Catalysts

About Donaldson Company

Donaldson Company provides filtration products and services across mobile, industrial and life sciences applications.

What are the underlying business or industry changes driving this perspective?

- Power generation order books tied to data center and AI projects are already described as full through the rest of fiscal 2026. Any project delays, site readiness issues or slower build activity could cap incremental filtration demand and limit revenue growth beyond the current backlog.

- The heavy project based nature of power generation and Aerospace and Defense creates timing swings. As the company runs at high utilization, even small execution issues or customer driven pushouts could pressure gross margin and keep operating margin below current record levels.

- Life Sciences growth in Food and Beverage and Disk Drive benefits from project timing and share gains. However, management already expects profit margins to moderate from Q1 levels, so a return to mid single digit profitability could temper earnings growth if mix shifts away from higher margin projects.

- Disk Drive and microelectronics filtration are tied to AI and cloud storage demand. Any slowdown in storage technology transitions such as HAMR adoption or changes in data center cooling approaches could flatten volume growth and restrain both segment revenue and incremental margins.

- Footprint and cost optimization efforts are still in the heavy lift and ramp up phase. If start up costs in new facilities or execution issues run higher or longer than expected, the intended structural efficiencies could be delayed, weighing on gross margin expansion and overall EPS.

Assumptions

This narrative explores a more pessimistic perspective on Donaldson Company compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts. How have these above catalysts been quantified?

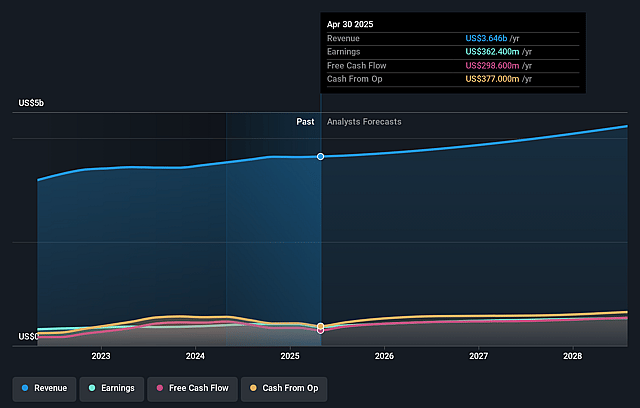

- The bearish analysts are assuming Donaldson Company's revenue will grow by 4.1% annually over the next 3 years.

- The bearish analysts assume that profit margins will increase from 10.2% today to 13.3% in 3 years time.

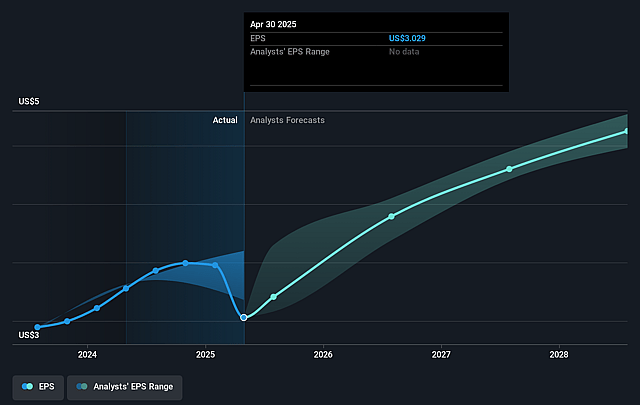

- The bearish analysts expect earnings to reach $557.4 million (and earnings per share of $4.96) by about January 2029, up from $381.9 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 18.3x on those 2029 earnings, down from 28.7x today. This future PE is lower than the current PE for the US Machinery industry at 26.3x.

- The bearish analysts expect the number of shares outstanding to decline by 3.5% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.47%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?

- Donaldson is tied into several long-term secular themes such as data center and AI infrastructure, where power generation order books are already full through the rest of fiscal 2026, and ongoing demand for electricity and cloud capacity could support filtration projects and replacement parts, which would support revenue and earnings.

- The razor to sell razorblades model in Mobile Solutions and Industrial Solutions, where more than half of industrial sales already come from replacement parts, creates a recurring revenue base that can be less sensitive to short term cycles, which may help sustain sales, gross margin and operating margin.

- Life Sciences is seeing double digit growth in Food and Beverage and Disk Drive, with share gains and new technologies for HAMR and liquid cooling in data centers, so if these long-term trends continue, they could support a higher mix of higher margin businesses and keep net margins and earnings resilient.

- Footprint and cost optimization efforts are nearing completion, and management expects structural efficiencies, gross margin expansion and incremental margins above 40% at the midpoint of fiscal 2026 guidance. If execution remains on track, that could support operating margin and earnings.

- Consistent capital allocation through 70 years of dividends, 30 consecutive years of dividend increases and planned 2% to 3% annual share repurchases signal ongoing cash generation and balance sheet strength. This could support earnings per share even if top line growth moderates.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bearish price target for Donaldson Company is $77.0, which represents up to two standard deviations below the consensus price target of $97.2. This valuation is based on what can be assumed as the expectations of Donaldson Company's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $120.0, and the most bearish reporting a price target of just $77.0.

- In order for you to agree with the more bearish analyst cohort, you'd need to believe that by 2029, revenues will be $4.2 billion, earnings will come to $557.4 million, and it would be trading on a PE ratio of 18.3x, assuming you use a discount rate of 8.5%.

- Given the current share price of $94.94, the analyst price target of $77.0 is 23.3% lower. Despite analysts expecting the underlying business to improve, they seem to believe the market's expectations are too high.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Donaldson Company?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.