are a leading indicator for PledPharma's valuation. It could also be instructive to look at the range of analyst estimates, to evaluate how different the outlier opinions are from the mean. There are some variant perceptions on PledPharma, with the most bullish analyst valuing it at kr22.00 and the most bearish at kr11.00 per share. Note the wide gap in analyst price targets? This implies to us that there is a fairly broad range of possible scenarios for the underlying business.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the PledPharma's past performance and to peers in the same industry. We would highlight that PledPharma's revenue growth is expected to slow, with forecast 40% increase next year well below the historical 67% p.a. growth over the last three years. By way of comparison, the other companies in this industry with analyst coverage are forecast to grow their revenue at 12% next year. So it's pretty clear that, while PledPharma's revenue growth is expected to slow, it's still expected to grow faster than the industry itself.

The Bottom Line

The most important thing to note from this downgrade is that the consensus increased its forecast losses this year, suggesting all may not be well at PledPharma. Unfortunately, analysts also downgraded their revenue estimates, although our data indicates revenues are expected to perform better than the wider market. After such a stark change in sentiment from analysts, we'd understand if readers now felt a bit wary of PledPharma.

Even so, the longer term trajectory of the business is much more important for the value creation of shareholders. At least one analyst has provided forecasts out to 2022, which can be seen for free on our platform here.

Of course, seeing company management invest large sums of money in a stock can be just as useful as knowing whether analysts are downgrading their estimates. So you may also wish to search this free list of stocks that insiders are buying.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About OM:EGTX

Egetis Therapeutics

A pharmaceutical company, focuses on projects in late-stage development for the treatment of serious diseases with unmet medical needs in the orphan drug segment.

High growth potential with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

WhiteCap Is Positioned To Profit Regardless Of Trump's Policy

Fair Value CA$22.60|61.5% undervalued

ST

Equity Analyst and Writer

Microsoft's Evolution Will Drive Revenue to New Heights Fueled by AI

Fair Value US$360.00|30.7% overvalued

BR

Community Contributor

A CASE FOR USD$2.50 (CAD$3.44) BY 2028 (A 5-10 BAGGER)

Fair Value CA$3.44|88.1% undervalued

AG

Community Contributor