Key Takeaways

- GDS Holdings' positioning in Tier 1 markets and flexibility in customer deployment aid in managing resources and enhancing financial stability.

- Strategic order wins and deconsolidation actions support growth and improve future revenue prospects and financial value creation.

- Dependence on AI demand in top markets, strategic uncertainty, financial unreliability, and high debt pose risks to revenue growth and net margins.

Catalysts

About GDS Holdings- Develops and operates data centers in the People's Republic of China.

- GDS Holdings is well-positioned in Tier 1 markets, with significant available land and power to meet the increasing demand for AI inferencing from the largest cloud and Internet companies in China, which could drive future revenue growth.

- The strategic focus on flexibility in customer deployment timing, combined with strong asset monetization capabilities, enables GDS to manage financial resources effectively, potentially improving net margins and financial stability.

- The company's high-volume new order wins, such as the 152-megawatt order from a major hyperscale customer, suggest strong future revenue prospects and efficient capital expenditure management, positively impacting earnings.

- GDS's strategic decision to wait and observe the chip supply situation allows it to remain agile and adapt to market conditions, which can lead to better capital allocation and improved net margins.

- The successful deconsolidation of DayOne to become an equity investee provides potential for future financial value creation, supporting growth in earnings as DayOne continues to commit to large-scale projects and expands its sales pipeline.

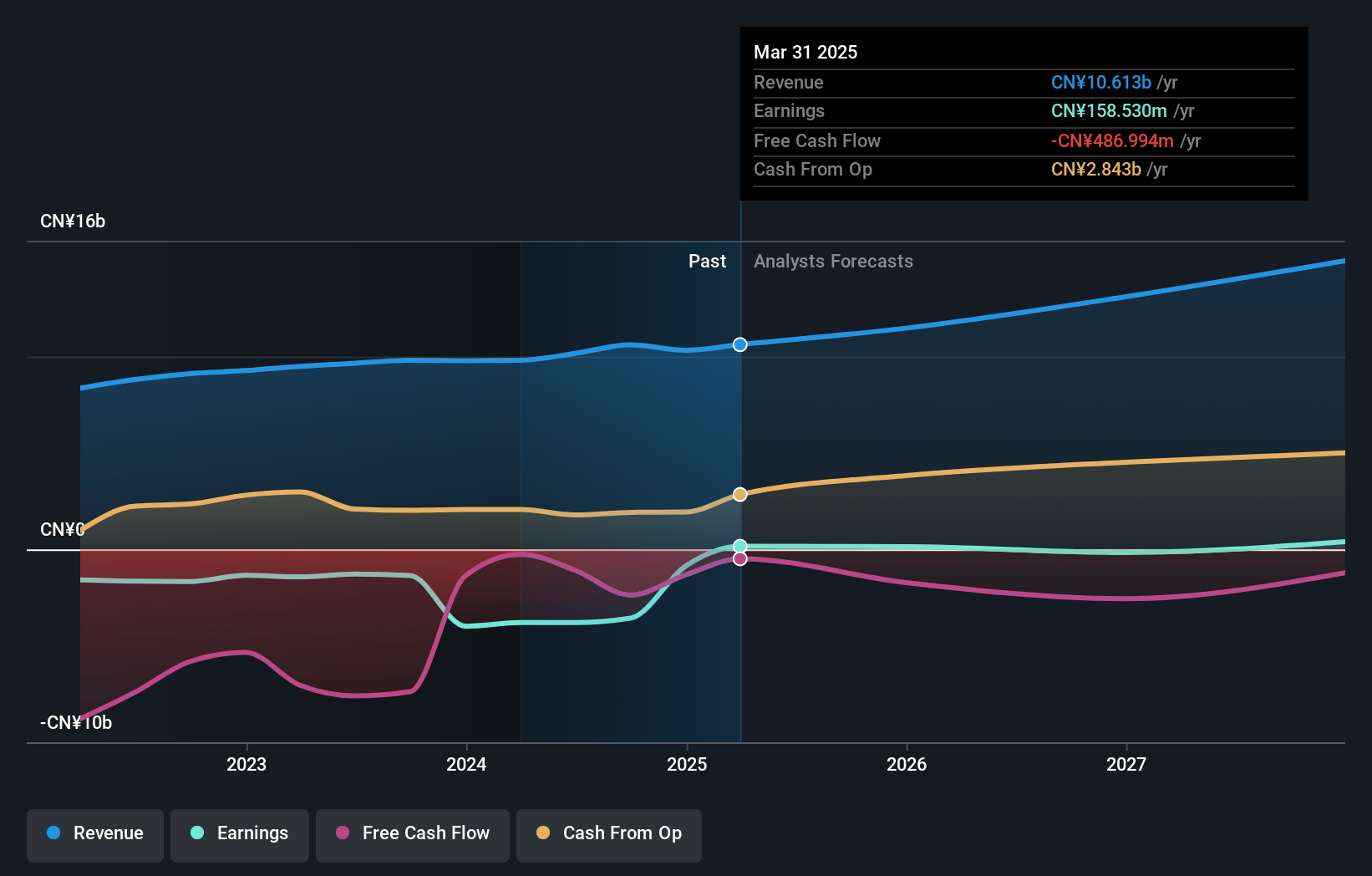

GDS Holdings Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming GDS Holdings's revenue will grow by 13.2% annually over the next 3 years.

- Analysts assume that profit margins will increase from -8.1% today to 2.6% in 3 years time.

