Last Update 23 Apr 26

LOW: Q4 Execution And FY26 Home Improvement Cycle Setup Will Support Upside

Analysts have adjusted the blended price target for Lowe's Companies modestly higher, within a range that now spans roughly the mid $250s to about $315, reflecting mixed reactions to Q4 results, FY26 guidance, and views on the home improvement and housing setup.

Analyst Commentary

Recent research paints a mixed picture, with many firms lifting price targets while a few trim expectations after Lowe's Q4 report and FY26 guidance. The updates cluster in a range from the mid US$250s to just above US$300, reflecting different views on how much to credit recent execution versus caution on the multi year outlook.

Bullish Takeaways

- Bullish analysts point to Q4 performance, including a Q4 earnings beat and what one firm called Lowe's strongest comparable sales growth in about four years, as evidence that execution is tracking well against prior expectations.

- Several firms that raised targets into the US$290 to US$305 range highlight consistent demand across regions, positive two year stacked comps, strength in big ticket categories and signs of early momentum in an industry recovery as support for higher valuation multiples.

- Research notes describe Lowe's as well positioned for long term earnings growth and potential market share gains, with cost discipline, disciplined P&L management and continued investment in future growth cited as key drivers.

- Some bullish analysts frame FY26 guidance as conservative or "a base to build off," arguing that near term margin pressure from acquisitions and distribution integration is manageable in the context of what they see as an improving home improvement cycle over time.

Bearish Takeaways

- Bearish analysts focus on FY26 guidance that is described as below expectations on margins and EPS, with some trimming price targets into the US$270 to US$293 range and maintaining more cautious ratings such as Hold or Sector Perform.

- Several firms flag concerns that 2026 expectations in the market may be drifting too high relative to management's guide, creating risk if sales or margins track closer to the lower end of current assumptions.

- One firm characterises guidance as disappointing even while calling it conservative, suggesting that upside may be more limited in the near term if home improvement demand and housing activity remain constrained.

- Bearish analysts that lowered targets cite slightly lower FY26 EPS estimates on revenue and margin tweaks and describe the post earnings selloff as a reaction to the longer dated software and fiscal 2026 outlook rather than the Q4 print itself.

What's in the News

- Lowe's plans to cut about 600 corporate and support roles, which the company says is less than 1% of its total workforce, and will offer career transition resources to affected employees (Wall Street Journal).

- The company introduced HomeCare+, a US$99 per year subscription for MyLowe's Rewards members that includes two in home visits annually and up to seven maintenance services per visit, such as HVAC filter replacement, electric dryer vent cleaning and smoke detector battery replacement, available across more than 75% of homes in the country.

- HomeCare+ subscribers receive 5% savings on select maintenance items, automatic Gold Status in MyLowe's Rewards with 1.5 points per US$1 on eligible purchases, fast and free delivery on qualifying orders, member only deals and access to member gifts, with gift cards for the service planned later in the year.

- Lowe's issued 2026 guidance that includes expected total sales of US$92.0b to US$94.0b, comparable sales flat to up 2%, operating margin of 11.2% to 11.4% and diluted EPS of about US$11.75 to US$12.25.

- Lowe's and Affirm announced a partnership that lets eligible customers split purchases into biweekly or monthly payments starting at 0% APR, with no compounding interest, late fees or hidden fees, and features Lowe's within the Affirm marketplace.

Valuation Changes

- Fair Value: holds steady at about $285.58, with no change from the prior estimate.

- Discount Rate: risen slightly from 9.04% to about 9.18%, implying a modestly higher required return in the model.

- Revenue Growth: edged up slightly from 5.24% to about 5.25%, a minimal adjustment to the long term sales growth assumption.

- Net Profit Margin: trimmed marginally from 8.07% to about 8.06%, reflecting a very small change in projected profitability.

- Future P/E: increased slightly from 25.47x to about 25.56x, a small upward shift in the valuation multiple applied to future earnings.

Key Takeaways

- Expansion into the Pro contractor market and integration of new digital capabilities position Lowe's for sustained growth, operational efficiency, and greater customer wallet share.

- Market consolidation and scale advantages are set to enhance supplier bargaining power and cost efficiencies, supporting long-term margin improvement.

- Major acquisitions, debt-related risks, tepid sales growth, labor pressures, and digital competition together threaten Lowe's operational margins, revenue growth, and long-term earnings potential.

Catalysts

About Lowe's Companies- Operates as a home improvement retailer in the United States.

