Last Update 25 Jun 26

NVMI: Advanced Packaging And Hybrid Bonding Momentum Will Shape Future Cash Generation

Analysts have raised their average price target on Nova to about $598, a move toward the recent $600+ targets from several firms that is supported by strong Q1 execution, higher expectations around advanced DRAM and logic investments, and faster than expected traction in hybrid bonding and advanced packaging.

Analyst Commentary

Recent research on Nova highlights a clear skew toward higher valuation frameworks after the Q1 report, with several firms lifting price targets into the high US$500s and low US$600s. The commentary centers on execution in the March quarter, expectations tied to advanced DRAM and logic spending, and the pace of adoption in hybrid bonding and advanced packaging.

Bullish Takeaways

- Bullish analysts point to Q1 results that came in ahead of prior Street expectations on sales and pro-forma EPS, which supports a higher valuation framework for Nova.

- Several price targets have been raised into a US$595 to US$640 range, reflecting confidence in Nova's exposure to advanced DRAM, logic and memory investments, as well as customer capacity expansion at large chip manufacturers.

- Commentary highlights faster than expected traction in hybrid bonding and advanced packaging, which bullish analysts view as important incremental growth drivers on top of the core business.

- Some bulls argue that a premium earnings multiple is justified, citing Nova's margin profile, execution in the March quarter and leverage to advanced logic and packaging trends.

Bearish Takeaways

- More cautious analysts acknowledge solid March quarter execution but question whether a 40x+ earnings multiple is sustainable given that their forecast growth rate is not meaningfully higher than peers.

- There is concern that, even with support from packaging revenue and advanced DRAM and logic exposure, the current valuation may already discount much of the expected growth.

- Some cautious views emphasize that while Nova offers "a lot to like," the risk reward looks less compelling if the growth profile does not clearly stand out versus other semiconductor equipment stocks.

What’s in the News for Nova

- Nova is featured as a strong momentum stock in the semiconductor manufacturing quality control sector, with the article citing lasting competitive advantages, higher annual revenue, and operating margins compared with peers, as well as market share gains and faster earnings growth over the last five years, according to a recent stock commentary piece. (Source: "1 Momentum Stock Worth Your Attention and 2 Facing Challenges")

- A recent investor letter from Wasatch Global Investors highlights Nova as one of the largest contributors to returns in its Small Cap Growth Strategy for Q1 2026, with the fund pointing to AI driven semiconductor demand as a key factor supporting the stock’s recent performance. (Source: Wasatch Global Investors Small Cap Growth Strategy Q1 2026 letter, "Nova Ltd. (NVMI) Gained from AI-Driven Momentum")

- Nova reported record Q1 results, with revenue of US$235.3 million, a 10.3% year over year increase and 3.5% above analyst expectations, alongside operating income that came in ahead of estimates and an improvement in inventory levels, which the CEO described as a record quarter across every dimension. (Source: "Nova Reports Record Q1 Results with Revenues Surpassing Expectations")

- Following the Q1 earnings release, Nova’s stock price moved sharply higher, reflecting the market reaction to the revenue and operating income outperformance and commentary from management on the quarter. (Source: "Nova Reports Record Q1 Results with Revenues Surpassing Expectations")

- Nova issued guidance for Q2 2026, projecting revenue between US$245 million and US$255 million and diluted GAAP EPS between US$2.10 and US$2.24, providing investors with a benchmark for the upcoming quarter. (Source: Company guidance filing)

Valuation Changes for Nova

- Fair Value: The model fair value estimate remains unchanged at $597.63, with no adjustment in the latest update.

- Discount Rate: The discount rate has fallen slightly from 14.51% to 14.50%, indicating a very small adjustment to the required return assumption.

- Revenue Growth: Revenue growth is held steady at 18.53%, with no change between the prior and updated assumptions.

- Net Profit Margin: The net profit margin is effectively unchanged at 32.63%, reflecting consistent profitability expectations for Nova.

- Future P/E: The future P/E is marginally lower, moving from 69.52x to 69.51x, a very small shift that keeps the valuation multiple largely intact.

Key Takeaways

- Demand for Nova's advanced metrology and analytics solutions is rising due to semiconductor complexity and global industry investments, supporting broad, diversified growth.

- Product innovation and recurring, high-margin services are strengthening customer relationships and margins, positioning Nova for increased market share and operational leverage.

