Last Update 25 Jun 26

FRACTL: Stable Margins And P/E Assumptions Will Support Future Upside Potential

Analysts have kept their SEK price target for Fractal Gaming Group effectively unchanged at about SEK21.33, reflecting only minor tweaks to the discount rate, revenue growth, profit margin and future P/E assumptions in their updated models.

What’s in the News for Fractal Gaming Group

- No recent company specific news items for Fractal Gaming Group were identified in the provided sources as of 24 Jun 2026.

- The absence of listed periodical coverage in the supplied data means there are no referenced third party articles to highlight for Fractal Gaming Group.

- No key developments were reported in the provided feeds, so recent corporate actions or announcements for Fractal Gaming Group are not captured here.

Valuation Changes for Fractal Gaming Group

- Fair Value: Estimated fair value remains unchanged at SEK21.33 per share. This indicates no revision to the central valuation outcome in the latest update.

- Discount Rate: The discount rate has risen slightly from 6.69% to about 6.75%, which marginally adjusts how Fractal Gaming Group’s future cash flows are weighted in the model.

- Revenue Growth: The assumed long term revenue growth rate has eased slightly from about 61.72% to about 60.51%. This reflects a small recalibration of top line expectations in SEK terms.

- Net Profit Margin: The modeled net profit margin is effectively stable, shifting only marginally from about 8.69% to about 8.69%. This keeps Fractal Gaming Group’s earnings profile largely consistent.

- Future P/E: The future P/E assumption edges up modestly from approximately 11.54x to 11.56x. This is a very small adjustment to how projected earnings are translated into an equity valuation.

Key Takeaways

- Expansion into new regions and premium product focus positions the brand for sustained growth and higher margins.

- Supply chain adjustments and direct sales channel growth aim to counter external margin pressures and support profitability.

- Overdependence on the shrinking DIY PC case market, weak diversification efforts, and external cost pressures threaten future revenue growth and profitability.

Catalysts

About Fractal Gaming Group- Offers PC gaming products in Sweden an internationally.

- The continued global expansion, especially in North America and APAC, provides a long-term growth runway as Fractal Gaming successfully increases market share and broadens its customer base, supporting future revenue growth.

- Rising consumer preference for premium, design-led and ergonomic gaming setups favors Fractal's innovation in modular and customizable products, positioning the brand to capitalize on increased demand for high-quality, aesthetic hardware and enabling revenue premiumization and higher gross margins.

- Ongoing adoption of new hardware (e.g., GPUs) and the robust upgrade cycle in the global gaming and esports community are expected to sustain elevated demand for Fractal's high-end cases and peripherals, fueling top-line growth beyond the latest product launch cycles.

- Strengthening direct-to-consumer and e-commerce channels, along with reduced reliance on intermediaries, is likely to improve operational leverage and increase net margins over time.

- Margin headwinds from tariffs, freight, and currency are being actively mitigated through price increases and strategic supply chain relocation, which are expected to deliver margin recovery and bolster earnings in the coming quarters.

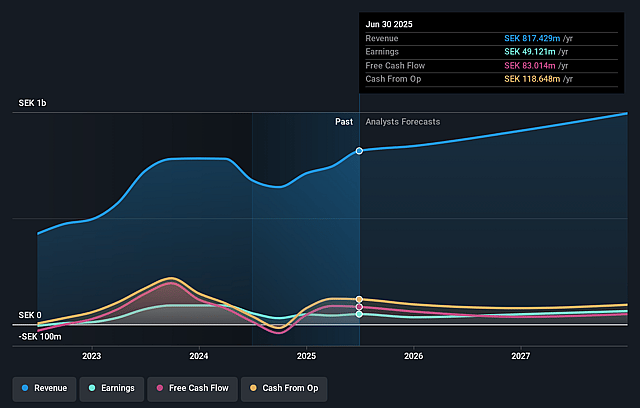

Fractal Gaming Group Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Fractal Gaming Group's revenue will remain fairly flat over the next 3 years.

- Analysts assume that profit margins will increase from 1.1% today to 8.7% in 3 years time.

- Analysts expect earnings to reach SEK 65.1 million (and earnings per share of SEK 1.6) by about June 2029, up from SEK 7.8 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting SEK92.9 million in earnings, and the most bearish expecting SEK23.3 million.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 11.6x on those 2029 earnings, down from 52.1x today. This future PE is lower than the current PE for the SE Tech industry at 44.3x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.75%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Heavy reliance on PC cases-accounting for nearly 90% of sales-exposes Fractal Gaming Group to shifts in consumer behavior away from DIY desktop PCs, especially as long-term trends indicate rising adoption of compact computing devices, gaming laptops, and all-in-ones, which could reduce future revenue growth.

- Ongoing external headwinds such as U.S. tariffs, global supply chain disruptions, and currency fluctuations have already eroded product margins and may continue to pressure net margins and earnings if global trade tensions or regulatory risks persist or worsen.

- Expansion into new product categories (e.g., headsets and chairs) is still nascent, and with early evidence of lower margins and launch-related sales volatility in these segments, diversification away from the core business may not offset potential declines in the main PC case market, thereby limiting revenue growth and compressing overall margins.

- Rising operating and inventory costs tied to strategic initiatives-increased warehousing, kickbacks, and inventory buildup-could persist if demand slows or market conditions change, further impacting net margins and cash flow.

- The broad PC hardware market is subject to longer and less pronounced upgrade cycles, and future consumer upgrading may slow as cloud/mobile gaming grows and the DIY PC market matures, posing a risk of stagnating or declining top-line revenue and profitability over the long term.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of SEK21.33 for Fractal Gaming Group based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of SEK35.0, and the most bearish reporting a price target of just SEK14.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be SEK748.9 million, earnings will come to SEK65.1 million, and it would be trading on a PE ratio of 11.6x, assuming you use a discount rate of 6.8%.

- Given the current share price of SEK14.0, the analyst price target of SEK21.33 is 34.4% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Fractal Gaming Group?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.