Last Update 08 Apr 26

Fair value Decreased 0.13%YUMC: Share Buybacks And Store Expansion Will Support Future Re Rating

Analysts have trimmed their average price target on Yum China by a small amount to around $62, citing slightly higher discount rate assumptions and only modest adjustments to long term revenue growth, profit margin, and future P/E expectations, even as recent research includes both target increases and decreases and a fresh addition to a major conviction list.

Analyst Commentary

Recent Street research on Yum China reflects a mix of optimism and caution, with several firms fine tuning their targets and ratings around execution, growth potential, and valuation.

Bullish Takeaways

- Bullish analysts highlight confidence in Yum China’s long term growth story, as shown by price target increases and the stock’s inclusion on a major APAC Conviction List, which points to conviction in the company’s ability to create value over time.

- The upgrade to a more positive rating suggests that some analysts see room for better execution, whether through store expansion, menu initiatives, or cost control, and expect these efforts to support earnings power.

- Target hikes are tied to the view that the current P/E can be supported by future cash flow generation, with bullish analysts comfortable that the company can justify, or potentially grow into, its valuation over time.

- The combination of target raises and a conviction list addition signals that, within the sector, Yum China is viewed by some as a relatively attractive way to gain exposure to the company’s existing footprint and brand portfolio.

Bearish Takeaways

- Bearish analysts who trimmed their price targets emphasize a more cautious stance on discount rate assumptions, which feeds directly into lower valuation estimates for Yum China.

- Some research reflects tempered expectations around long term revenue growth and profit margins, which, if not met, could make the current or prior P/E assumptions look demanding.

- The coexistence of both target increases and reductions shows that not all analysts are aligned on execution risk, with more cautious views focusing on whether Yum China can consistently deliver on its growth and margin ambitions.

- The modest cut to the average target underscores that even relatively small changes in key inputs, such as discount rates or margin expectations, can meaningfully affect perceived upside for the shares.

What's in the News

- Yum China completed a major share buyback tranche, repurchasing 9,752,000 shares for US$454.74 million between October 1, 2025 and December 31, 2025. This brought total repurchases under the program announced on February 7, 2017 to 98,919,696 shares, or 25.18%, for US$4,244.78 million (Key Developments).

- The company reported 1,706 net new stores in 2025, taking total store count to 18,101 as of December 31, 2025. Franchisees accounted for 31% of the net additions (Key Developments).

- Management communicated a target of more than 20,000 total stores and over 1,900 net new stores in 2026, indicating continued focus on expanding the physical footprint (Key Developments).

- For the fourth quarter ended December 31, 2025, Yum China reported store impairment charges of US$17 million, compared with US$20 million in the previous year period (Key Developments).

- The board approved a 21% increase in the annual cash dividend to US$0.29 per share for the year ended December 31, 2025. The dividend is payable on March 25, 2026 to shareholders of record on March 4, 2026, with an ex dividend date of March 3, 2026 (Key Developments).

Valuation Changes

- Fair Value: Trimmed slightly from $62.43 to $62.35, reflecting a very small adjustment to the model output.

- Discount Rate: Risen modestly from 9.25% to about 9.44%, implying a slightly higher required return in the updated analysis.

- Revenue Growth: Adjusted marginally from about 6.09% to about 6.08%, indicating a near flat change to long term top line growth assumptions.

- Net Profit Margin: Revised fractionally at about 8.52%, keeping earnings efficiency expectations broadly stable.

- Future P/E: Increased slightly from about 19.8x to about 19.9x, signaling a very small recalibration of the valuation multiple applied to future earnings.

Key Takeaways

- Aggressive expansion in lower-tier cities and digital ecosystem investments fuel revenue growth, enhance customer engagement, and boost operational efficiency.

- Innovation in menu offerings and improved supply chain efficiency support market share gains, higher profitability, and resilience against increasing competition.

- Escalating costs, intensifying competition, and shifting consumer preferences may constrain sales growth, compress margins, and challenge Yum China's ability to sustain long-term earnings expansion.

Catalysts

About Yum China Holdings- Owns, operates, and franchises restaurants in the People’s Republic of China.

