Last Update 02 Jul 26

Fair value Decreased 50%OSSD: Higher Margin Outlook And Lower P/E Will Support Future Re Rating

Analysts have adjusted their price target on OssDsign to SEK 6.40 from SEK 12.75, citing updated assumptions around revenue growth, profit margins, and a lower future P/E multiple.

What’s in the News for OssDsign

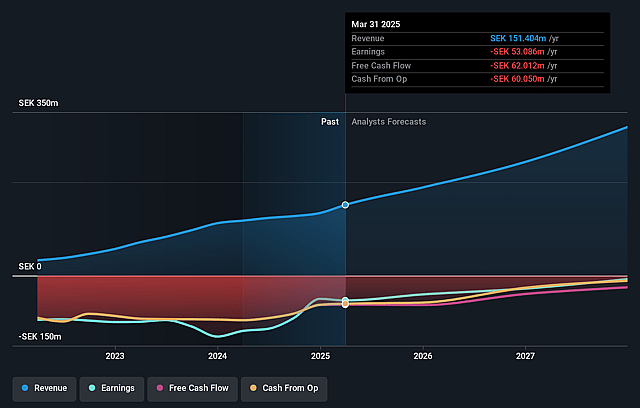

- OssDsign issued earnings guidance for the first quarter of 2026, indicating an expected loss before interest and taxes in the range of SEK 12.0 million to SEK 14.0 million, according to company guidance.

- The company stated that exchange rate effects are expected to have only a marginal impact on the first quarter 2026 EBIT result, based on the same guidance.

- This forward-looking guidance provides investors with an updated reference point for assessing OssDsign’s short term financial outlook, sourced from the company’s published expectations for Q1 2026.

Valuation Changes for OssDsign

- Fair Value: Revised down from SEK 12.75 to SEK 6.40, indicating a significantly lower assessed equity value per share.

- Discount Rate: Adjusted slightly lower from 5.99% to 5.65%, reflecting a modest change in the required return used in the valuation model.

- Revenue Growth: Updated from 26.21% to 22.41%, implying more cautious expectations for future SEK revenue expansion.

- Net Profit Margin: Increased from 5.01% to 10.63%, indicating a higher projected level of profitability on future SEK earnings.

- Future P/E: Reduced from 112.92x to 25.81x, pointing to a materially lower valuation multiple applied to projected earnings.

Key Takeaways

- Strategic shift to orthobiologics boosts growth and operational efficiency, enhancing future revenue and sustaining high net margins.

- U.S. market expansion and distinctive product benefits position OssDsign for significant market share and increased adoption.

- Heavy reliance on limited customers, high competition, and regulatory risks could create revenue volatility and potential cash flow challenges.

Catalysts

About OssDsign- Designs, manufactures, and sells implants and material technology for bone regeneration in Sweden, Germany, the United States, the United Kingdom, rest of Europe, and internationally.

- The strategic shift to a pure-play orthobiologics company has proven highly successful, as evidenced by over 100% year-over-year growth. Continued operational efficiency improvements and scalability are expected to drive future revenue growth.

- The company's gross margin increased to 95.4% for the full year, up from 74.6% in 2023, signaling improved production efficiencies that are likely to sustain high net margins moving forward.

- OssDsign's significant investment in building a robust repository of clinical evidence through more than 10 clinical and preclinical white papers enhances its value proposition, which could drive increased adoption and revenue.

- The expansion into the U.S. market, including the signing of a large GPO contract and broad access to hospitals and surgical centers, positions OssDsign favorably to capture significant market share, boosting future earnings.

- OssDsign Catalyst’s unique capabilities, such as exceptional intraoperative handling qualities and dual pathway bone formation, provide distinct competitive advantages likely to lead to increased sales and market penetration.

OssDsign Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming OssDsign's revenue will grow by 22.4% annually over the next 3 years.

- Analysts are not forecasting that OssDsign will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate OssDsign's profit margin will increase from -27.8% to the average SE Medical Equipment industry of 10.6% in 3 years.

- If OssDsign's profit margin were to converge on the industry average, you could expect earnings to reach SEK 33.6 million (and earnings per share of SEK 0.29) by about July 2029, up from -SEK 47.9 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 25.8x on those 2029 earnings, up from -9.5x today. This future PE is lower than the current PE for the SE Medical Equipment industry at 32.0x.

- Analysts expect the number of shares outstanding to grow by 1.34% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 5.65%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The company relies heavily on a limited number of customers and specific orders for growth, indicated by the mention of one-off orders contributing to past growth, which could create revenue volatility. (Revenue)

- The presence of high competition in the orthobiologics market suggests potential difficulty in maintaining high growth and market share, impacting future revenue projections. (Revenue)

- Increased provisions related to royalty payments indicate the possibility of higher-than-expected operational costs, which could affect profitability. (Net Margins)

- Despite reaching its targeted revenue run rate, the company is still cash flow negative, indicating challenges in achieving cash flow positivity and potential liquidity issues. (Earnings)

- OssDsign’s reliance on FDA-clearance for future market pursuits suggests potential regulatory risks, which could affect the speed and success of U.S. market expansion. (Revenue)

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of SEK6.4 for OssDsign based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of SEK9.0, and the most bearish reporting a price target of just SEK5.1.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be SEK316.5 million, earnings will come to SEK33.6 million, and it would be trading on a PE ratio of 25.8x, assuming you use a discount rate of 5.7%.

- Given the current share price of SEK4.11, the analyst price target of SEK6.4 is 35.9% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on OssDsign?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.