Last Update 02 Jun 26

Fair value Increased 3.69%BMPS: Leadership Transition And Bullish Coverage Will Drive Future Upside Potential

Analysts have raised their price target for Banca Monte dei Paschi di Siena to about €10.63 from approximately €10.25, citing updated assumptions on growth, margins and valuation following recent bullish research coverage.

What's in the News

- The board removed Chief Executive Luigi Lovaglio's executive powers and the role of general manager after a disagreement over his strategy for recently acquired peer Mediobanca, according to key developments data.

- Deputy General Manager Maurizio Bai was appointed to oversee the ordinary running of the bank until 15 April, based on the same disclosure.

- The board urged Lovaglio to resign, according to people cited in the key developments summary, but he remains on the board as a director until the next general meeting.

- The board plans to propose Fabrizio Palermo, currently CEO of Roman utility ACEA, as the sole CEO candidate for Banca Monte dei Paschi di Siena, replacing an earlier plan to present three potential candidates, as reported in the key developments data.

Valuation Changes

- Fair Value has been updated to €10.63 from €10.25 and has risen slightly based on the revised assumptions.

- The Discount Rate has been reduced to 12.81% from 14.06% and has fallen moderately, affecting how future cash flows are assessed.

- Revenue Growth has been reset to 23.03% from 31.70% and has fallen meaningfully in the updated model.

- Net Profit Margin has been adjusted to 36.24% from 35.89% and has risen slightly in the latest assumptions.

- Future P/E has been updated to 17.78x from 17.93x and has edged slightly lower in the revised valuation work.

Key Takeaways

- Declining interest rates, demographic challenges, and digital disruption threaten future profitability, loan growth, and revenue sustainability.

- Reliance on merger synergies and digital transformation is crucial, but scale disadvantages and rising costs may constrain long-term earnings improvement.

- Improved asset quality, capital strength, and expansion initiatives position the bank for enhanced profitability, strategic growth, and stronger shareholder returns amid ongoing sector consolidation.

Catalysts

About Banca Monte dei Paschi di Siena- Engages in the provision of retail and commercial banking services in Italy.

- The bank's recent strong profit growth and improved asset quality appear to reflect favorable Italian economic conditions, but with interest rates expected to decline and structural macro headwinds like Italy's aging population persisting, credit demand and loan growth could slow longer-term, compressing revenues and ultimately earnings.

- Current robust net interest income benefits from strong lending volumes and retail deposit growth, but the anticipated environment of declining rates in the EU threatens net interest margins and makes it difficult to maintain the current level of profitability, likely leading to margin pressure ahead.

- While the high current profitability and strong capital position underpin a raised guidance and the prospect of a 100% payout dividend policy, intensifying competition from fintechs and rapid digitalization may erode traditional fee and lending revenues, weakening future revenue growth.

- The bank's optimistic forward guidance hinges heavily on merger synergies with Mediobanca, but if industry consolidation trends accelerate, BMPS risks competitive disadvantage or value-dilutive terms if unable to achieve scale, which could hamper cost synergies and constrain earnings growth.

- Long-term structural pressures-including regulatory tightening, higher capital requirements, and persistent scale disadvantages versus larger EU peers-threaten to drive up operating costs and maintain elevated cost-to-income ratios, limiting sustainable improvement in net margins and overall earnings.

Banca Monte dei Paschi di Siena Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

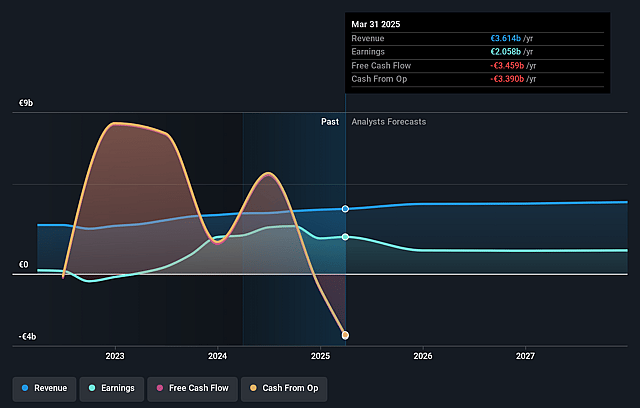

- Analysts are assuming Banca Monte dei Paschi di Siena's revenue will grow by 23.0% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 59.6% today to 36.2% in 3 years time.

- Analysts expect earnings to reach €3.2 billion (and earnings per share of €1.0) by about June 2029, up from €2.8 billion today. However, there is some disagreement amongst the analysts with the more bullish ones expecting earnings as high as €3.5 billion.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 17.8x on those 2029 earnings, up from 9.8x today. This future PE is greater than the current PE for the IT Banks industry at 10.0x.

- Analysts expect the number of shares outstanding to grow by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 12.81%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Sustained improvements in asset quality, evidenced by consistent reductions in non-performing loan (NPL) stock and a declining cost of risk, could enhance net margins and reduce future credit losses, positively impacting profitability and earnings.

- The robust capital position (CET1 ratio of 19.6%) and strong results in stress tests provide a significant buffer above regulatory requirements, enabling strategic flexibility for further growth, M&A, and increased shareholder payouts, which could support or boost the share price.

- The proposed combination with Mediobanca is projected to deliver substantial pre-tax synergies (~€700 million per year) and double-digit accretion in adjusted earnings per share, as well as a 100% payout ratio and high dividend yield, directly benefiting shareholder returns and future earnings growth.

- Ongoing expansion in wealth management, commercial banking, and consumer lending-demonstrated by strong inflows, increased lending volumes, and rising fee income-reflects effective digital transformation and commercial execution, which may drive revenue growth and operational efficiency long-term.

- Progressive financial sector consolidation in Europe could unlock cross-border synergies, improved scale, and competitive positioning for the combined entity, positioning Banca Monte dei Paschi di Siena to capture new revenue streams, enhance net margins, and improve cost-to-income ratios over time.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of €10.63 for Banca Monte dei Paschi di Siena based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of €12.0, and the most bearish reporting a price target of just €9.2.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be €8.8 billion, earnings will come to €3.2 billion, and it would be trading on a PE ratio of 17.8x, assuming you use a discount rate of 12.8%.

- Given the current share price of €9.09, the analyst price target of €10.63 is 14.5% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Banca Monte dei Paschi di Siena?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.