Catalysts

About Clean Energy Fuels

Clean Energy Fuels develops, produces and supplies renewable natural gas and related fueling infrastructure for transportation fleets.

What are the underlying business or industry changes driving this perspective?

- Although heavy-duty fleets are increasingly focused on cost-effective decarbonization and the X15N platform offers a viable solution today, ongoing freight rate weakness and deferred truck replacement could slow equipment turnover and temper the pace of RNG volume growth, limiting upside to revenue expansion.

- Despite regulatory frameworks that favor low carbon intensity fuels and support long haul decarbonization, prolonged uncertainty around future emissions rules and incentive structures may delay large fleet commitments to RNG, constraining scale benefits and the margin leverage the company can achieve on its fueling network.

- While the build-out of dairy RNG projects positions the company to control more negative carbon supply over the next several years, operational ramp-up risks and the need for continued fine tuning at new plants could keep production below nameplate longer than anticipated, weighing on upstream earnings and depressing consolidated EBITDA.

- Although programs like LCFS and the clean fuel production credit are expected to strengthen the economics of low carbon fuels over time, slower than expected credit price recovery or less favorable 45Z implementation would limit improvement in realized environmental attribute values, putting pressure on net margins from the RNG production segment.

- While broader transportation markets are steadily shifting away from diesel toward cleaner alternatives, intensifying competition from other low carbon solutions and ample third-party RNG supply may cap pricing power at fueling stations, moderating fuel margin expansion and constraining long-term earnings growth.

Assumptions

This narrative explores a more pessimistic perspective on Clean Energy Fuels compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts. How have these above catalysts been quantified?

- The bearish analysts are assuming Clean Energy Fuels's revenue will remain fairly flat over the next 3 years.

- The bearish analysts are not forecasting that Clean Energy Fuels will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate Clean Energy Fuels's profit margin will increase from -49.6% to the average US Oil and Gas industry of 14.2% in 3 years.

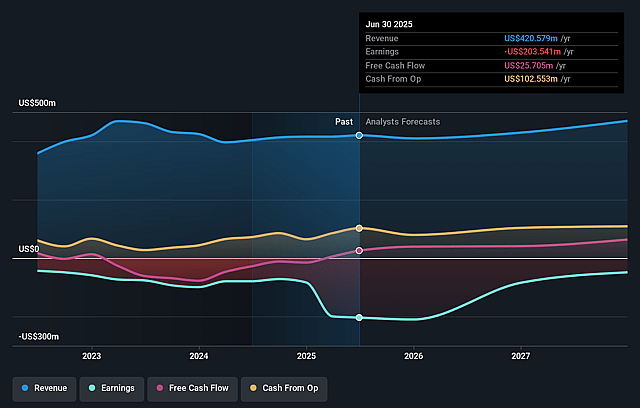

- If Clean Energy Fuels's profit margin were to converge on the industry average, you could expect earnings to reach $61.1 million (and earnings per share of $0.3) by about December 2028, up from $-209.2 million today.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 9.2x on those 2028 earnings, up from -2.4x today. This future PE is lower than the current PE for the US Oil and Gas industry at 13.2x.

- The bearish analysts expect the number of shares outstanding to decline by 1.92% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.43%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?

- If LCFS credit prices and other environmental attribute values recover faster and stronger than management currently assumes, CARB program changes and potential 45Z implementation could materially enhance the economics of dairy RNG and accelerate upstream project returns, driving higher revenue and improved net margins.

- As newly commissioned dairy RNG plants ramp from partial output toward nameplate and additional Maas Energy projects come online through 2026 and 2027, Clean Energy could shift from modest to substantial owned negative carbon supply, lifting consolidated earnings as volume scales across a largely fixed-cost infrastructure base.

- Should freight markets and heavy-duty truck replacement cycles normalize sooner than expected, combined with growing shipper pressure to decarbonize, adoption of the Cummins X15N platform and low carbon leasing solutions like Pioneer Clean Fleet could inflect, materially increasing RNG fuel sales volumes, revenue and downstream EBITDA.

- If electric and hydrogen truck alternatives continue to face cost and infrastructure constraints while RNG maintains a clear cost per mile and emissions advantage, Clean Energy's extensive fueling network and customer base could translate into durable pricing power and higher fuel margins that support sustained growth in earnings.

- With over $232 million in cash, access to capital for additional RNG projects and a large pipeline of contracted customers, effective execution on project optimization and disciplined expansion could produce operating leverage that drives meaningful upside in adjusted EBITDA and accelerates the path toward GAAP profitability.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bearish price target for Clean Energy Fuels is $2.2, which represents up to two standard deviations below the consensus price target of $4.71. This valuation is based on what can be assumed as the expectations of Clean Energy Fuels's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $10.0, and the most bearish reporting a price target of just $2.2.

- In order for you to agree with the more bearish analyst cohort, you'd need to believe that by 2028, revenues will be $429.2 million, earnings will come to $61.1 million, and it would be trading on a PE ratio of 9.2x, assuming you use a discount rate of 7.4%.

- Given the current share price of $2.27, the analyst price target of $2.2 is 3.2% lower. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Clean Energy Fuels?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.