- Heavy reliance on key customers, technology adoption risks, higher R&D spending, geopolitical exposure, and rising competition all cloud Nova's revenue and margin outlook.

Catalysts

About Nova- Engages in the design, development, production, and sells of process control systems used in the manufacture of semiconductors in Taiwan, the United States, China, Korea, and internationally.

- The accelerating complexity of semiconductor devices-driven by AI, larger die sizes, advanced nodes, and heterogeneous packaging-continues to fuel demand for Nova's advanced metrology solutions across both logic/foundry and memory segments, which is poised to lift long-term revenue growth as global digitization trends expand.

- Ongoing global investments in semiconductor manufacturing capacity (including reshoring, new fabs in multiple regions, and government incentives) are broadening Nova's customer base and diversifying revenue streams, supporting sustained top-line growth and reducing reliance on any single geography or customer.

- Expansion of Nova's software-driven analytics, AI/ML integration, and value-added services is deepening customer relationships and driving a recurring revenue mix with higher margins, which is likely to support stable or improving net margins over time.

- Introduction and ramp of new product platforms (e.g., Sentronics integration, VeraFlex, METRION, and ELIPSON tools) for advanced logic, memory, and 3D NAND applications positions Nova to capture additional market share and opens new cross-selling opportunities, further boosting future revenue trajectories.

- Operational excellence achieved through diversified revenue streams, a resilient business model, and continued efficiency investments positions Nova to leverage scale and expand operating margins as their solutions proliferate through industry inflection points.

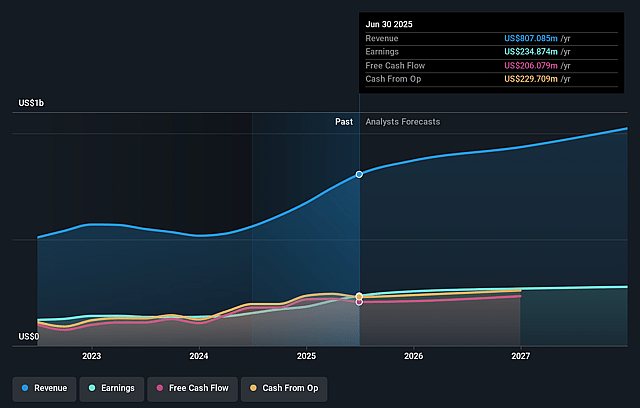

Nova Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Nova's revenue will grow by 18.5% annually over the next 3 years.

- Analysts assume that profit margins will increase from 29.2% today to 32.6% in 3 years time.

- Analysts expect earnings to reach $490.5 million (and earnings per share of $13.06) by about June 2029, up from $263.7 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 71.2x on those 2029 earnings, up from 64.4x today. This future PE is greater than the current PE for the US Semiconductor industry at 70.5x.

- Analysts expect the number of shares outstanding to grow by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 14.5%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Nova's significant exposure to a few major "gate-all-around" and advanced node customers increases concentration risk-if any large customer reduces or delays CapEx, as hinted at for one IDM customer, it could result in uneven revenue growth and threaten earnings stability over time.

- The company's ongoing growth depends on successful adoption and commercialization of new technologies like ELIPSON, METRION, and advanced material metrology platforms; failure to reach "process tool of record" status or slower-than-expected lab-to-fab conversion could stall product diversification and limit future top-line expansion.

- Heightened investments in R&D and integration of new acquisitions (e.g., Sentronics), while necessary for innovation, may pressure net margins if commercialization cycles are longer than planned or if revenue synergy assumptions are not fully realized.

- Nova cites increasing strength in advanced packaging and China, but given potential future shifts in trade restrictions, tariffs, or geopolitical tensions, its global revenue diversification remains vulnerable to external shocks that could negatively impact both revenue and margin profiles.

- The market's current optimism about Nova's competitive leadership in several segments could be undermined by intensified competition in integrated and stand-alone metrology, especially if larger or emerging players launch new products or price aggressively, potentially eroding Nova's gross margins and long-term earnings power.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $597.62 for Nova based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $640.0, and the most bearish reporting a price target of just $494.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $1.5 billion, earnings will come to $490.5 million, and it would be trading on a PE ratio of 71.2x, assuming you use a discount rate of 14.5%.

- Given the current share price of $534.24, the analyst price target of $597.62 is 10.6% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Nova?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.