- Analysts expect earnings to reach CN¥385.1 million (and earnings per share of CN¥1.44) by about April 2028, up from CN¥-831.4 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting CN¥1.0 billion in earnings, and the most bearish expecting CN¥-569.3 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 241.3x on those 2028 earnings, up from -38.3x today. This future PE is greater than the current PE for the US IT industry at 32.6x.

- Analysts expect the number of shares outstanding to grow by 0.96% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 13.29%, as per the Simply Wall St company report.

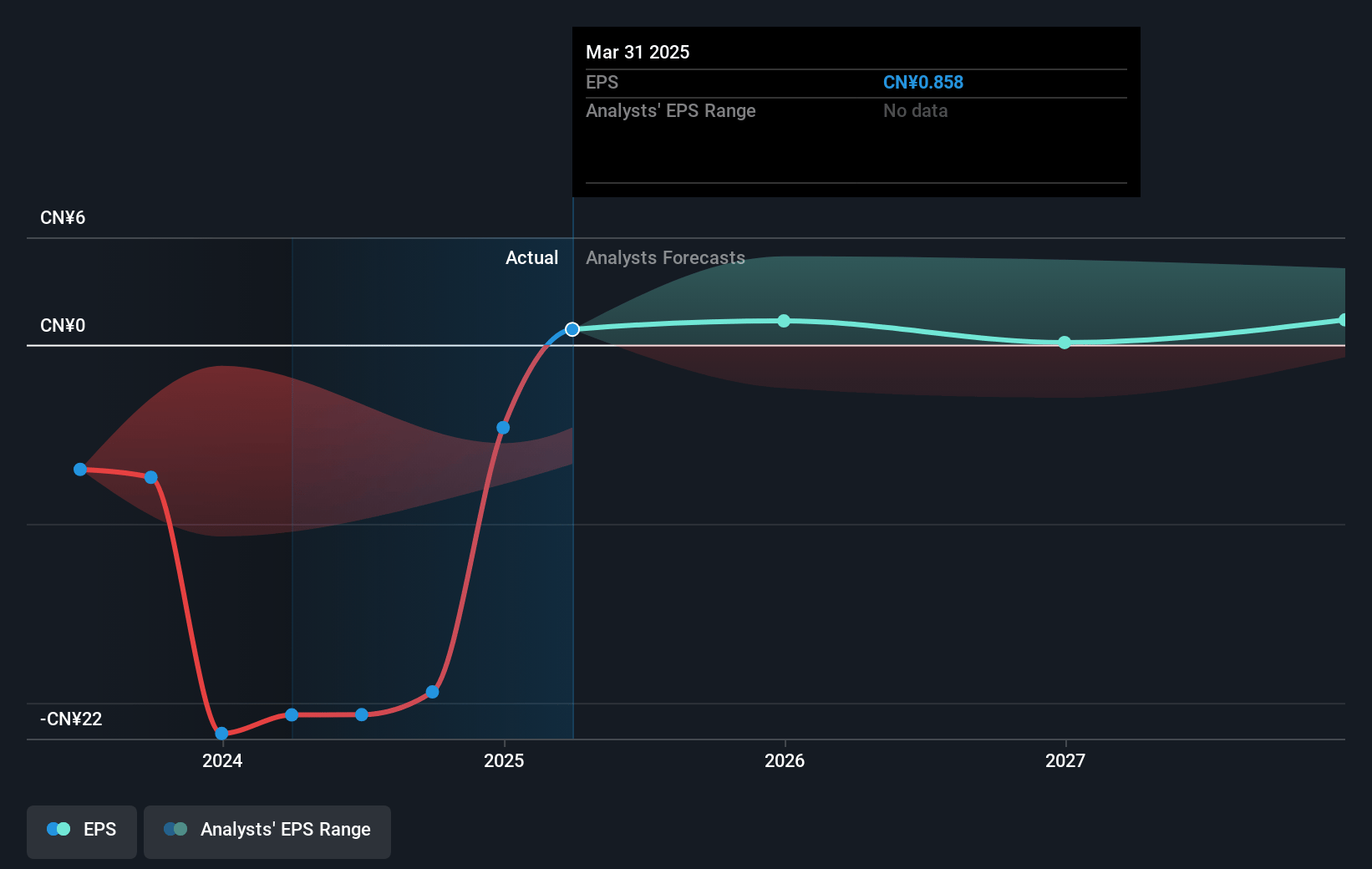

GDS Holdings Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- GDS Holdings' success is heavily reliant on the demand for AI inferencing in Tier 1 markets. Any delay in chip availability could hinder future customer deployments, impacting revenue growth.

- The company's strategy includes waiting and seeing for future deployments, which indicates uncertainty in future market conditions and could limit immediate revenue opportunities and result in missed growth.

- Deconsolidation of DayOne and its reclassification as an equity investee reduces the contribution to GDS's financials from DayOne's quickly growing demand, potentially affecting net income visibility.

- Current financial projections do not account for the balance of proceeds from future asset monetization transactions, which could lead to variability in cash flow and dependence on external factors for free cash flow stability.

- The high net debt to last quarter annualized adjusted EBITDA multiple, though expected to decline, remains a risk if there's an economic slowdown or increased interest rates that could impact net margins and earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $43.706 for GDS Holdings based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $62.91, and the most bearish reporting a price target of just $28.96.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be CN¥15.0 billion, earnings will come to CN¥385.1 million, and it would be trading on a PE ratio of 241.3x, assuming you use a discount rate of 13.3%.

- Given the current share price of $22.4, the analyst price target of $43.71 is 48.7% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.