- The acquisition of Foundation Building Materials (FBM) sharply accelerates Lowe's access to the large Pro contractor market-especially in key underserved regions (California, Northeast, Midwest)-unlocking new revenue streams, greater ticket sizes, and a larger share of the $250 billion Pro market, which is expected to drive above-market sales growth and improved diversification of revenue over the coming years.

- Ongoing pent-up demand from delayed home improvement projects, combined with record-high aging U.S. housing stock and an estimated 18 million new homes needed by 2033, points to a significant runway for future growth in renovation, repair, and new construction; this will positively affect revenue and support sustained top-line expansion as the housing cycle recovers.

- Continued investment in digital and omnichannel capabilities-including AI-powered tools for associates and new digital solutions brought through FBM's technology (e.g., MyFBM app, digital blueprint takeoff)-is expected to enhance operational efficiency, improve service levels for Pro and DIY customers, and drive incremental margin expansion through productivity gains.

- Cross-selling opportunities arising from the integration of FBM and ADG (flooring, cabinets, countertops) enable Lowe's to offer comprehensive interior solutions to large builders, boosting wallet share per customer and supporting margin and earnings growth through higher attachment rates and bundled sales.

- Market consolidation trends and Lowe's growing scale in both retail and distribution are poised to strengthen its bargaining power with suppliers, optimize procurement, and improve cost efficiencies, helping to defend and potentially expand both gross and operating margins over the long term.

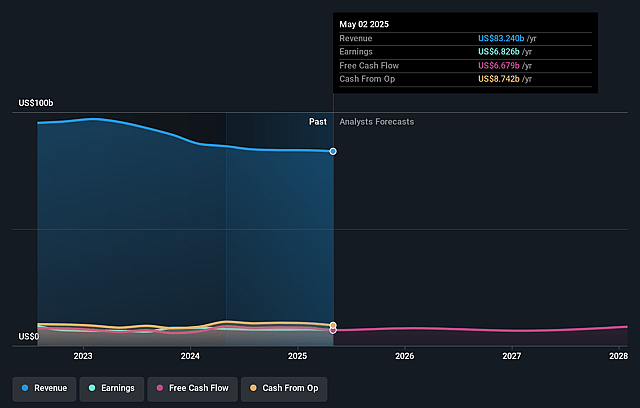

Lowe's Companies Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Lowe's Companies's revenue will grow by 5.3% annually over the next 3 years.

- Analysts assume that profit margins will increase from 7.7% today to 8.1% in 3 years time.

- Analysts expect earnings to reach $8.1 billion (and earnings per share of $14.7) by about April 2029, up from $6.6 billion today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $9.3 billion in earnings, and the most bearish expecting $7.3 billion.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 25.6x on those 2029 earnings, up from 20.7x today. This future PE is greater than the current PE for the US Specialty Retail industry at 20.8x.

- Analysts expect the number of shares outstanding to decline by 0.07% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.18%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The success of Lowe's major acquisitions (FBM and ADG) hinges on complex integration and execution; failure to effectively merge operations, technology, and cultures could lead to higher costs, operational disruptions, and lower-than-anticipated synergy realization, negatively affecting net margins and long-term earnings.

- The significant debt financing required for the $8.8 billion FBM acquisition will suspend share repurchases until 2027 and temporarily elevate leverage, increasing the company's exposure to interest rate changes and financial risk, which may weigh on earnings growth and shareholder returns.

- Flat to low single-digit comparable sales guidance and management's cautious commentary on a "flat home improvement market" signal that housing turnover and discretionary big-project demand remain suppressed by high mortgage rates and affordability concerns-potentially limiting revenue growth despite favorable secular trends.

- Persistent labor shortages and rising labor costs among both Pro customers and Lowe's workforce threaten to pressure operating margins and erode customer service advantages, possibly leading to margin compression and reduced earnings power long term.

- Ongoing market risk from digital disruption, large supplier bargaining power, and direct-to-consumer competition (including e-commerce channel rivalry and major brands bypassing retailers) may threaten Lowe's in-store and online sales growth, undermining both revenue expansion and margin improvement initiatives.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $285.58 for Lowe's Companies based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $325.0, and the most bearish reporting a price target of just $228.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $100.6 billion, earnings will come to $8.1 billion, and it would be trading on a PE ratio of 25.6x, assuming you use a discount rate of 9.2%.

- Given the current share price of $245.19, the analyst price target of $285.58 is 14.1% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Lowe's Companies?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.