Last Update 08 Aug 25

Fair value Decreased 1.06%With OssDsign's consensus price target revised lower, primarily driven by a notable drop in its Future P/E from 77.22x to 64.47x, the fair value estimate has decreased from SEK15.67 to SEK14.83.

What's in the News

- An undisclosed buyer acquired an unknown minority stake in OssDsign AB from Karolinska Development AB.

- One-year PROPEL registry results for OssDsign Catalyst showed an 88.4% spinal fusion rate in a highly complex patient cohort, with no unexpected device-related adverse events and significant patient improvement.

- Completed a follow-on equity offering of SEK 158.125 million via direct listing at SEK 13.75 per share.

- Revised financial targets to achieve over SEK 400 million in sales by 2028 (30%+ CAGR), with expected EBIT profitability in the second half of the 2025–2028 strategy period.

- Surpassed 10,000 patients treated with OssDsign Catalyst in the US, signaling market traction for the nanosynthetic bone graft.

Valuation Changes

Summary of Valuation Changes for OssDsign

- The Consensus Analyst Price Target has fallen from SEK15.67 to SEK14.83.

- The Future P/E for OssDsign has significantly fallen from 77.22x to 64.47x.

- The Discount Rate for OssDsign remained effectively unchanged, at 5.54%.

Key Takeaways

- Strategic shift to orthobiologics boosts growth and operational efficiency, enhancing future revenue and sustaining high net margins.

- U.S. market expansion and distinctive product benefits position OssDsign for significant market share and increased adoption.

- Heavy reliance on limited customers, high competition, and regulatory risks could create revenue volatility and potential cash flow challenges.

Catalysts

About OssDsign- Designs, manufactures, and sells implants and material technology for bone regeneration in Sweden, Germany, the United States, the United Kingdom, rest of Europe, and internationally.

- The strategic shift to a pure-play orthobiologics company has proven highly successful, as evidenced by over 100% year-over-year growth. Continued operational efficiency improvements and scalability are expected to drive future revenue growth.

- The company's gross margin increased to 95.4% for the full year, up from 74.6% in 2023, signaling improved production efficiencies that are likely to sustain high net margins moving forward.

- OssDsign's significant investment in building a robust repository of clinical evidence through more than 10 clinical and preclinical white papers enhances its value proposition, which could drive increased adoption and revenue.

- The expansion into the U.S. market, including the signing of a large GPO contract and broad access to hospitals and surgical centers, positions OssDsign favorably to capture significant market share, boosting future earnings.

- OssDsign Catalyst’s unique capabilities, such as exceptional intraoperative handling qualities and dual pathway bone formation, provide distinct competitive advantages likely to lead to increased sales and market penetration.

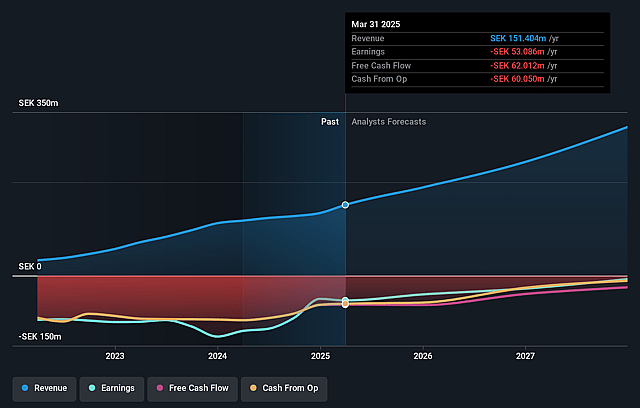

OssDsign Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming OssDsign's revenue will grow by 29.4% annually over the next 3 years.

- Analysts assume that profit margins will increase from -35.1% today to 0.2% in 3 years time.

- Analysts expect earnings to reach SEK 507.4 thousand (and earnings per share of SEK -0.01) by about August 2028, up from SEK -53.1 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting SEK18 million in earnings, and the most bearish expecting SEK-21.7 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 3952.7x on those 2028 earnings, up from -29.5x today. This future PE is greater than the current PE for the SE Medical Equipment industry at 44.1x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 5.56%, as per the Simply Wall St company report.

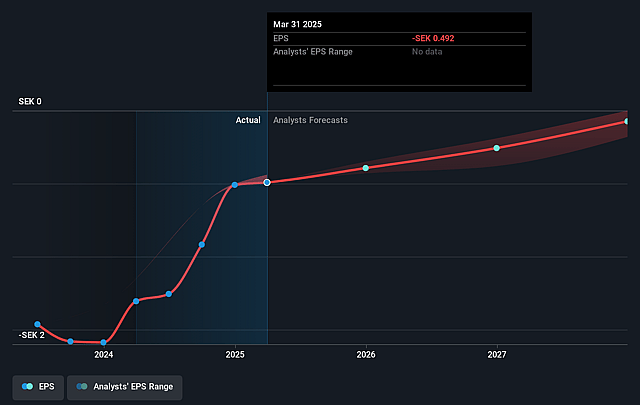

OssDsign Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The company relies heavily on a limited number of customers and specific orders for growth, indicated by the mention of one-off orders contributing to past growth, which could create revenue volatility. (Revenue)

- The presence of high competition in the orthobiologics market suggests potential difficulty in maintaining high growth and market share, impacting future revenue projections. (Revenue)

- Increased provisions related to royalty payments indicate the possibility of higher-than-expected operational costs, which could affect profitability. (Net Margins)

- Despite reaching its targeted revenue run rate, the company is still cash flow negative, indicating challenges in achieving cash flow positivity and potential liquidity issues. (Earnings)

- OssDsign’s reliance on FDA-clearance for future market pursuits suggests potential regulatory risks, which could affect the speed and success of U.S. market expansion. (Revenue)

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of SEK15.5 for OssDsign based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of SEK17.5, and the most bearish reporting a price target of just SEK14.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be SEK328.1 million, earnings will come to SEK507.4 thousand, and it would be trading on a PE ratio of 3952.7x, assuming you use a discount rate of 5.6%.

- Given the current share price of SEK14.16, the analyst price target of SEK15.5 is 8.6% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.