Last Update 17 Jun 26

APEI: Military Segment And Health Recovery Will Support 2026 Reacceleration

Analysts have maintained their $62.17 price target on American Public Education, citing recent Q1 upside, stable Military+ performance, and an ongoing recovery in Rasmussen and Health+ as key supports for their view.

Analyst Commentary

Recent research on American Public Education highlights a generally upbeat stance on the stock, centered on execution in core segments and the implications for margins, earnings quality, and valuation support.

Bullish Takeaways

- Bullish analysts see the inclusion of American Public Education in select lists of high quality companies as a signal of confidence in its business model, competitive moat, and risk‑reward profile at current valuation levels.

- Multiple upward price target revisions, clustered around the low to mid US$60 range, are tied to Q1 results that topped expectations on both revenue and earnings, which analysts view as support for their existing models.

- Commentary points to steady, profitable performance in the Military+ and APUS segments and a recovery in Health+ and Rasmussen as key execution drivers that, if sustained, could support margin stability and potential expansion.

- Analysts highlight registration strength in Army and Vets/Families cohorts as evidence of brand strength, which they see as important for maintaining enrollment momentum and supporting longer term growth assumptions embedded in their targets.

Bearish Takeaways

- Some analysts flag the impact of Middle East conflict on a portion of active duty students as a headwind, which introduces uncertainty around near term enrollment and revenue contribution from that group.

- Price targets, while higher than before in several cases, still imply that American Public Education needs to deliver on continued operational recovery and margin execution, which may be challenging if external disruptions persist.

- Reliance on ongoing improvement at Rasmussen and Health+ is a key pillar in bullish models, and any stall in that recovery could pressure both earnings trajectories and the valuation frameworks supporting current analyst targets.

What’s in the News for American Public Education

- American Public Education is actively seeking tuck in acquisitions, with management highlighting interest in new campuses and licensed states that show a supply demand imbalance in health care education, source: APEI Q1 2026 earnings call.

- Leadership indicated that the company is considering both single campus and multi campus targets that fit broader criteria such as geographic adjacency and licensing, source: APEI Q1 2026 earnings call.

- American Public Education issued full year 2026 guidance, with expected consolidated revenue of US$686 million to US$696 million, net income available to common stockholders of US$44.9 million to US$51.6 million, and diluted EPS of US$2.33 to US$2.68 per share, source: company guidance.

- The company provided guidance for Q2 2026, expecting consolidated revenue of US$170.0 million to US$172.0 million, net income available to common stockholders of US$6.5 million to US$7.5 million, and diluted EPS of US$0.34 to US$0.39 per share, source: company guidance.

Valuation Changes for American Public Education Stock

- Fair Value: The modeled fair value remains unchanged at $62.17 per share, indicating no adjustment to the central valuation point.

- Discount Rate: The discount rate has risen slightly from 7.29% to 7.43%, reflecting a modestly higher required return on American Public Education.

- Revenue Growth: The long term revenue growth assumption is essentially unchanged at 7.52%.

- Net Profit Margin: The projected net profit margin remains effectively stable at 8.49%, with only a minimal numerical adjustment.

- Future P/E: The assumed future P/E multiple has risen slightly from 20.97x to 21.05x, implying a marginally higher earnings multiple in the updated model.

Key Takeaways

- Consolidating educational brands and expanding career-oriented healthcare offerings drive operational efficiencies and align with rising demand for upskilling among adult learners.

- Enhanced online capabilities and strong military partnerships boost student retention, recurring revenue, and sustain revenue stability through affordable, outcome-focused programs.

- Integration challenges, reliance on federal funding, regulatory uncertainty, and competition from alternative education models threaten profitability and margin growth despite enrollment gains.

Catalysts

About American Public Education- Provides online and campus-based postsecondary education and career learning in the United States.

- Ongoing double-digit enrollment growth at Rasmussen University and Hondros College of Nursing, combined with operating leverage as these units scale, positions APEI to benefit from increased demand for career-oriented healthcare education-likely supporting future revenue growth and margin expansion.

- Strategic consolidation of APUS, Rasmussen, and Hondros into a single accredited institution will unlock cost and revenue synergies, including shared curriculum access and more efficient marketing across a unified brand platform, potentially accelerating top-line growth and improving net margins.

- Expansion in online learning and remote education, reinforced by investments in intelligent infrastructure, predictive analytics, and personalized digital tools, strengthens student engagement and retention-expected to drive higher recurring revenues and improved profitability over time.

- Elevated government support for military education (e.g., $100M extension in tuition assistance through the Department of Defense) and APEI's strong relationships with military institutions enhance visibility of future enrollment and reduce student acquisition costs, contributing to sustained revenue stability and higher gross margins.

- APEI's focus on affordable, outcome-based educational offerings in high-demand fields (especially nursing) aligns with rising demand for upskilling and reskilling among adult learners, supporting a stable, growing customer base and underpinning long-term revenue and earnings growth.

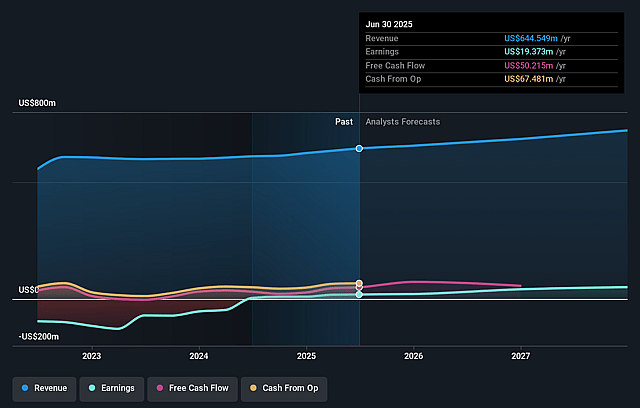

American Public Education Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming American Public Education's revenue will grow by 7.5% annually over the next 3 years.

- Analysts assume that profit margins will increase from 5.4% today to 8.5% in 3 years time.

- Analysts expect earnings to reach $69.6 million (and earnings per share of $3.09) by about June 2029, up from $35.6 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 21.3x on those 2029 earnings, down from 26.8x today. This future PE is greater than the current PE for the US Consumer Services industry at 16.1x.

- Analysts expect the number of shares outstanding to grow by 1.53% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.43%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Ongoing integration of APUS, Rasmussen, and Hondros into a single accredited institution presents execution and consolidation risks-delays, unexpected costs, or difficulty realizing anticipated synergies could negatively affect expenses and profitability.

- Despite enrollment growth, Rasmussen and Hondros are operating at or near breakeven levels, and profitability relies heavily on continued enrollment momentum-any slowdown could compress margins and restrain earnings growth.

- The company's strong reliance on federal military tuition assistance and related policies exposes revenue and profitability to future legislative, regulatory, or budgetary changes, despite recent funding increases.

- The sector remains vulnerable to increased regulatory scrutiny, accountability standards, and potential changes in gainful employment or loan caps that, even if currently manageable, could increase compliance costs or reduce available funding, pressuring margins and enrollments.

- American Public Education's strategy of focusing on affordable, high-demand programs requires ongoing marketing efficiency and technological investment; escalating competition from alternative credential providers or new education models could erode market share and force tuition reductions, negatively impacting revenues and net margins.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $62.17 for American Public Education based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $68.0, and the most bearish reporting a price target of just $55.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $819.2 million, earnings will come to $69.6 million, and it would be trading on a PE ratio of 21.3x, assuming you use a discount rate of 7.4%.

- Given the current share price of $51.89, the analyst price target of $62.17 is 16.5% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on American Public Education?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.