- Continued aggressive expansion into lower-tier Chinese cities and new store formats (including KCOFFEE Cafes and Pizza Hut WOW), combined with healthy new store payback periods, supports ongoing top-line revenue growth and market share gains by tapping into rising urbanization and a broadening middle class.

- Deepening digital ecosystem investments (e.g., Super App, Mini programs, AI-driven end-to-end digitization, frontline innovation fund) enhance customer engagement, drive higher frequency of transactions, and improve operational efficiencies-positively impacting both revenues and net margins.

- Rapid growth of the delivery business, with delivery now 45% of total sales and all brands available on major platforms, expands the addressable market and supports sustainable same-store sales growth, mitigating competition by leveraging scale and cross-channel synergies.

- Ongoing innovation in menu offerings (e.g., KFC product launches, Pizza Hut's new pizzas, value-driven "All-You-Can-Eat" campaigns, and branded collaborations) enables Yum China to capture evolving consumer preferences for branded, safe, and experiential dining, driving incremental transactions and pricing power.

- Supply chain improvements, store automation, and lower CapEx per store (alongside a growing franchise store mix) drive down cost ratios and G&A expense, enabling sustainable margin expansion and higher operating profits even in the face of labor cost pressures.

Yum China Holdings Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

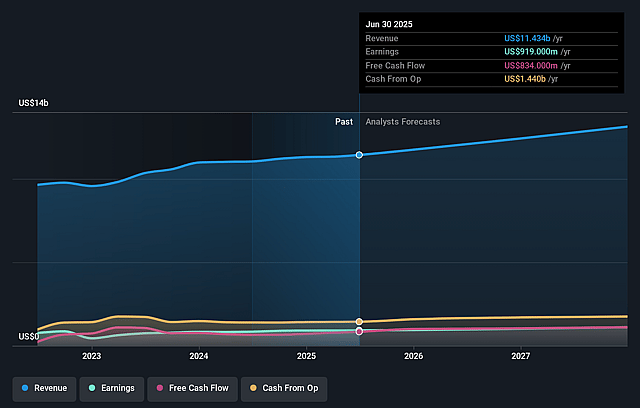

- Analysts are assuming Yum China Holdings's revenue will grow by 6.1% annually over the next 3 years.

- Analysts assume that profit margins will increase from 7.9% today to 8.5% in 3 years time.

- Analysts expect earnings to reach $1.2 billion (and earnings per share of $3.62) by about April 2029, up from $929.0 million today. However, there is some disagreement amongst the analysts with the more bullish ones expecting earnings as high as $1.3 billion.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 19.9x on those 2029 earnings, up from 17.8x today. This future PE is lower than the current PE for the US Hospitality industry at 21.0x.

- Analysts expect the number of shares outstanding to decline by 6.09% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.44%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Intensifying competition and aggressive discounting on delivery platforms, especially from digital-native and local Chinese QSR brands, could erode market share and limit Yum China's pricing power, resulting in downward pressure on same-store sales growth and net margins.

- The ongoing shift to a higher delivery mix, while expanding sales reach, is structurally increasing rider costs as a percentage of sales, which may compress restaurant margins and limit operating profit growth if labor cost inflation persists.

- Mix shift toward smaller-ticket orders (e.g., beverages, breakfast), and aggressive expansion into lower-tier cities with inherently lower ticket averages, may dilute average check size and restrain top-line revenue growth, even if transaction volumes increase.

- Reduced tailwind from commodity price declines, coupled with rising labor and delivery costs, may result in margin headwinds and create challenges in maintaining value-for-money offerings, limiting potential earnings expansion.

- Reliance on Western core brands (KFC, Pizza Hut) and slower testing or scaling of innovative formats (like Pizza Hut WOW) exposes the company to shifting consumer preferences towards healthier, more local, or niche QSR options, increasing the risk of stagnating same-store sales and impacting long-term revenue and profit stability.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $62.35 for Yum China Holdings based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $86.4, and the most bearish reporting a price target of just $53.1.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $14.1 billion, earnings will come to $1.2 billion, and it would be trading on a PE ratio of 19.9x, assuming you use a discount rate of 9.4%.

- Given the current share price of $47.99, the analyst price target of $62.35 is 23.0% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Yum China Holdings?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.